C-MACC Sunday Executive Summary

Cheap Gas, Tight Capital: Petrochemical Expansion Remains Selective

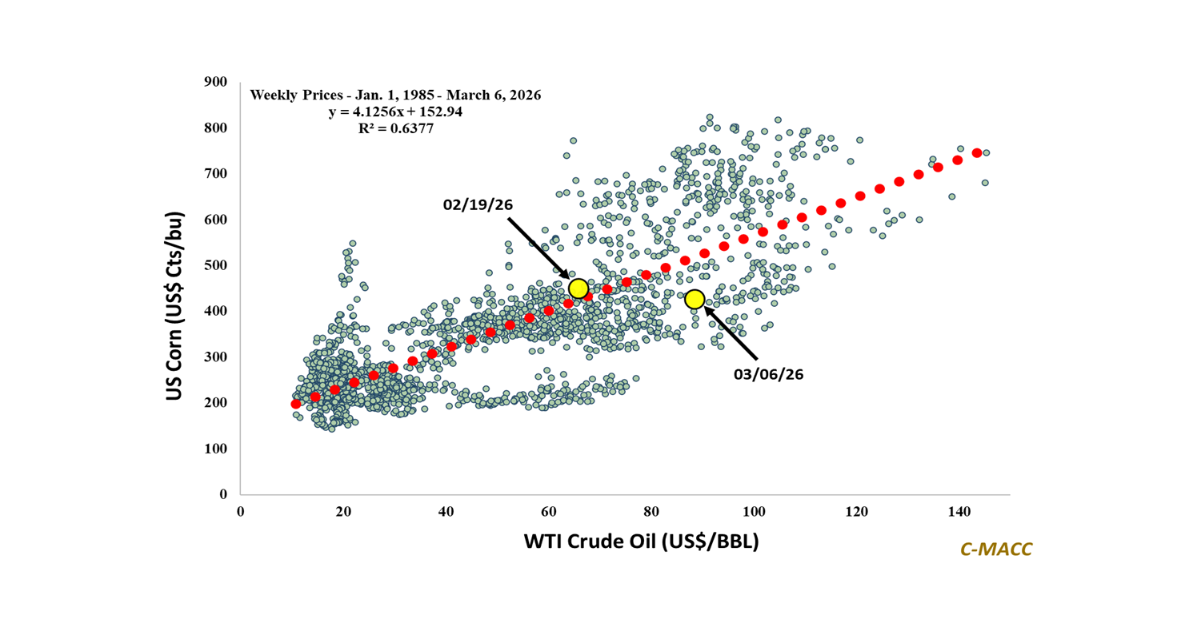

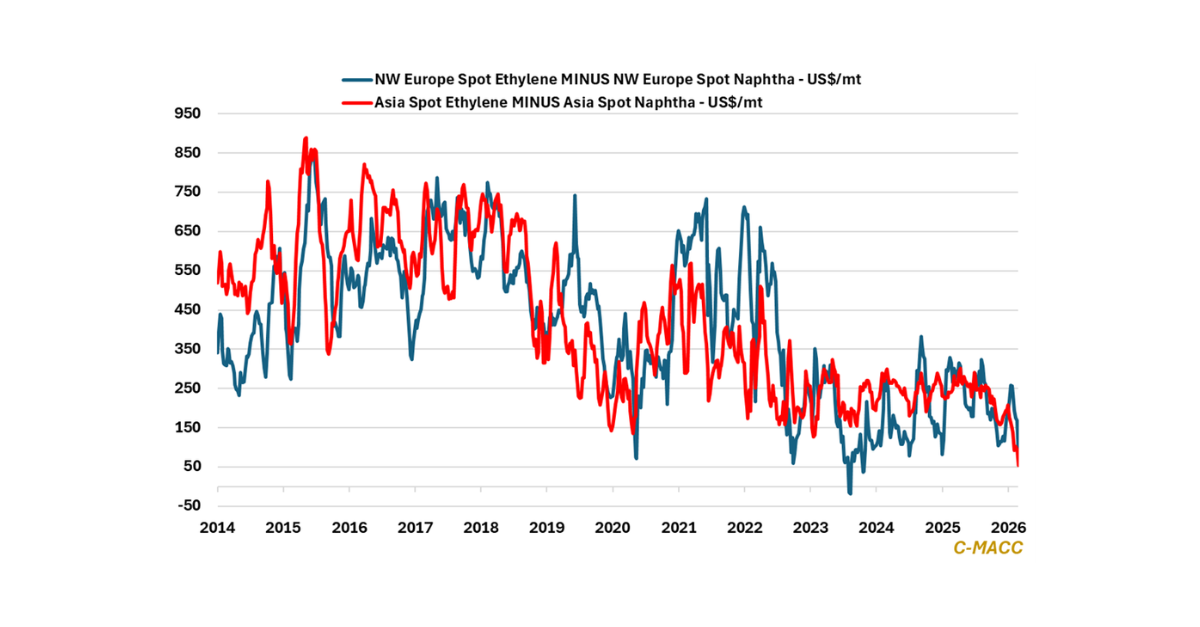

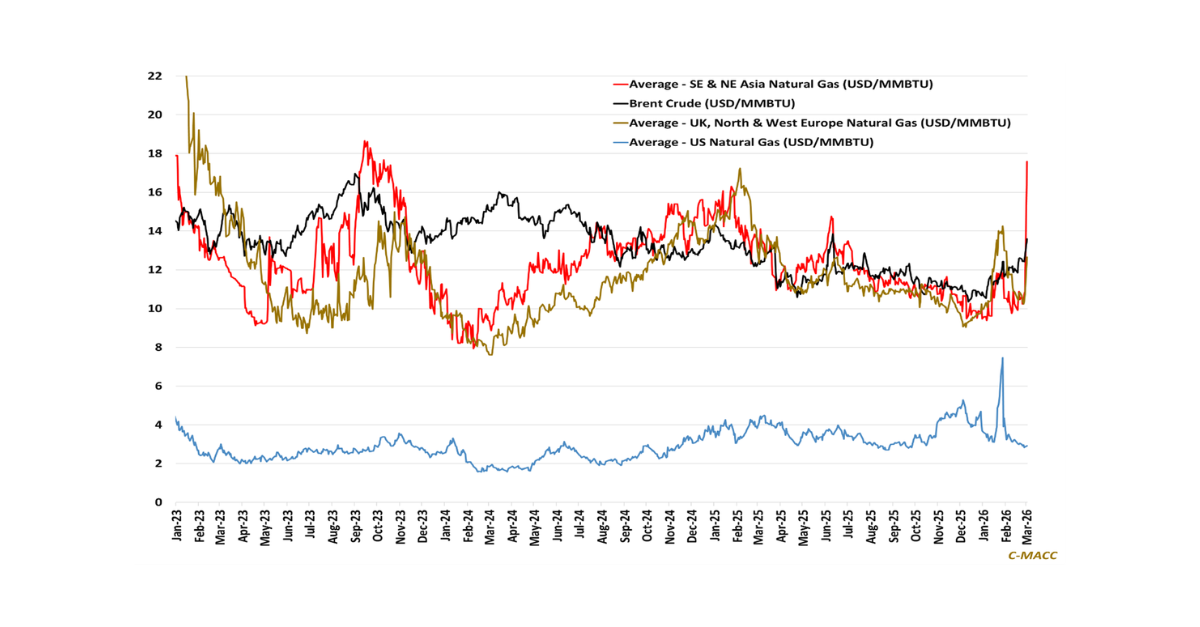

- Surging crude prices and widening feedstock spreads are steepening the global petrochemical cost curve. Cheap regional gas and NGLs may support selective integration, but not a broad new build cycle.

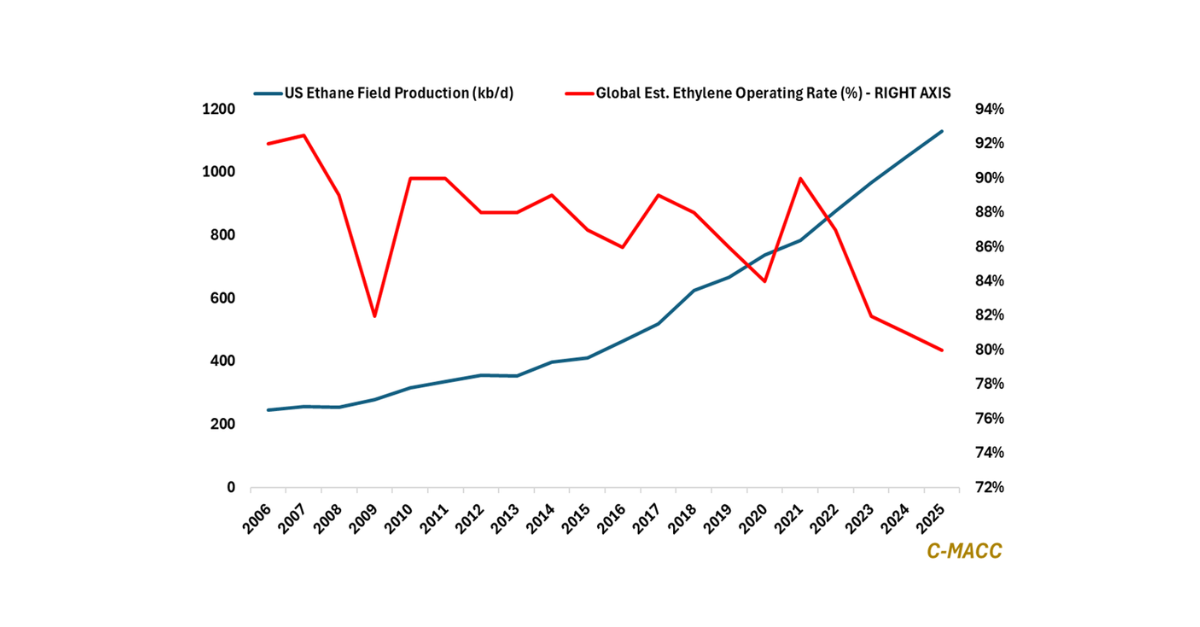

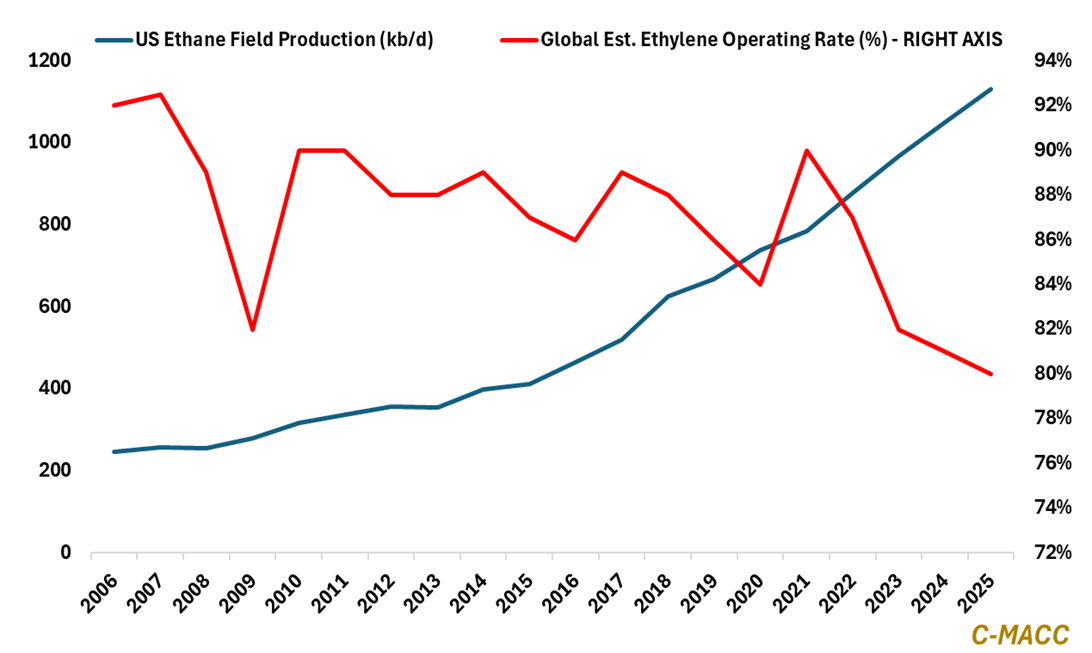

- US ethane supply continues rising rapidly, yet global ethylene operating rates near the low-80% range still signal structural overcapacity and weak incentives for merchant cracker investment.

- US ethane exports, rejection into natural gas streams, and accelerating power-sector gas demand increasingly absorb supply growth before more petrochemical capacity becomes economically necessary.

- The US shale boom and China’s petrochemical expansion helped create today’s surplus capacity, shifting the industry’s challenge toward rationalization, consolidation, and disciplined capital allocation.

- Otherwise, narrowing discounted crude access, widening energy spreads, packaging resilience, ethanol momentum, and slower China growth reinforce restructuring, integration, logistics control, and discipline.

- Companies Mentioned: Shintech, Dow, ExxonMobil, LyondellBasell, Dow, Nova, Westlake, SABIC, Energy Transfer, Enterprise Products, Navigator, GEVO, Green Plains

- Products Mentioned: Ethane, Ethylene, Natural Gas, NGLs, LNG, Crude Oil, Naphtha, LPG, Corn, Ethanol, Gasoline, Sustainable Aviation Fuel, Polyethylene, Polyvinyl Chloride, Methanol, Ammonia

Exhibit 1: Rising US ethane supply has coincided with declining global ethylene operating rates.

Source: Bloomberg, C-MACC Estimates, March 2026

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!