Base Chemical Global Analysis

Global Weekly Catalyst No. 297

- General Thoughts: Global chemical markets hinge on resilience over growth, as volatility, protectionism, and uneven rationalization redefine competitive advantage more profoundly than price or demand cycles.

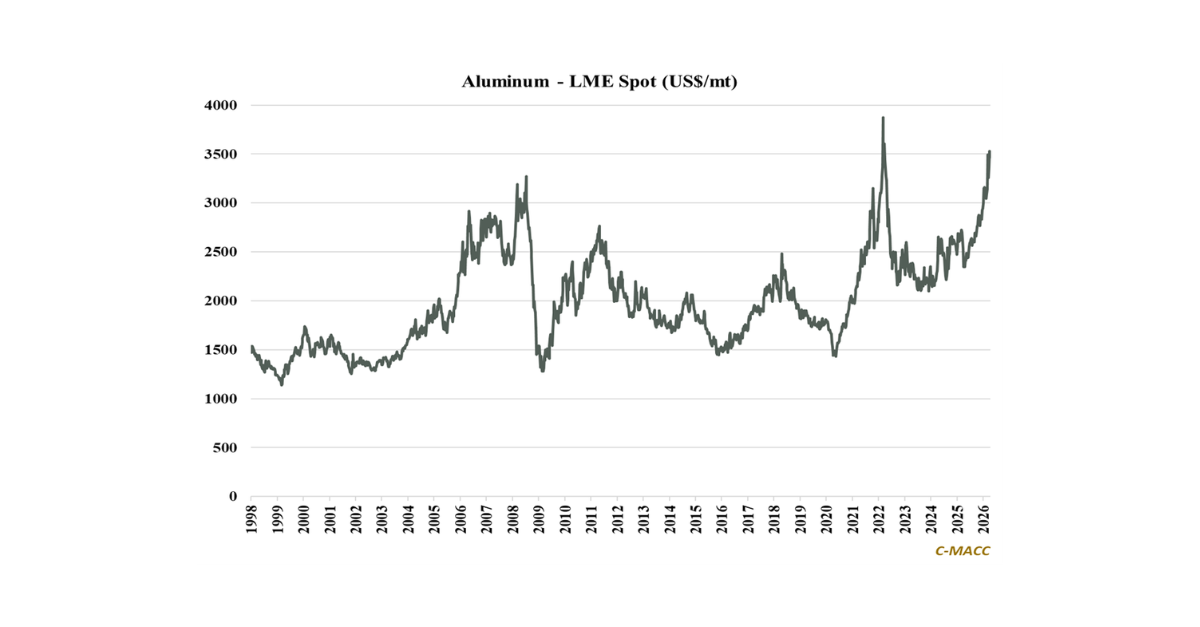

- Feedstocks & Energy: Brent’s easing alongside tightening naphtha balances and slowing Permian growth, offset by expanding midstream capacity, redefine feedstock dynamics near term while laying foundations for 2026.

- Olefins: Global olefins markets reel from outages, oversupply, and diverging spreads as Western hubs languish, Asia tightens, and restructuring pressures mount, setting volatile near-term markets against 2026 improvement.

- Other Base Chemicals: Benzene struggles to sustain gains, methanol steadies with China’s uptick, and chlor-alkali drifts on overcapacity, as volatility, protectionism, and shifting arbitrage redefine advantage into 2H25.

- Agriculture: Global ammonia markets were steady WoW yet reflect higher prices MoM, fueled by corn-driven demand, volatile harvest dynamics, and constrained supply, advantaging low-cost US and Middle East producers.

- Refining & Biofuels: US ethanol margins eased from their recent 2025 highs on rising corn; crude oil refinery margins fell WoW yet remain higher YoY, with policy, demand, and outages shaping a supportive profit setting.

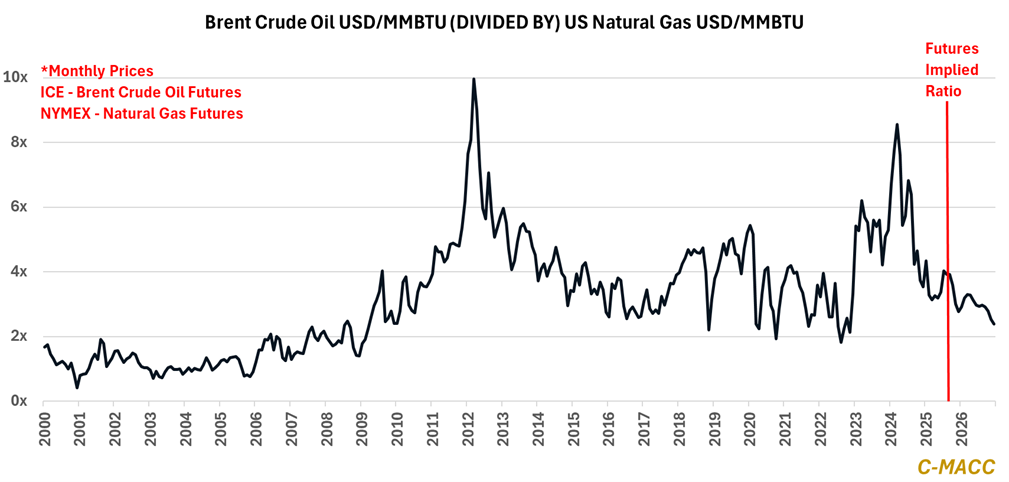

Exhibit 1 – Chart of the Day: Futures markets suggest tighter profits for North American chemical producers in 2026.

Source: Bloomberg, C-MACC Analysis, September 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!