Base Chemical Global Analysis

Global Weekly Catalyst No. 300

- General Thoughts: Shifting energy costs, tighter margins, and policy uncertainty redraw the global chemicals map, favoring integrated, flexible producers but pressuring most in a demand- and cost-challenged 4Q setting.

- Feedstocks & Energy: Feedstock divergence flattens global ethylene cost curves; weak Brent, firm US natural gas, and tightening NGL spreads compress margins, reward integration, and punish volume-driven producers.

- Olefins: Global olefin markets fragment as regional spreads diverge, margins compress, and integration depth, not volume, defines advantage amid 2H25 margin volatility and accelerating structural consolidation.

- Other Base Chemicals: Regional divergence, margin compression, and rationalization redefine competitiveness as benzene stabilizes, methanol bifurcates, and chlor-alkali exposes Europe’s fragility amid an uneven 4Q reset.

- Agriculture: Western ammonia tightening, corn-leaning acreage incentives, and policy stagnation are realigning nitrogen demand curves, reshaping fertilizer margins and structural resilience in 4Q25, likely to carry into 2026.

- Refining & Biofuels: US spot ethanol strength, refining margin pressure, and policy tailwinds define a polarized fuels landscape, where integration depth and feedstock agility emerge as decisive competitive advantages.

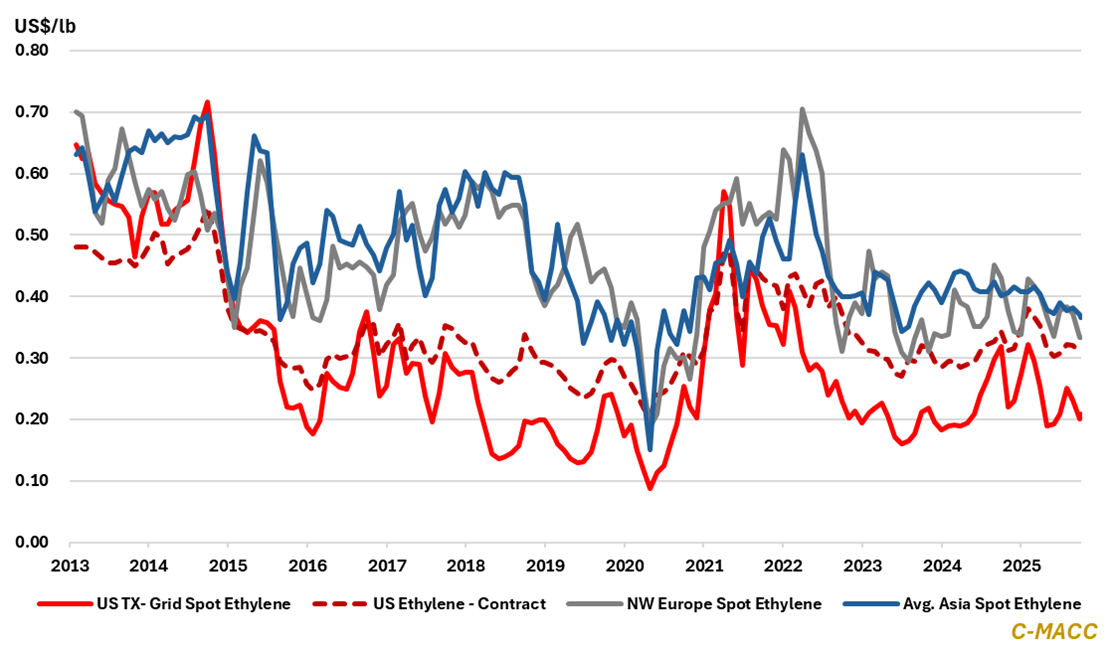

Exhibit 1 – Chart of the Day: US ethylene contract prices step lower in September; US spot margins near 2025 low.

Source: Bloomberg, C-MACC Estimates, October 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!