Global Market Analysis

Margins in Motion: From Acres to Ammonia, Propane to Propylene, to Blue USGC Market Developments

Key Findings

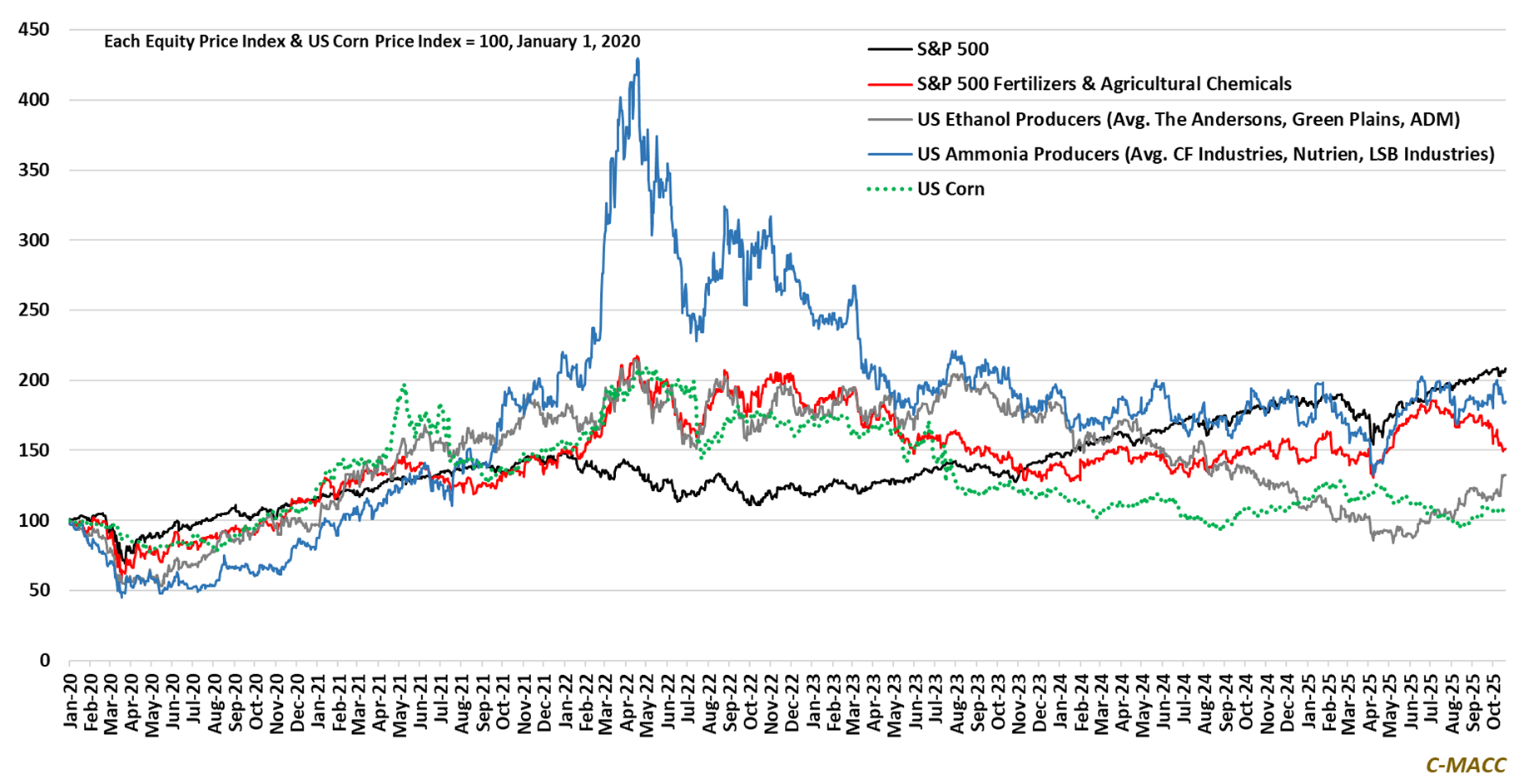

- General Thoughts: Low costs, tight global markets, and expectations for another strong corn-planted acreage year in 2026 amid US soybean export uncertainties have favored US ammonia and ethanol producer equities in 2025.

- Supply Chain/Commodities: Western ammonia prices (& margins) are mostly at or near YTD highs, and notice of production cuts in Trinidad stokes optimism. Separately, US spot polymer-grade propylene prices fall to a YTD low.

- Energy/Upstream: US spot propane prices fall to a 2025 low amid ample inventory, pushing its Mont Belvieu price to reflect a YTD low relative to ethane. Most global crude-linked chemical feedstocks reflect downward pressure.

- Sustainability/Energy Transition: A positive EPA Class VI permit development on the US Gulf Coast benefits its blue ammonia build-out and related infrastructure and reflects positive regional read-throughs for clean ethanol.

- Downstream/Other Chemicals: Soybean-to-corn price ratios favor soybeans, but uncertain Chinese offtake and corridor reliability mean policy and logistics increasingly position as key determinants of 2026 US planting math.

Exhibit 1: US ammonia and ethanol producer equities have surged higher from YTD lows. Will the momentum hold?

Source: Bloomberg, C-MACC Analysis, October 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!