Base Chemical Global Analysis

Global Weekly Catalyst No. 320

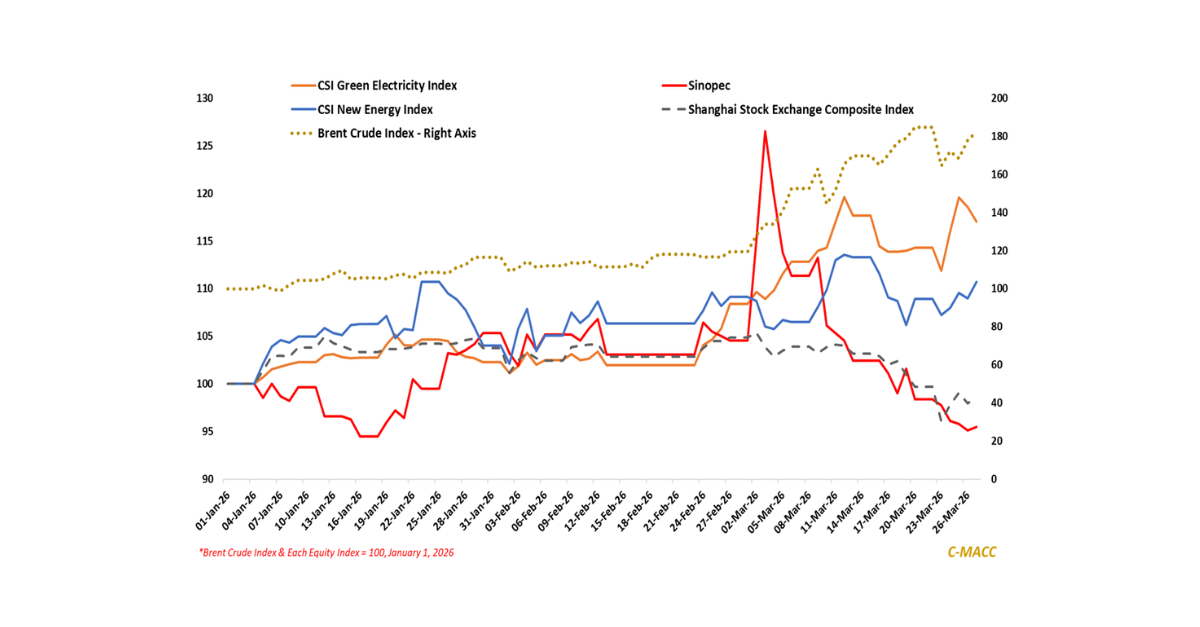

- General Thoughts: Crude oil and Ex-US natural gas price strength relative to US levels has steepened the global cost curve for most chemicals, accelerating rationalization prospects and setting the stage for tighter balances.

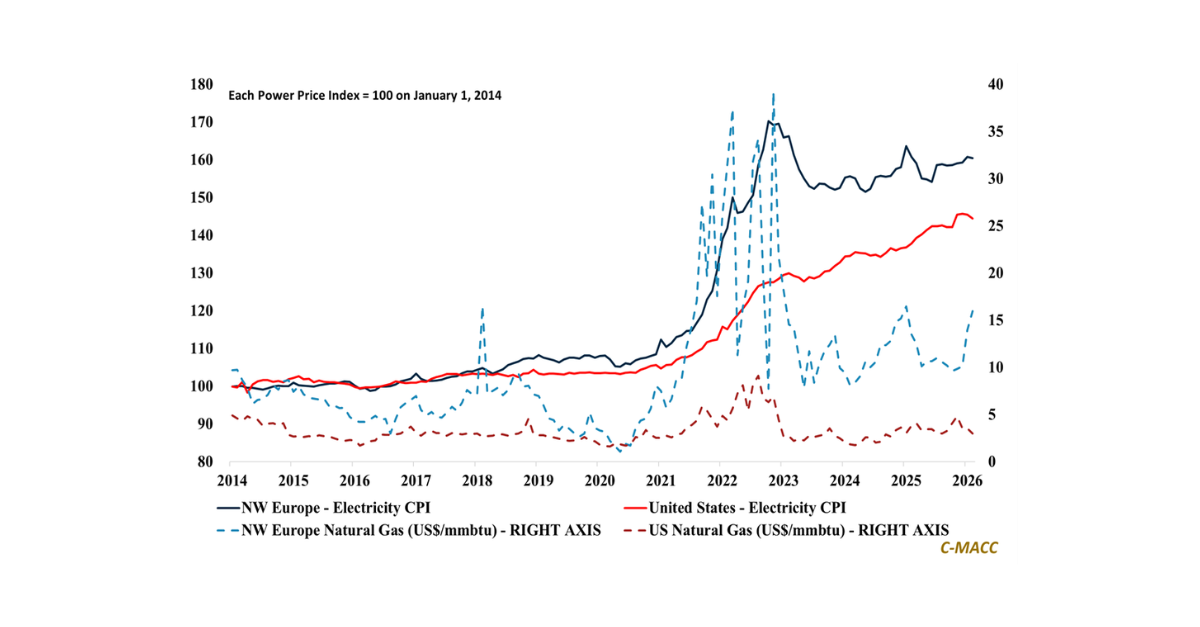

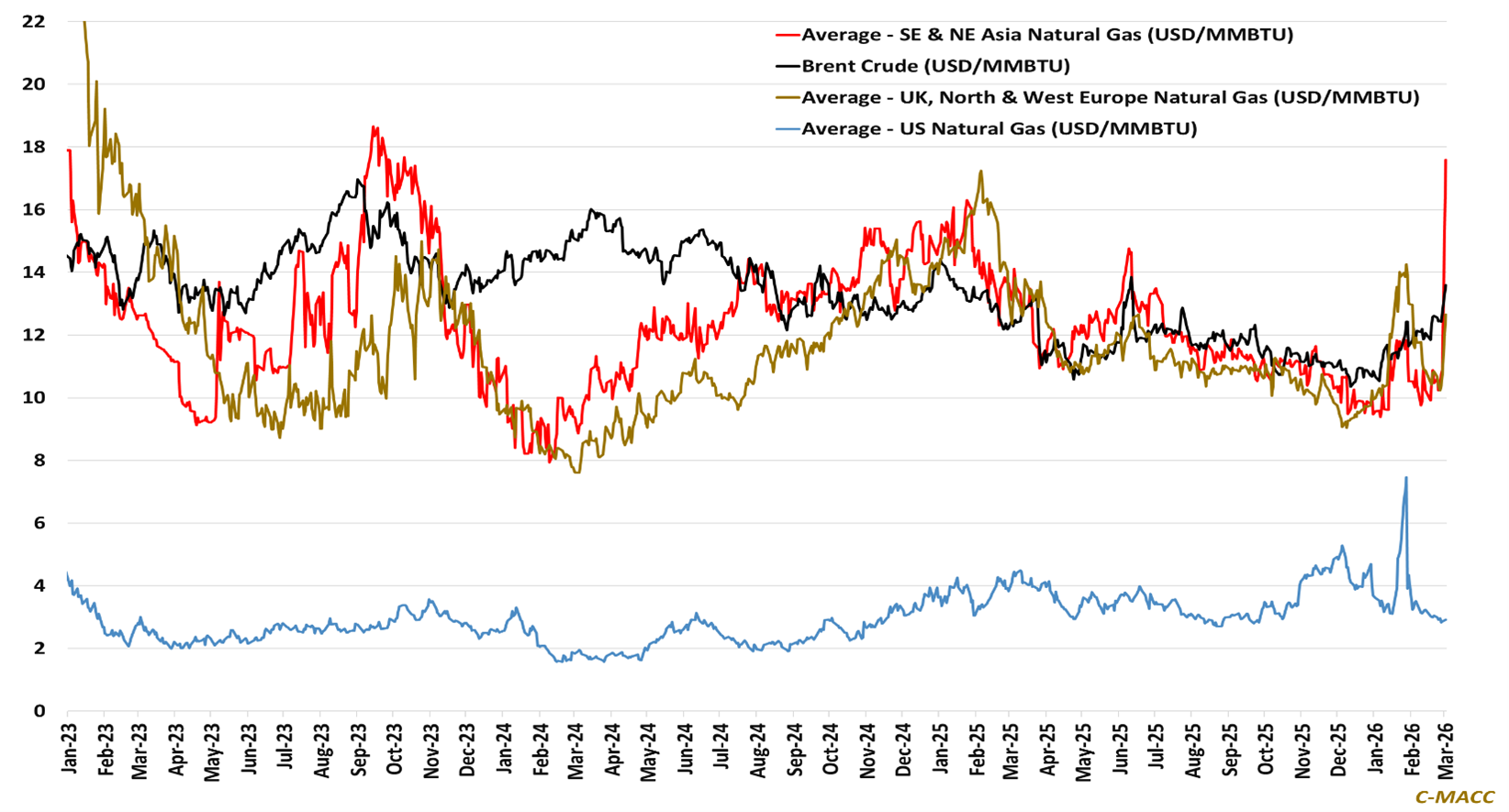

- Feedstocks & Energy: Higher Asian and European natural gas prices and crude oil values following the latest Middle East conflict favor higher prices, but compressed ex-US margins and likely accelerated restructurings.

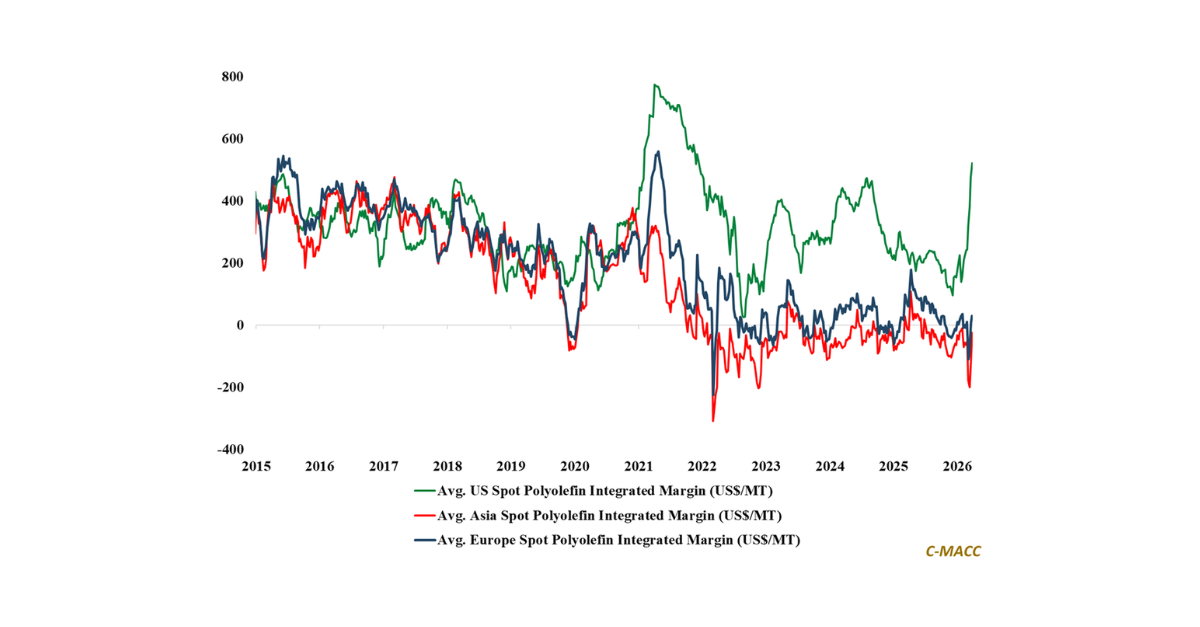

- Olefins: Rising global marginal cracker costs are resetting olefin market-clearing levels, favoring integrated operators relative to non-integrated producers and hastening high-cost capacity exits amid lingering oversupply.

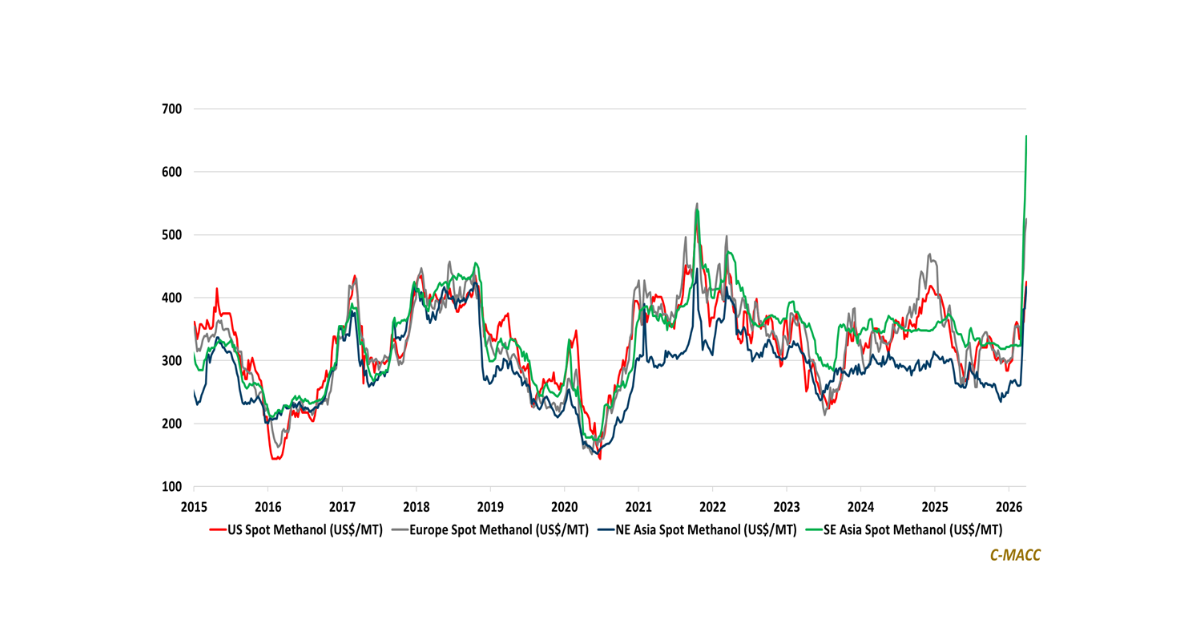

- Other Base Chemicals: Higher ex-US costs raise global intermediate prices, with global methanol markets among those impacted by Iranian disruptions, benefiting low-cost producers with feedstock and shipping optionality.

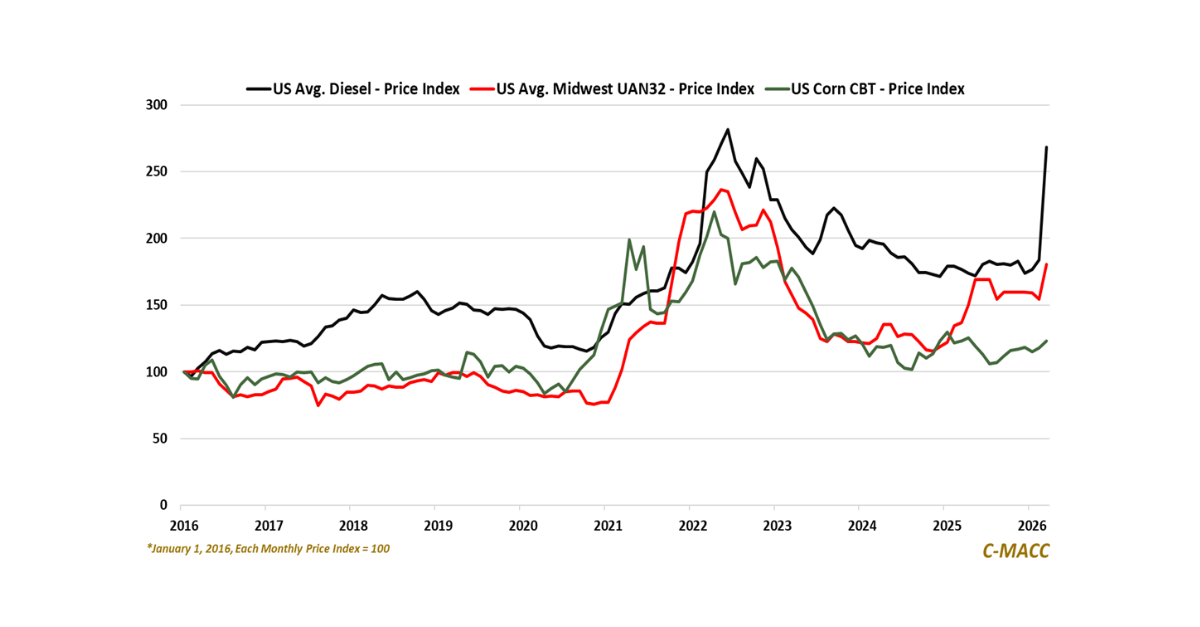

- Agriculture: A steeper global ammonia cost curve improves positioning for natural gas advantaged producers, while raising farmer input costs and posing downside risk to corn planted acreage estimates at the margin.

- Refining & Biofuels: Crude oil volatility will widen dispersion between integrated refiners and marginal players, while gasoline support amid tighter refined product markets implies margin benefits for US ethanol producers.

Exhibit 1 – Chart of the Day: Crude oil and Ex-US natural gas price strength steepens global chemical cost curves.

Source: Bloomberg, C-MACC Estimates, March 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!