Base Chemical Global Analysis

Global Weekly Catalyst No. 295

- General Thoughts: Global chemical and energy markets remain feedstock- and region-sensitive, with shifting oil-to-gas ratios, margin pressures, and divergent dynamics shaping producer competitiveness and profitability.

- Feedstocks & Energy: North American petrochemical producers hold relative cost advantages from favorable feedstock spreads and US gas still below its 2Q25 average. However, the recent US gas uptick threatens margins.

- Olefins: US spot olefin prices continue to slide relative to overseas levels, reflecting margin pressure. Though selective support could emerge, we anticipate global propylene chain margin headwinds to rise in late 3Q25.

- Other Base Chemicals: Chinese acetyl-chain improvement is a plus for Western producers. US benzene premiums pose headwinds for non-integrated buyers, and weak chlor-alkali demand sees margin pressure in most markets.

- Agriculture: US ammonia margins lift on persistent strength in prices, yet looming supply upticks and likely net demand erosion temper optimism until trends favoring structurally tighter developments emerge post-2026.

- Refining & Biofuels: US ethanol production margins rose to fresh 2025 highs last week on corn weakness and overseas demand. US crude oil refinery margins declined last week but reflect significant YTD improvement.

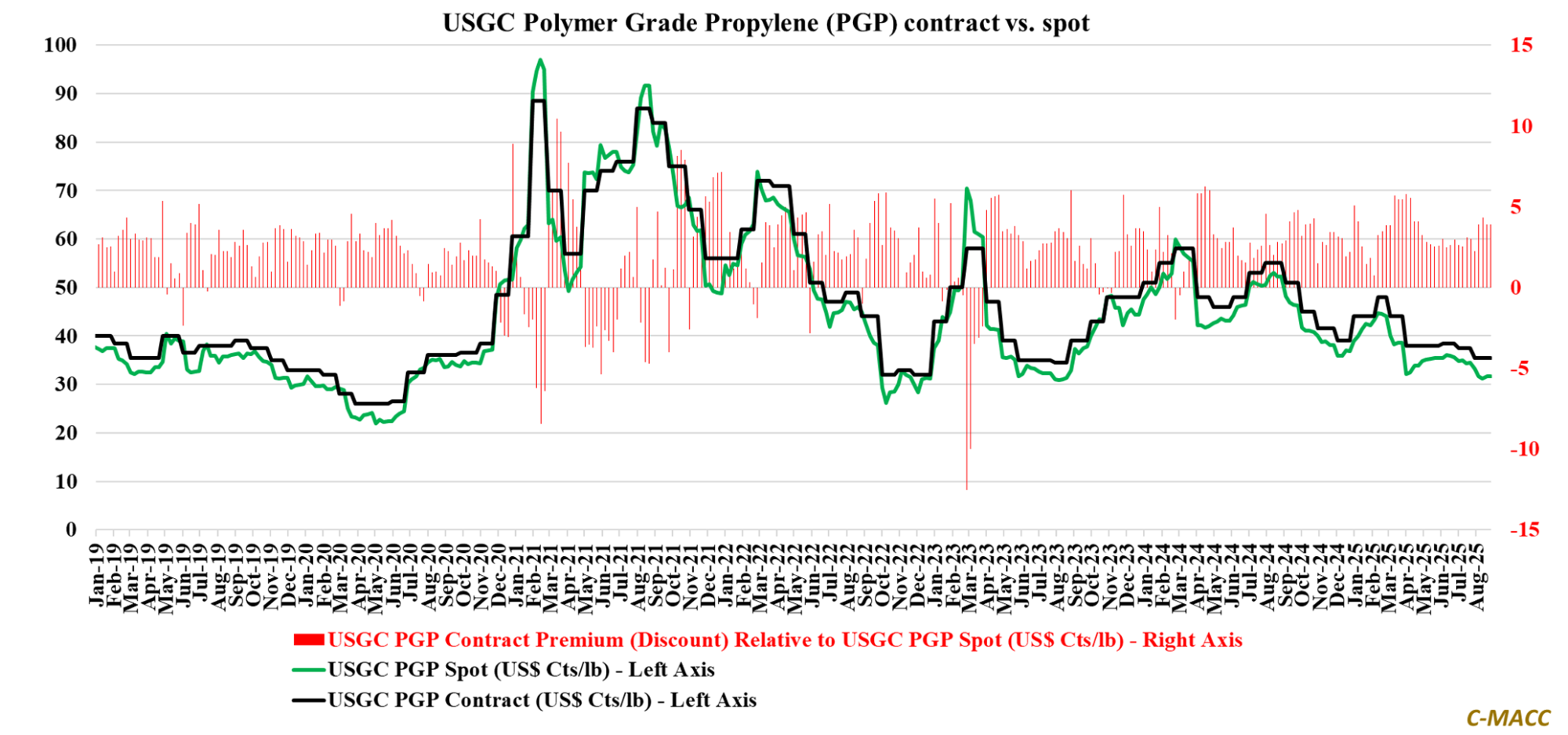

Exhibit 1 – Chart of the Day: US polymer-grade propylene (PGP) contracts follow spot values lower in August.

Source: Bloomberg, C-MACC Analysis, September 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!