Global Market Analysis

Integrated Wins: Cheap Feedstocks Trump Scale In Global Chemical Shakeout

Key Findings

- General Thoughts: Integration, logistics flexibility, and feedstock advantage are increasingly replacing scale as the chemical sector’s defining competitive edge, steering capital toward integrated production platforms.

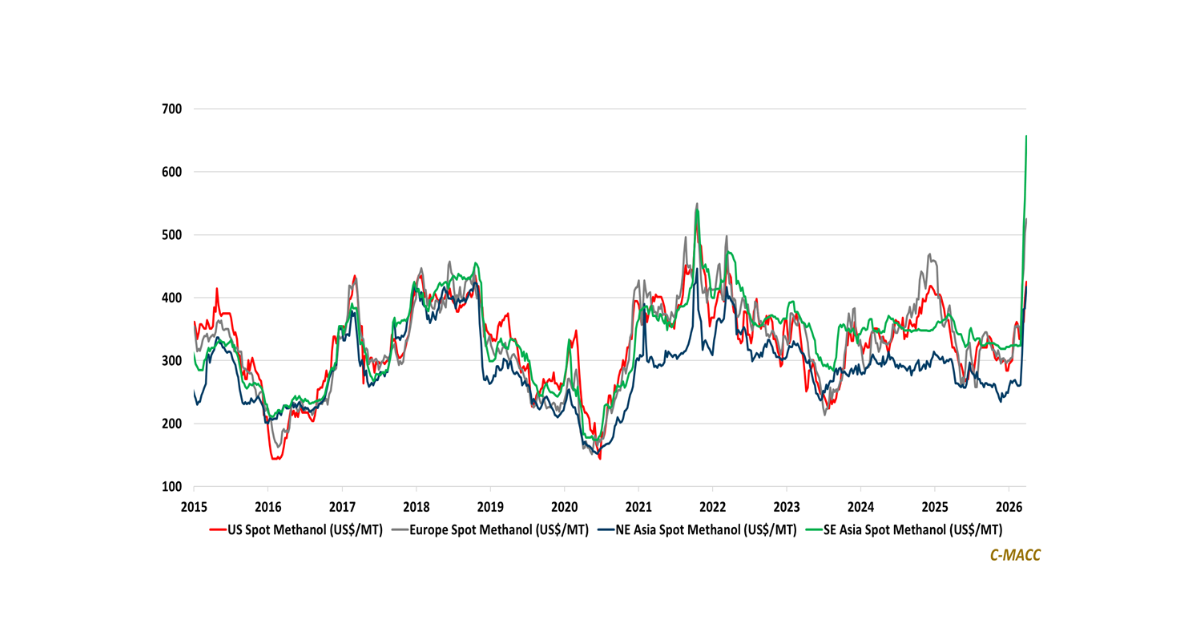

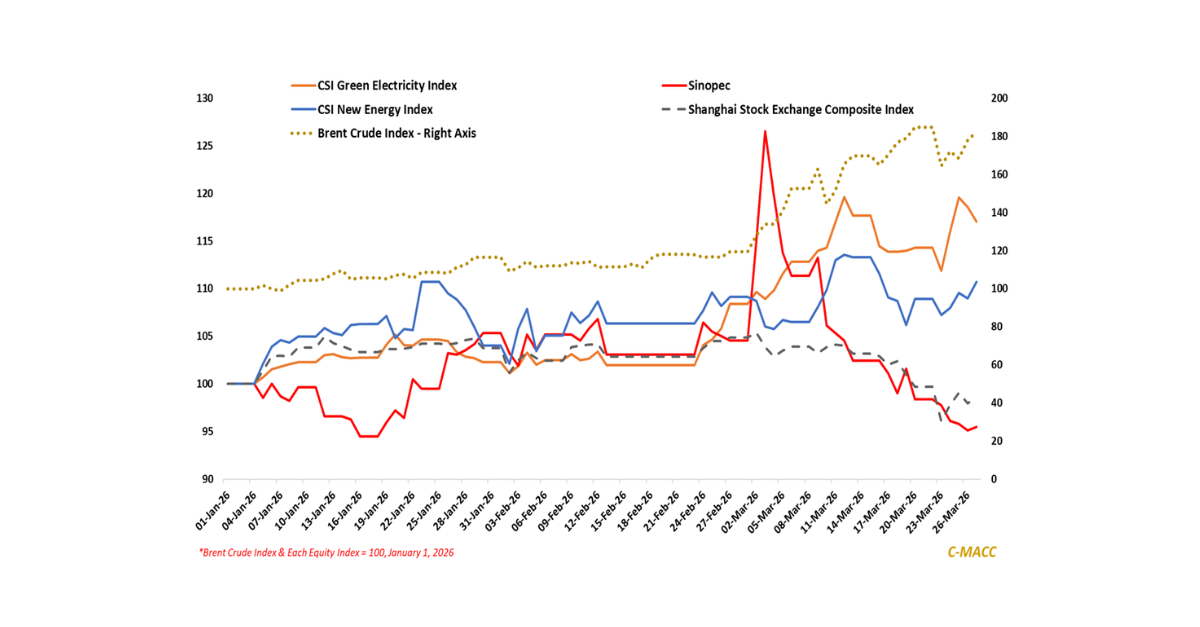

- Supply Chain/Commodities: Surging natural gas price dispersion, Middle East supply risk, and tightening methanol trade flows lift Western methanol premiums and strengthen North America’s feedstock advantage.

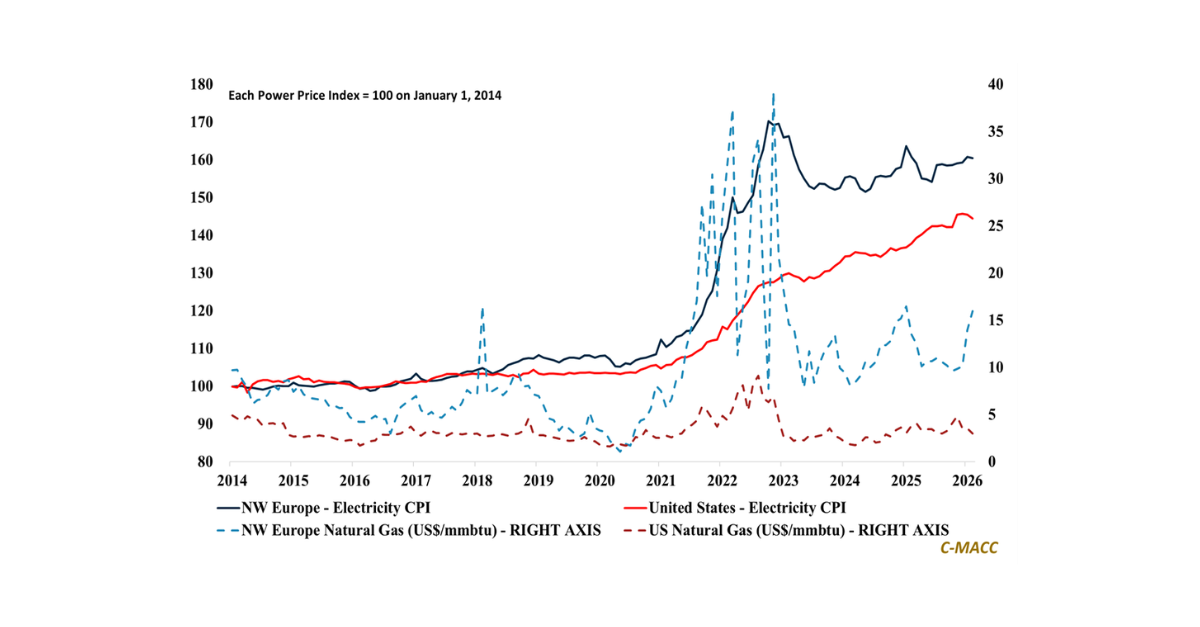

- Energy/Upstream: LNG scarcity is an underappreciated driver of industrial competitiveness, as natural gas prices in Europe and Asia surge further above US levels, steepening chemical cost curves beyond oil trends.

- Sustainability/Energy Transition: Processing capacity now defines lithium supply growth as Smackover brine infrastructure, commodity traders, and energy players converge to accelerate US battery-grade production.

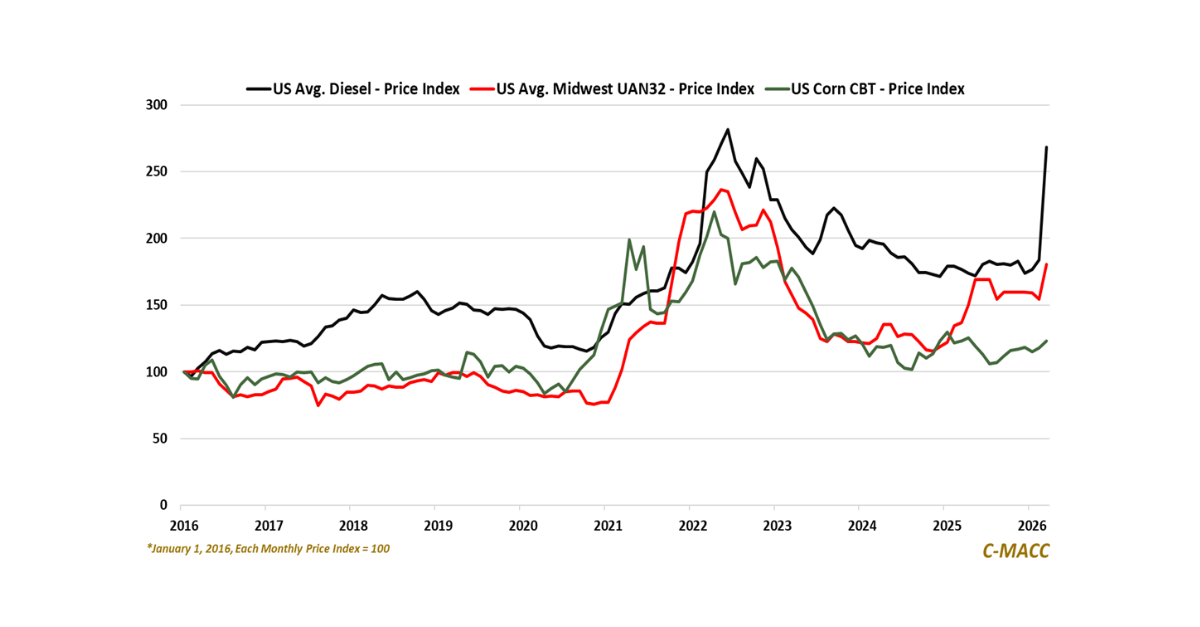

- Downstream/Other Chemicals: Elevated nitrogen fertilizer prices and a ~2.7x soy-corn ratio favor soybean acres, lowering fertilizer use while linking energy markets, crop economics, ethanol demand, and food supply.

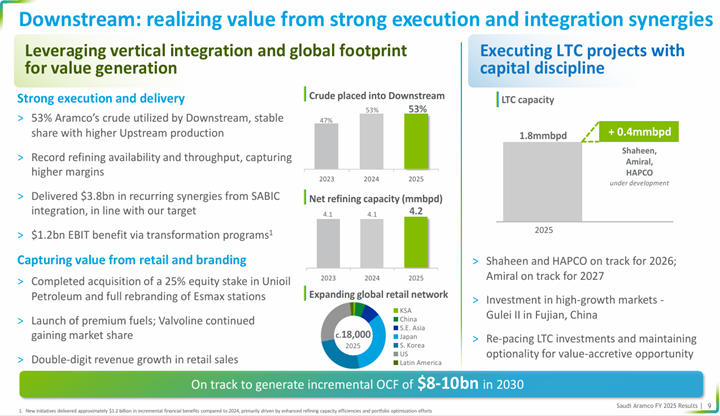

Exhibit 1: Aramco demonstrates how cost advantage and integration outperform sheer scale in chemicals.

Source: Aramco 4Q25 Earnings Call Presentation, March 2026

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!