Base Chemical Global Analysis

Global Weekly Catalyst No. 303

- General Thoughts: Feedstock volatility is uneven and mostly net margin negative, as weak derivative demand keeps chemical profits under pressure in late October, with supply rationalizations needed for improvement.

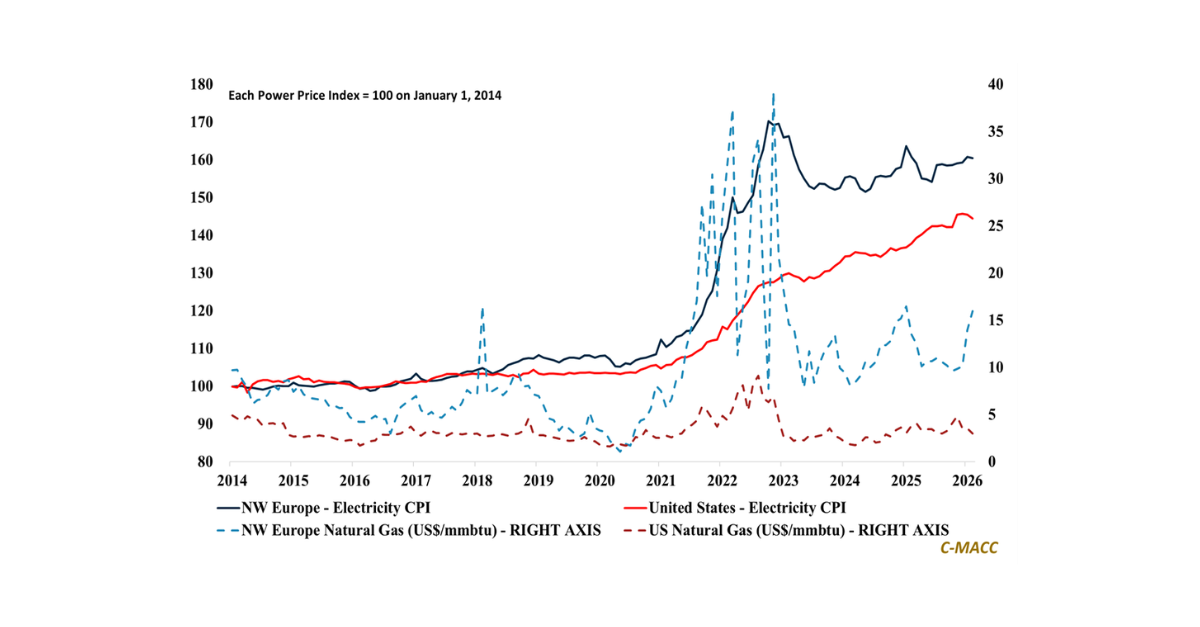

- Feedstocks & Energy: With global crude oil prices rising WoW, natural gas spreads contracting as US prices outpaced flat Europe/Asia and rose faster than oil, implying tighter margins across most global chemical chains.

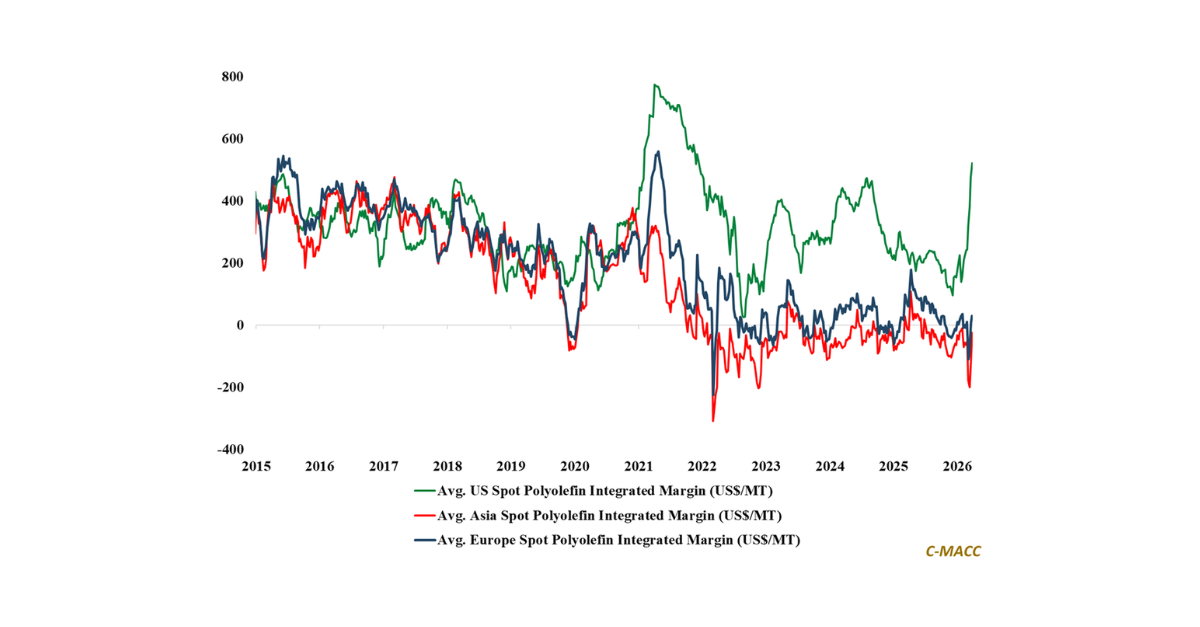

- Olefins: Global olefin prices fell last week, on average, relative to feedstocks that suggest support, with US spot ethylene production margins still near 2025 lows. Global butadiene markets saw sizable price drops last week.

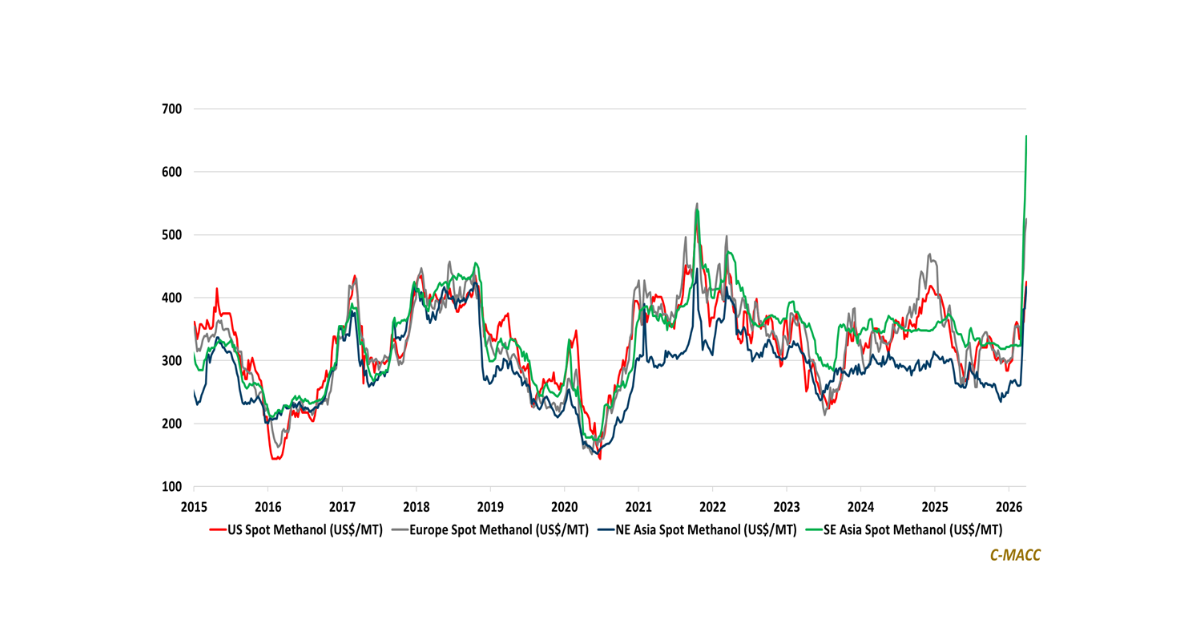

- Other Base Chemicals: Methanol, benzene, and chlor-alkali markets are fragmenting along energy lines, as Western price compression persists while Asia prices show shifts toward selective parity, not broad recovery.

- Agriculture: Ammonia’s plateau reflects engineered scarcity, not structural strength; European highs mask tighter freight and input asymmetries, implying Western margins peak before potentially moderating into 2026.

- Refining & Biofuels: Refining and biofuel chains are shifting from throughput optimization to strategic calibration; policy timing and regional tightness now define returns as input inflation reshapes profit architecture.

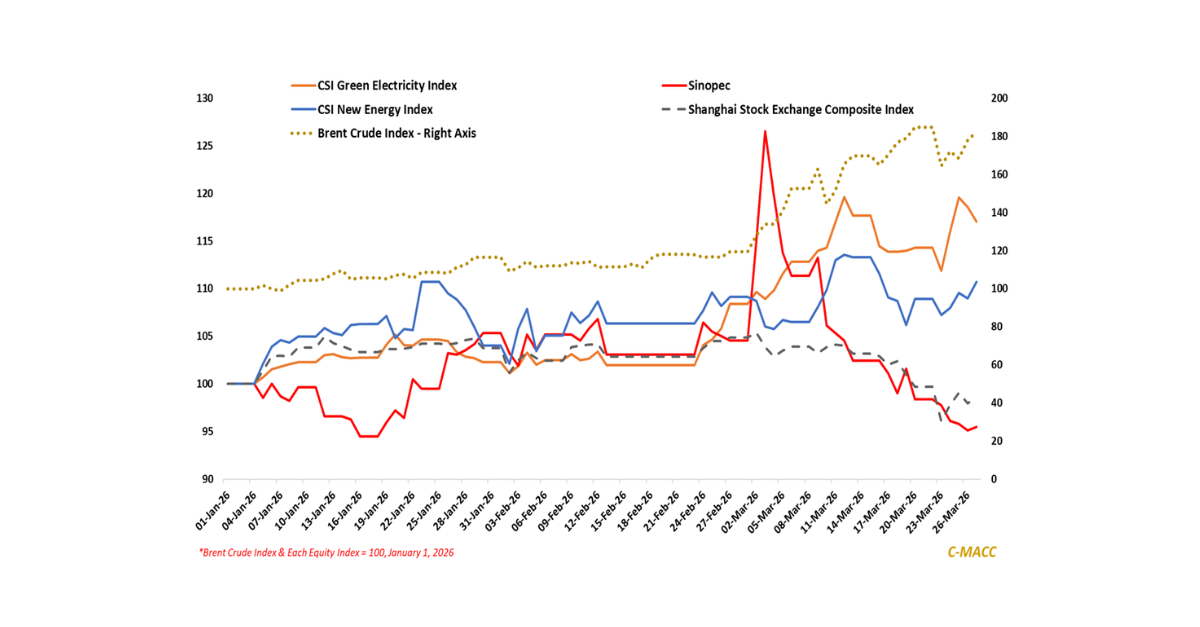

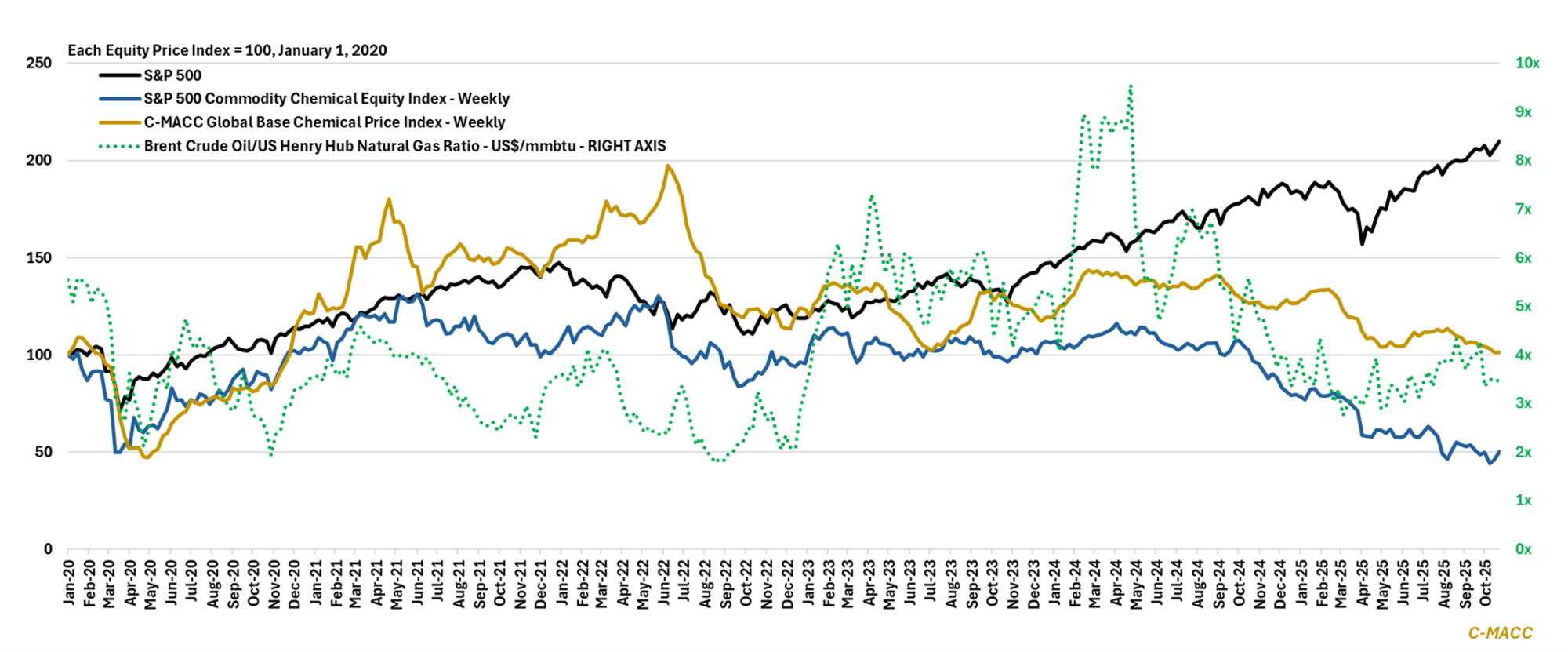

Exhibit 1 – Chart of the Day: US commodity chemical equities stay under pressure amid commodity price weakness.

Source: Bloomberg, C-MACC Estimates, October 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!