Global Market Analysis

The Chemical Hangover: How Ugly Markets Could Just Be Getting Attractive Again!

Key Findings

- General Thoughts: Pessimism in petrochemicals is capitulation, not a signal; trough pricing, rationalizations, and capital scarcity prewire tighter conditions, as integration and customer intimacy reward relative outperformers.

- Supply Chain/Commodities: Global supply is normalizing through closures, delays, and anti-dumping reroutes; NA and ME runs, Europe trims, Asia redirects, pushing operating rates upward as working capital resets in 2026.

- Energy/Upstream: Energy volatility, not stability, governs advantage; fat-tail gas behavior, as flagged by EQT, spills into NGLs, rewarding integrated producers with storage, hedging sophistication, and LNG-linked optionality.

- Sustainability/Energy Transition: Power reliability has become a scarce commodity; grid delays, turbine backlogs, and transformer constraints spur hybrid solutions, embedding gas-plus-architectures and rewarding circularity.

- Downstream/Other Chemicals: Chemical end markets bifurcate by technology class; data centers, electronics, and coatings pull premiums while tires and construction lag, elevating a spec control over tonnage theme.

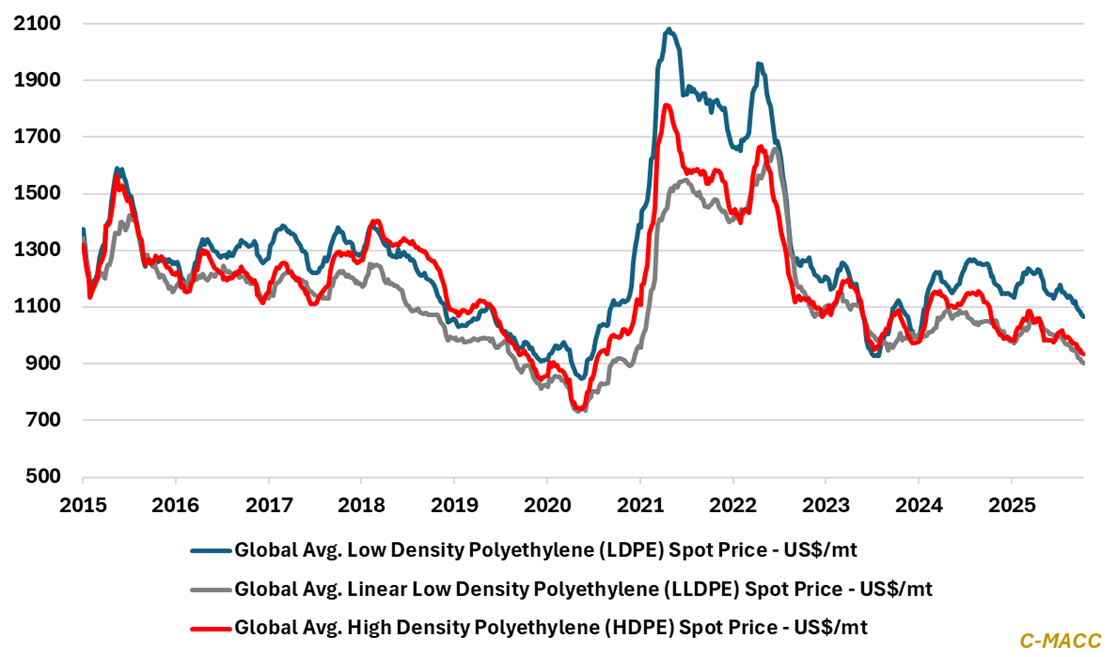

Exhibit 1: Global polyethylene spot prices and integrated margins are under pressure; is it now time to turn positive?

Source: Bloomberg, C-MACC Analysis, October 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!