Base Chemical Global Analysis

Global Weekly Catalyst No. 319

- General Thoughts: Oil-to-gas dispersion, cracker co-product volatility, and logistics bottlenecks signal that 2026 returns will reward integration and execution over scale, while accelerating needed sector rationalizations.

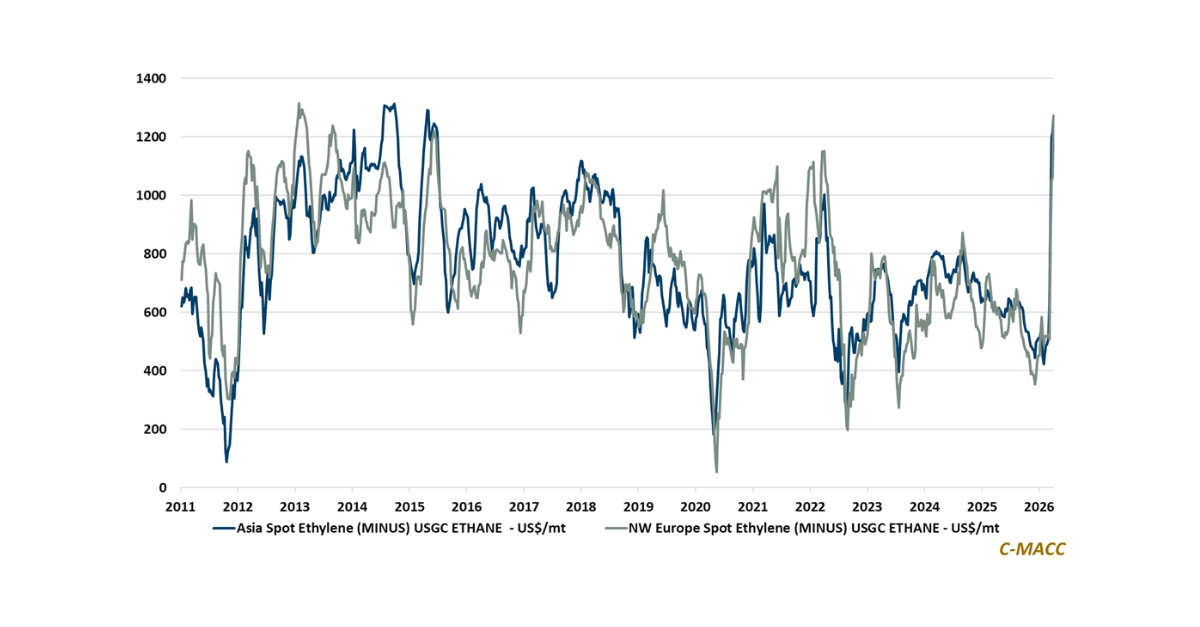

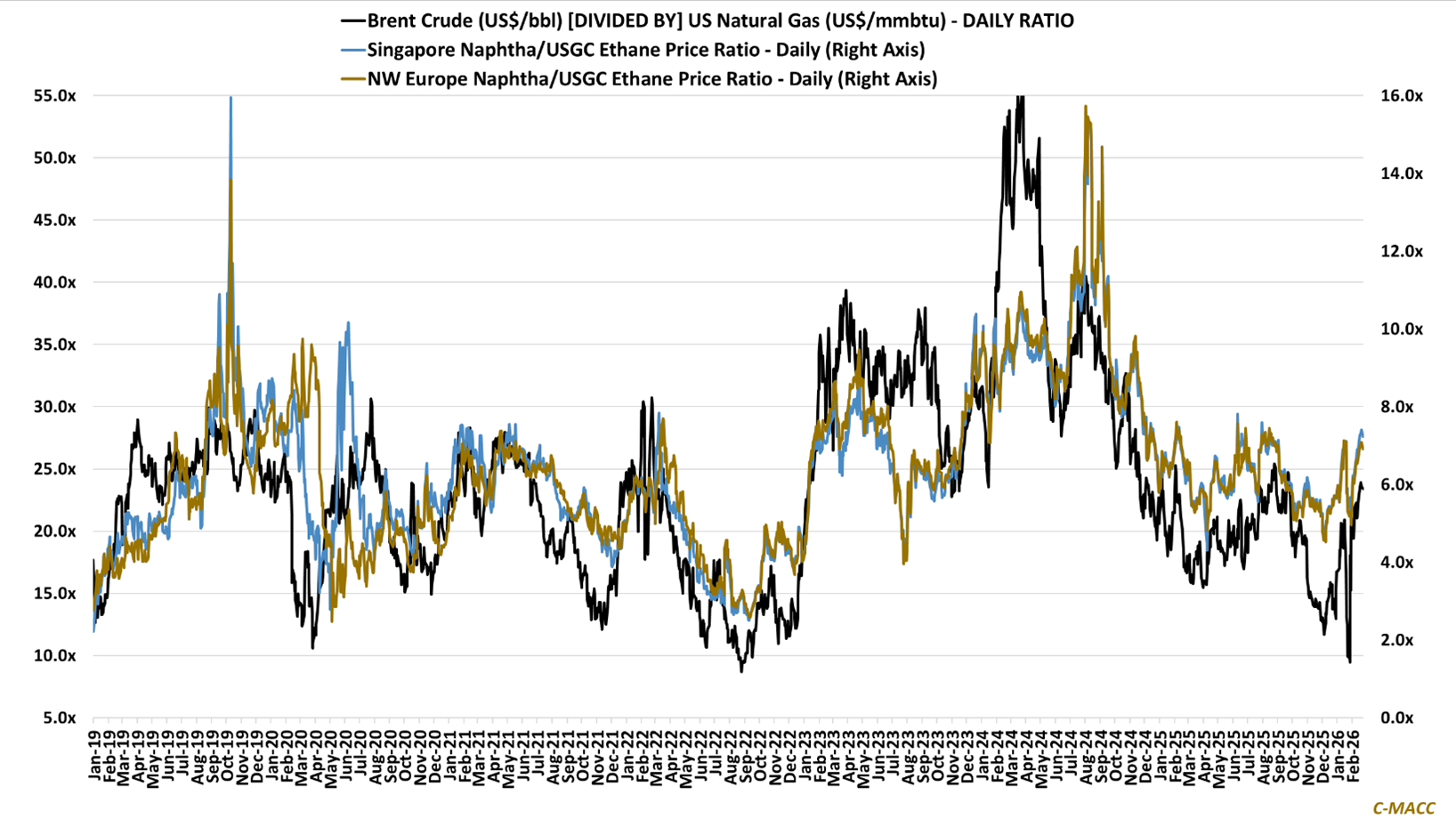

- Feedstocks & Energy: Crude’s renewed strength amid easing natural gas and ethane prices is widening global cost differentials, strengthening North America’s petrochemical cost advantage relative to Europe and Asia.

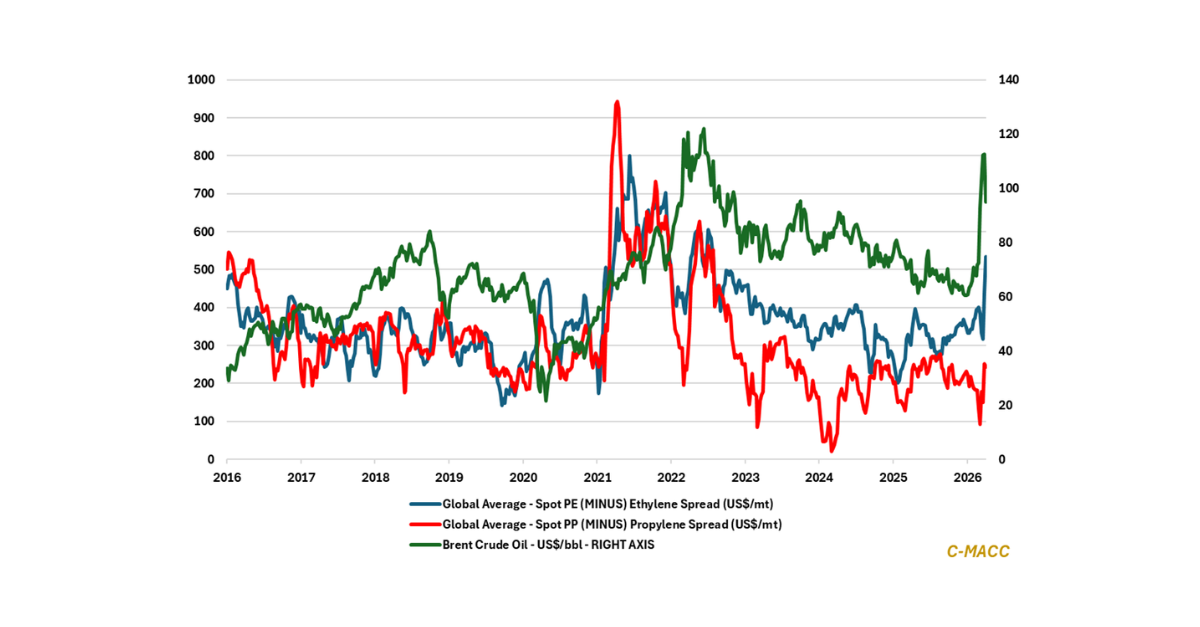

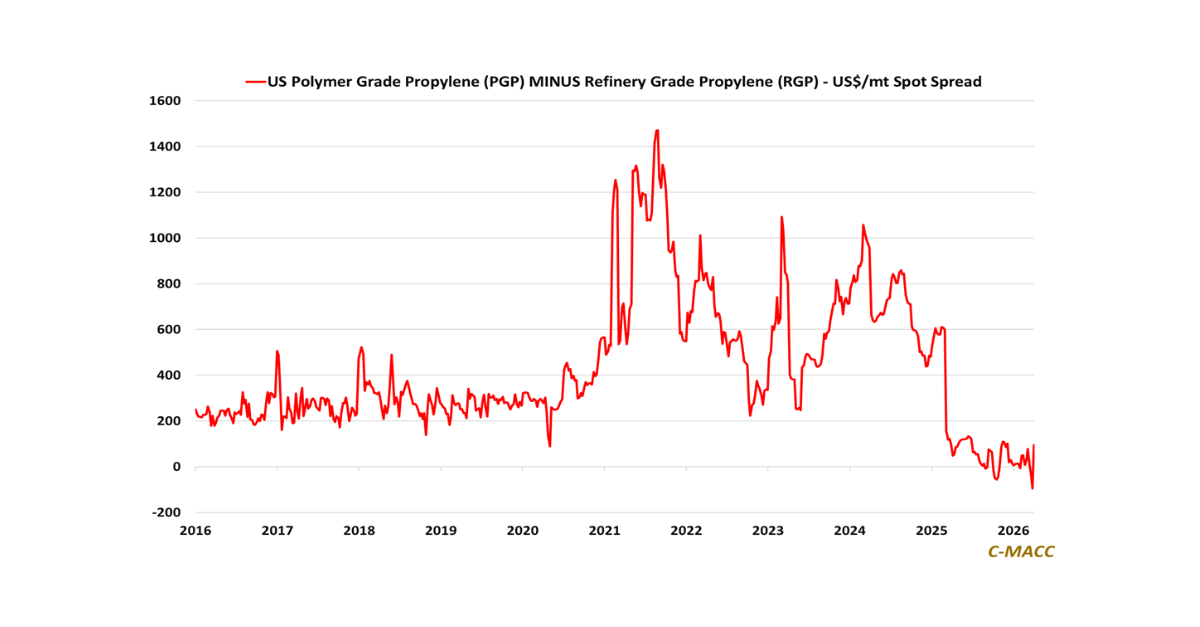

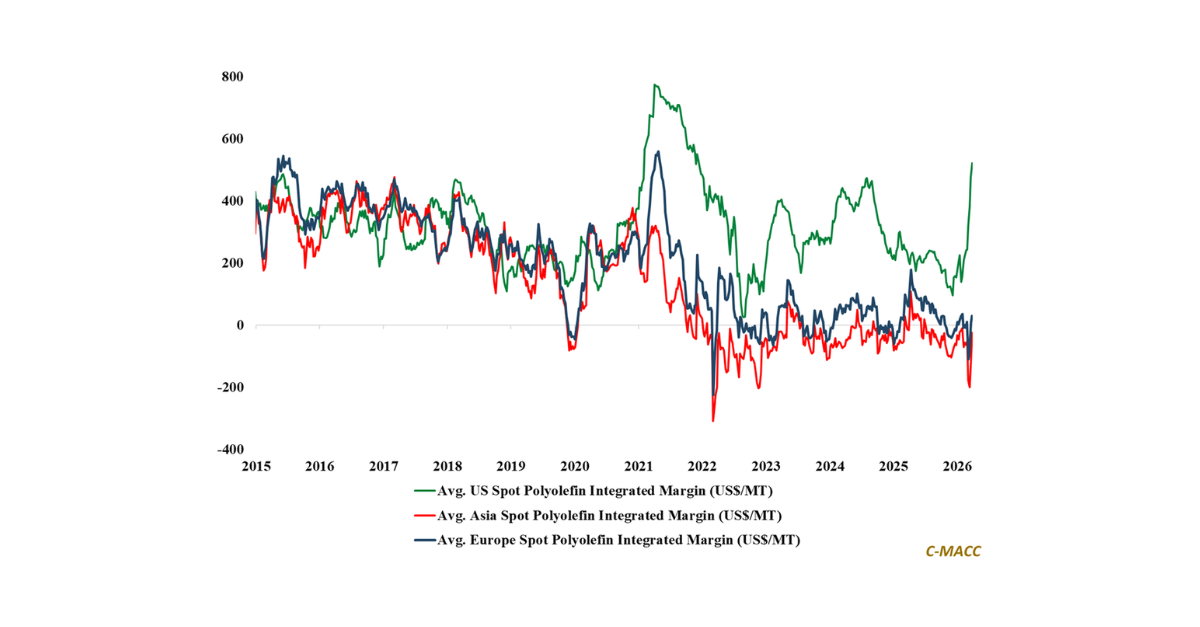

- Olefins: Persistent ethylene oversupply relative to firmer global propylene and butadiene markets, on average, stresses reliable offtake and co-product recovery as margin differentiators among Europe and Asia cracking units.

- Other Base Chemicals: Mixed aromatics, steady Chlor-alkali, and sharply weaker Western methanol markets show that freight positioning and operating discipline, not energy shifts alone, drive intermediate markets.

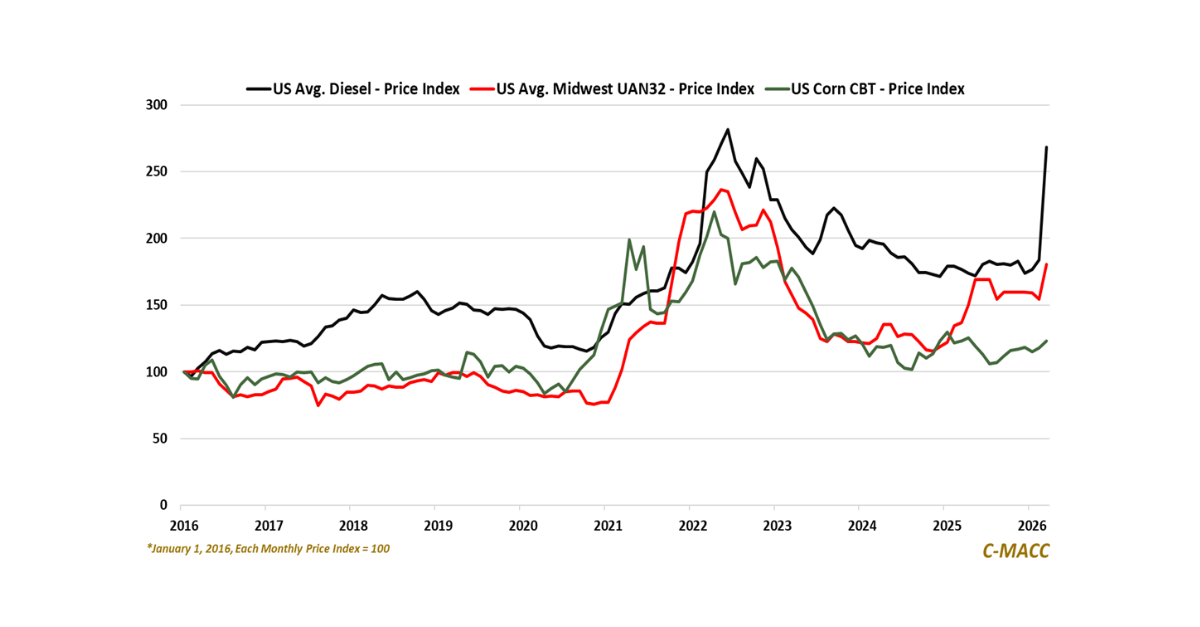

- Agriculture: Lower global natural gas benchmarks are widening implied global ammonia producer margins, yet seasonal demand pacing and export uncertainty will determine the durability of margin expansion into late 1H26.

- Refining & Biofuels: Stronger crude oil and modest crack improvement support refinery margin stabilization, but sustained US refining and ethanol returns in 2026 ultimately depend on utilization discipline and policy clarity.

Exhibit 1 – Chart of the Day: Oil-to-gas and naphtha-to-ethane ratios are rising, widening relative cracking economics.

Source: Bloomberg, C-MACC Estimates, February 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!