Global Market Analysis

No Pain, No Grain – Ammonia Highs Squeeze Corn Profits, Can Soybeans Seize the Moment?

Key Findings

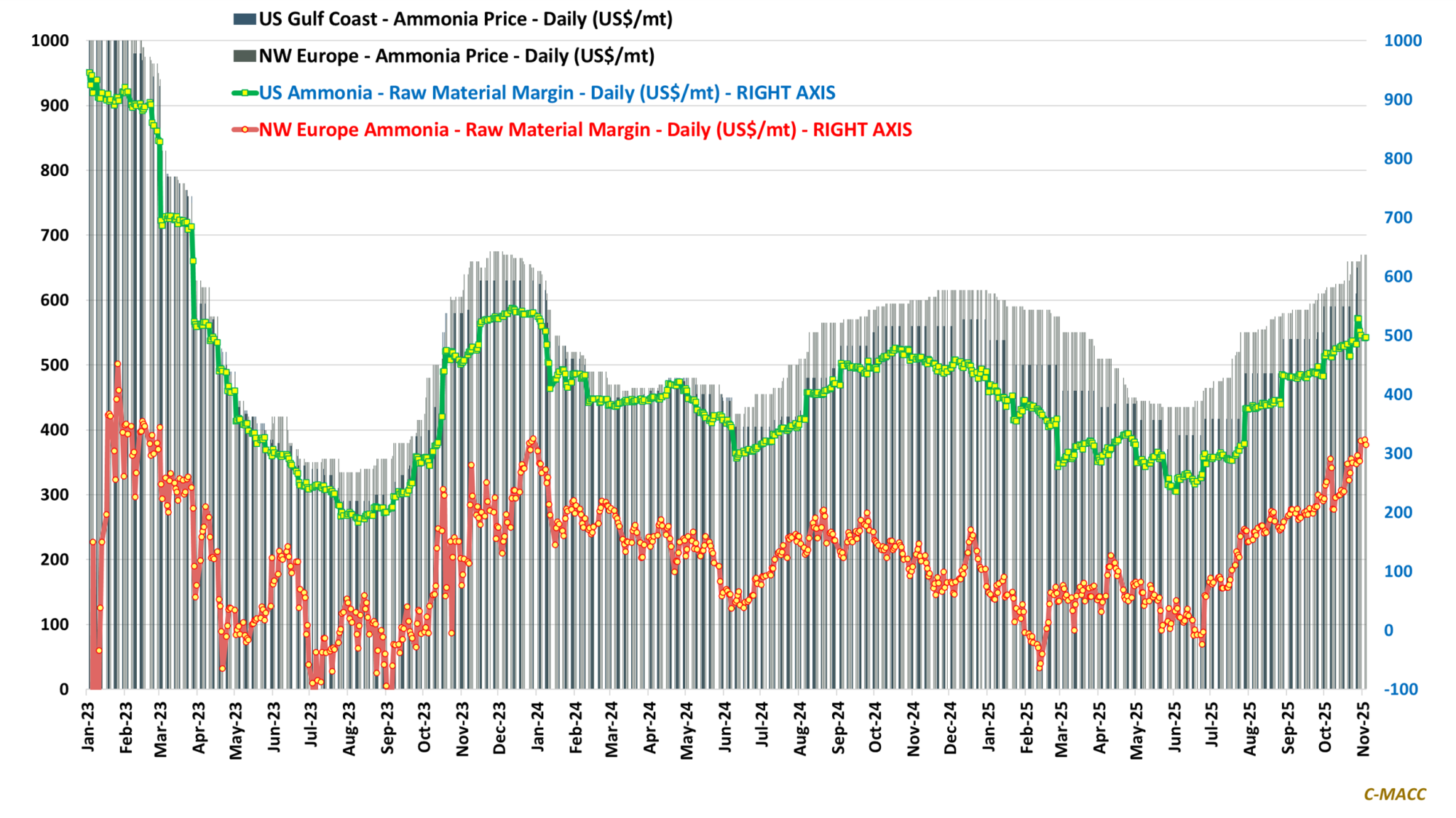

- General Thoughts: Ammonia remains firm amid outages, yet narrowing Atlantic gas spreads, soybean rotation, and supply additions cap upside, shifting value to reliability, demand, and low-carbon positioning into 2026.

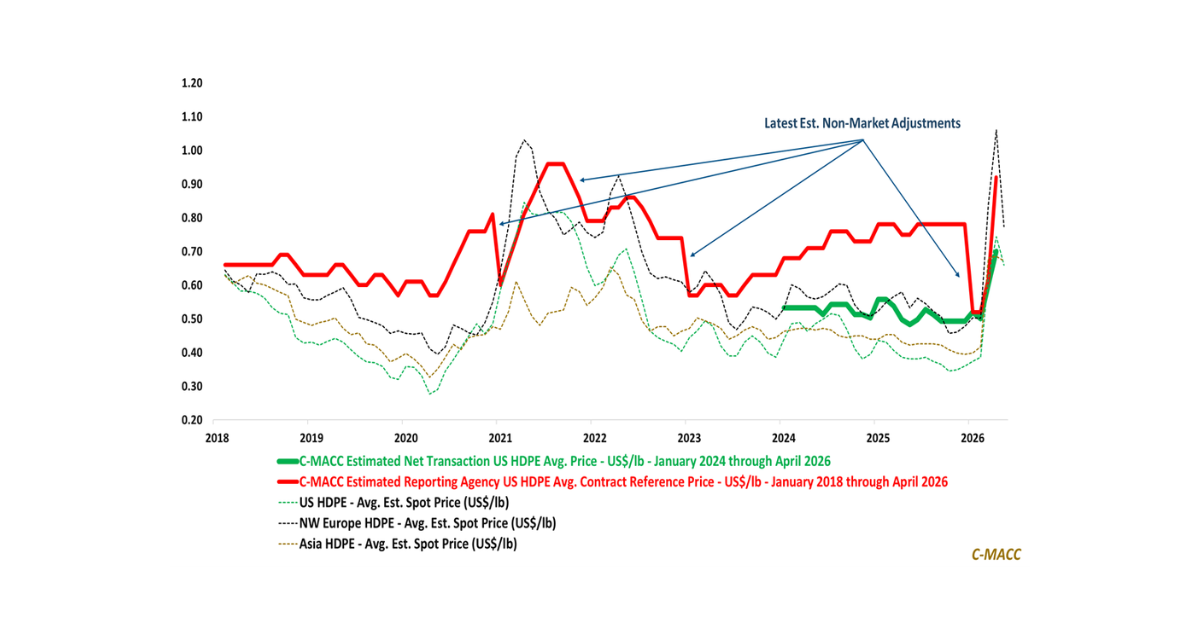

- Supply Chain/Commodities: Saudi producers advance as Aramco boosts downstream integration and SABIC adds capacity, as scale gives way to coordinated value chains anchored by gas and capital amid persistent oversupply.

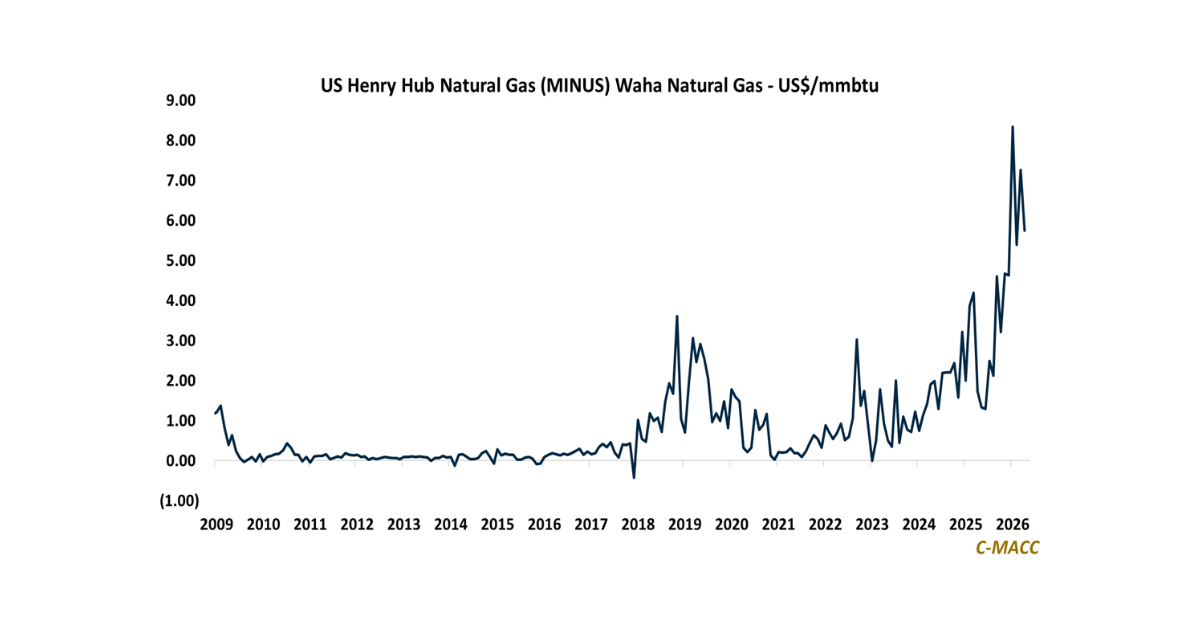

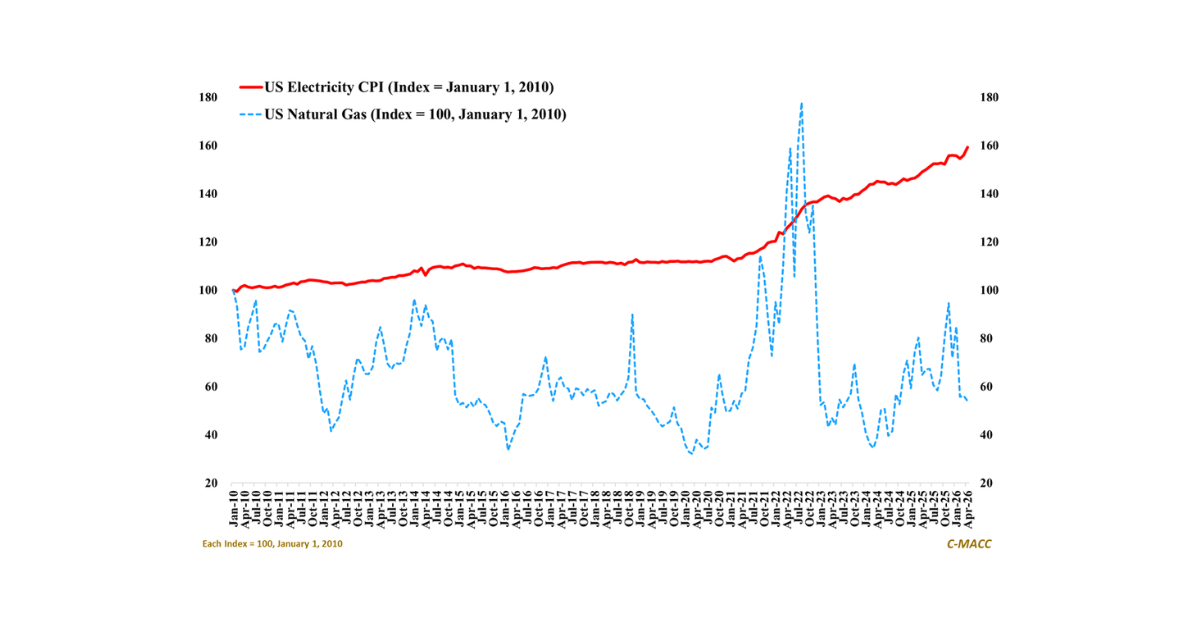

- Energy/Upstream: Global natural gas price spreads compress in 4Q25 as US suppliers balance flows, pipelines move to unlock Permian optionality, and LNG growth sustains demand, favoring infrastructure players into 2026

- Sustainability/Energy Transition: Low-carbon economics pivot from subsidies to integration as Eastman scales methanolysis and ADM realigns its biofuel platform, as companies push to lift margins considering policy volatility.

- Downstream/Other Chemicals: Soybean prices rise in the US and Argentina to favor soy plantings relative to corn in 2026, while trade and demand uncertainty continues to cap sentiment, despite recent US-China trade news.

Exhibit 1: Western ammonia prices hold near their 2025 highs as US and European margins remain resilient.

Source: Bloomberg, C-MACC Analysis, November 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!