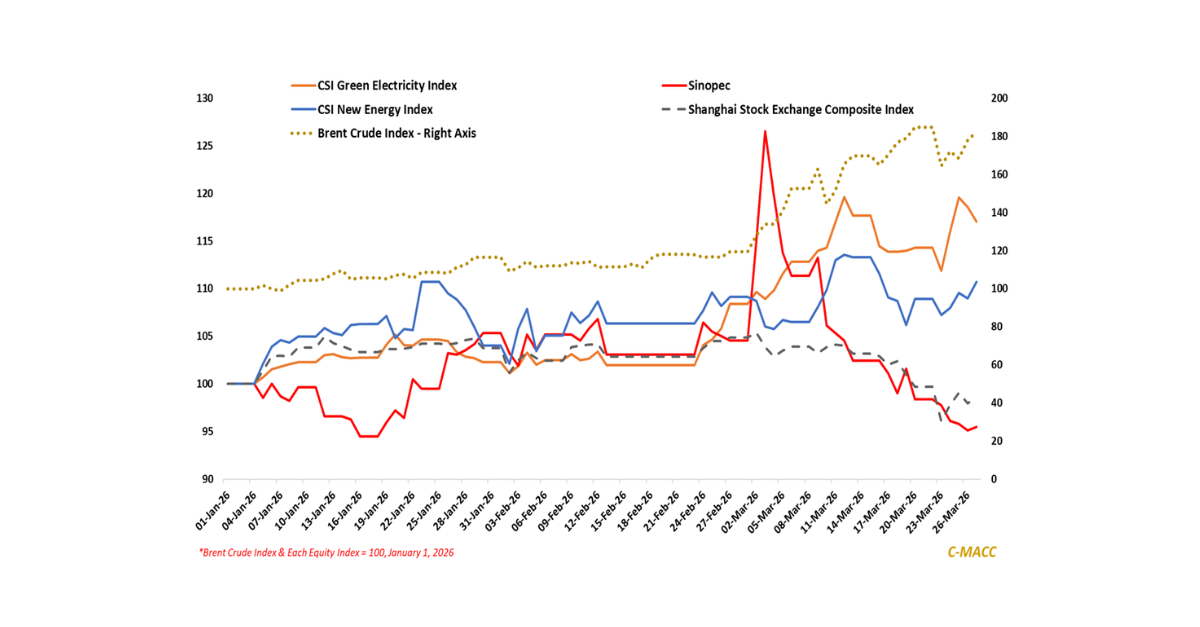

C-MACC Sunday Executive Summary

Return to Sender: Integration Rocks While Scale Rolls Away

- Modular carve-outs and precision platforms increasingly unlock latent value amid cheap energy, long commodity markets, and capital fatigue, driving faster rotation, governance clarity, and monetized agility.

- Coatings, adhesives, and polymers are evolving from commodity supply to embedded performance systems, strategically advancing customer intimacy, allied growth, and verifiable ESG-driven pricing power.

- Energy and chemical majors are streamlining carbon-intensive portfolios while reallocating capital toward circular, differentiated molecules sustaining durable margins and defensible downstream integration.

- Strategy now prioritizes minority retention, externalized execution, and modular governance, converting structural complexity into optionality, valuation expansion, and enduring capital efficiency across cycles.

- Otherwise, integration beats scale; timing, enforcement set margins: benzene self-corrects, LNG timing widens spreads, frontloading fades, Europe weakens, freight normalizes, clean ammonia credibility to pick winners.

- Companies Mentioned: BASF, Henkel, Shell, ExxonMobil, Ineos, OMV, Borouge Group International, ADNOC, Dow, Solvay, Syensqo, Linde, LG Chem, Toyota Tsusho, Reliance Industries, CF Industries, JERA, Mitsui, Woodside, Yara, Fertiglobe, Maersk, Hapag-Lloyd, TotalEnergies, SABIC, SK Geo Centric, ENEOS, H.B. Fuller, Trinseo, Bechtel, BP, Chevron, APA Corporation, Meta, Amazon, Google, Microsoft, Constellation, Talen, Invenergy, Eneco, Shizen Energy, Porsche, Volkswagen, Mercedes-Benz, BMW, Drewry, ArcelorMittal, HYBRIT, H2 Green Steel, NextEra Energy, AES Corporation, Hannon Armstrong, Bloom Energy, Plug Power, Ballard Power Systems, Neste, Sunfire

- Products Mentioned: Ammonia, Hydrogen, Carbon, LNG, Natural gas, Crude oil, Naphtha, Ethane, Propane, Jet fuel, Diesel, Biofuels, Electricity, Power, Fertilizer, Nitrogen, Corn, Ethylene, Propylene, Benzene, Styrene, Caprolactam, Phenol, Methanol, Chlor-alkali, Polyethylene, Polypropylene, Polyvinyl chloride, Polystyrene, Toluene

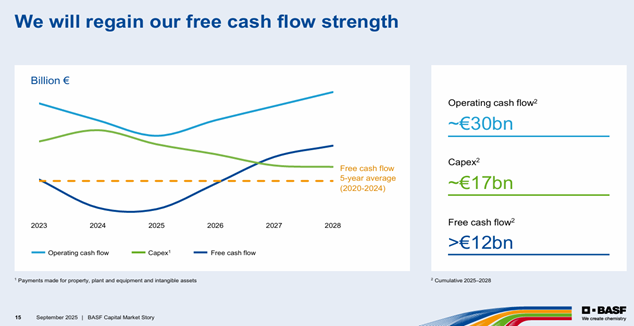

Exhibit 1: BASF pushes forward with its “winning ways” strategy, unlocking value and boosting core FCF conversion.

Source: BASF – Capital Markets Day, October 2025

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!