Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

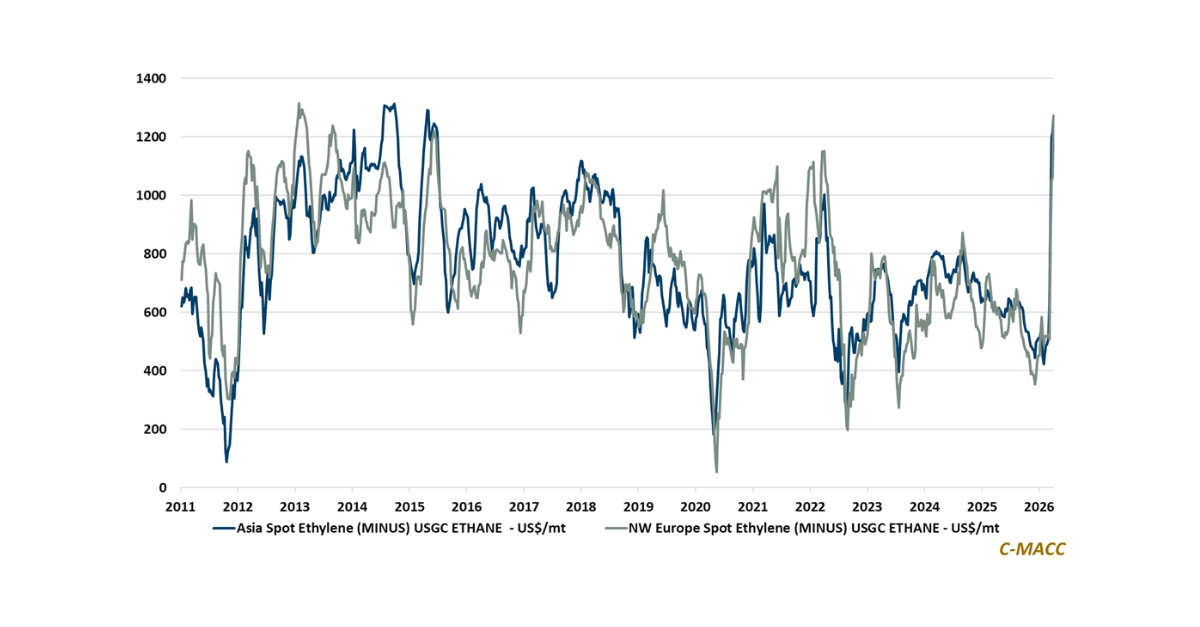

- General Thoughts: Steeper crude oil-linked cost curves and widening feedstock dispersion are forcing rationalization, rewarding integration, and concentrating PE and PVC profitability within advantaged global industrial ecosystems.

- Polyethylene (PE): The global PE outlook hinges less on early-year price strength and more on exporter discipline as China absorbs inventories ahead of significant 2H26 capacity ramps that will intensify pressure on high-cost producers.

- Polypropylene (PP): Propylene inflation is supporting higher PP prices, but 2026 winners will be integrated producers defending spreads as Chinese demand normalizes, high-cost European assets rationalize, and new Asian capacity ramps.

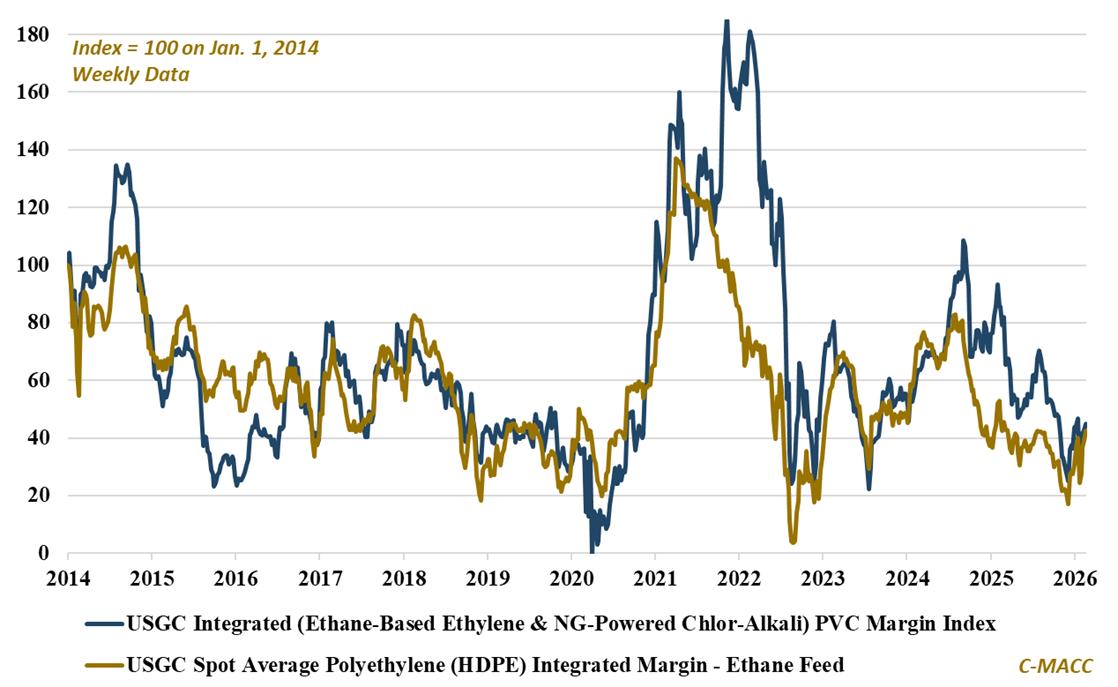

- Polyvinyl Chloride (PVC): Chinese export reform and Indian infrastructure demand are resetting global PVC price floors; sustained producer margin expansion requires surplus absorption without downstream spread compression.

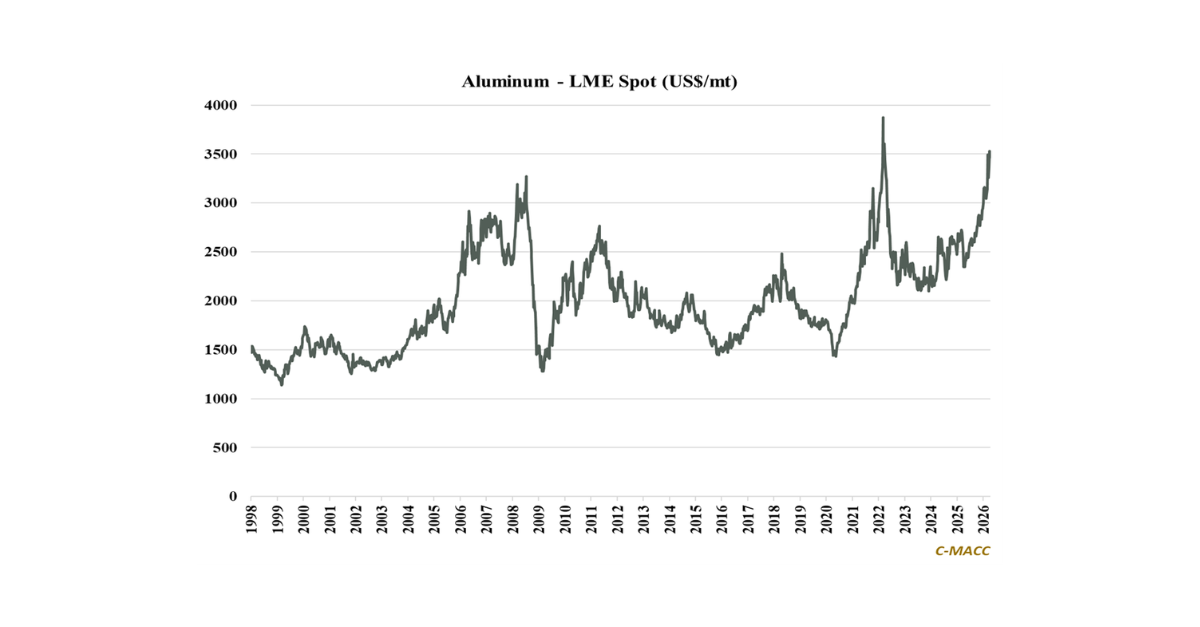

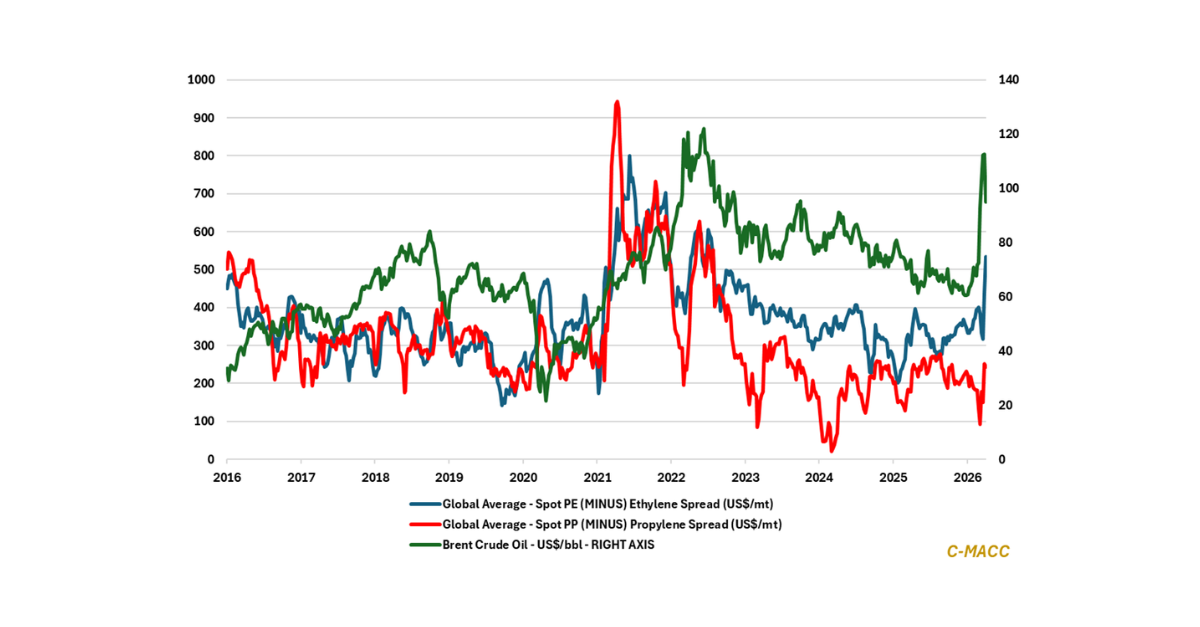

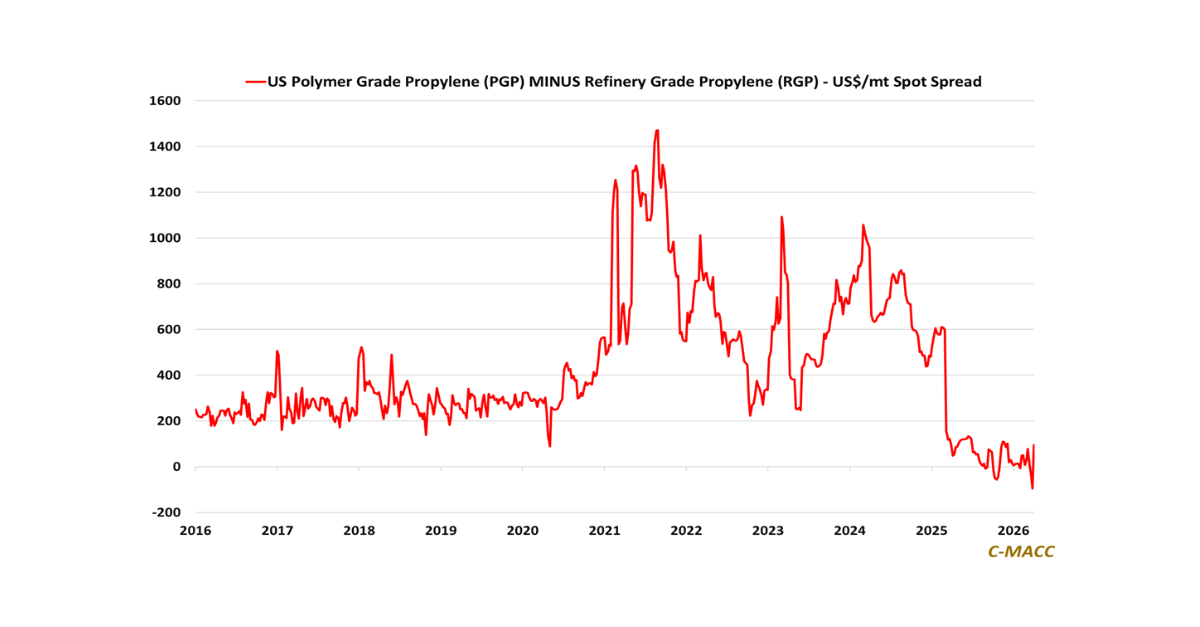

- Other Sector Developments: Oil price support versus US natural gas, firmer naphtha, volatile propane, and tightening PP-to-PGP spreads are reinforcing ethane advantages while pressuring merchant and naphtha-based producers globally.

Exhibit 1 – Chart of the Day: US integrated PVC and PE margins rebound in 1Q26 as global cost dispersion widens.

Source: Bloomberg, C-MACC Analysis, February 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!