Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

- General Thoughts: Our Pack Expo meetings show advantages shifting from cheap resin to collaboration, certification, and downstream integration, where specifications drive demand, catalyze consolidation, and rewrite competition.

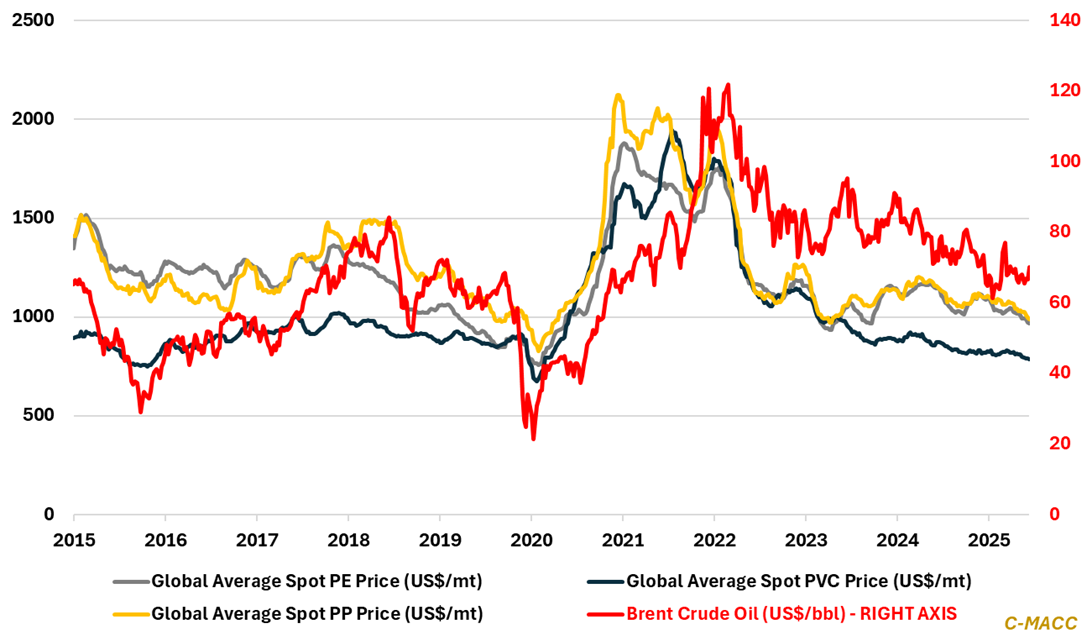

- Polyethylene (PE): Global PE benchmarks remain under pressure as inventories remain elevated, margins tighten, and US and Middle East discounting anchors global floors, leaving any recovery fleeting without structural rationalization.

- Polypropylene (PP): Global PP markets confront relentless oversupply, tightening propylene spreads, and muted demand, pressuring non-integrated producers in the near term, with high-cost regions facing 4Q25 return challenges.

- Polyvinyl Chloride (PVC): Global PVC markets face persistent oversupply, tightening spreads, and fragile demand; without accelerated early 4Q cutbacks and policy-driven catalysts, prices risk deeper declines before 1H26 stabilization.

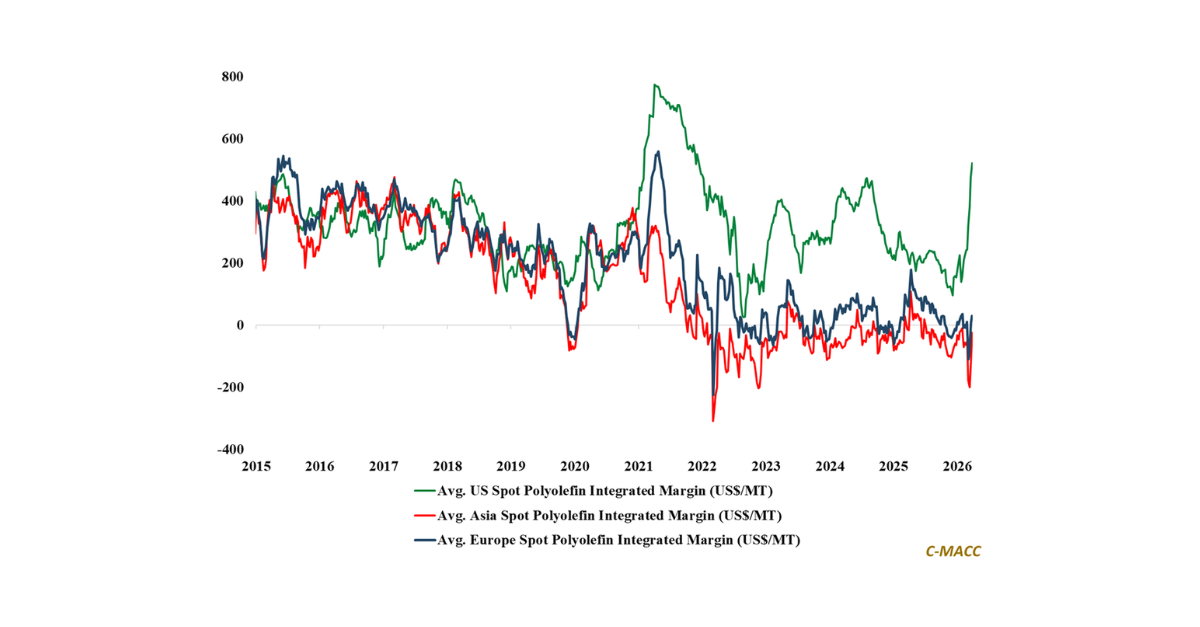

- Other Sector Developments: Global integrated spot polymer margins decreased last week amid rising costs and mostly lower polymer prices, with margin compression reinforcing the need for cutbacks to support per-unit profits in 4Q25.

Exhibit 1 – Chart of the Day: Performance, certification, and collaboration initiatives advance as polymer prices fall.

Source: Bloomberg, Company Reports, C-MACC Analysis, October 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!