Global Market Analysis

November Air: Winds of Pragmatism & Rationalization Stiffen, Global Supply Chains Reconfigure

Key Findings

- General Thoughts: Critical minerals pivot from simple price-recovery bets to resilience math, where capital discipline, restructuring, community license, and carbon intensity increasingly shape competitiveness and returns.

- Supply Chain/Commodities: Global ethylene generally mirrors post-COVID shipping dynamics, as overcapacity spurs closures and pulls advantaged hubs into benchmark-setting, arbitrage-enabled swing-supplier roles.

- Energy/Upstream: European naphtha prices fall to a 2025 low relative to US natural gas, while North American LPG export expansions act to tighten regional spreads and realign global flows around advantaged producers.

- Sustainability/Energy Transition: Hydrogen logistics economics position flows between regions, with China’s green exports and America’s blue exports underwriting decarbonization as Europe sees rising compliance costs.

- Downstream/Other Chemicals: Global chemical demand looks sleepy, not sick; easing mortgages and stabilizing freight costs could stage-manage a shift from defensive maintenance spending toward phased upgrade cycles.

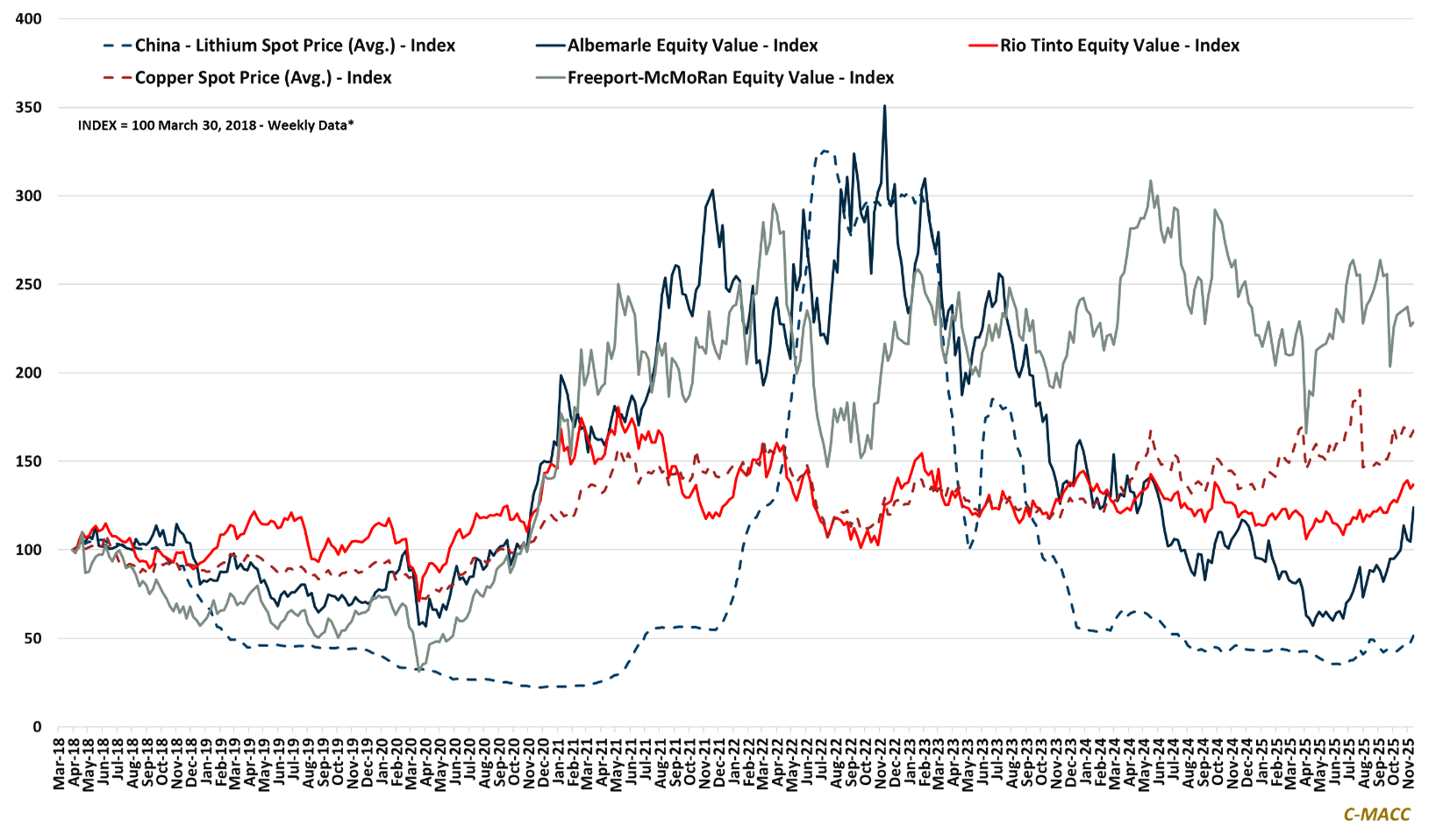

Exhibit 1: Critical mineral prices and producer equities decouple as lithium sentiment rises relative to copper in 4Q25.

Source: Bloomberg, C-MACC Analysis, November 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!