C-MACC Sunday Executive Summary

System Design Now Determines Chemical Advantage

- Dependable operations now define competitive advantage, with non-integrated assets losing ground as fragility disrupts throughput, raises risk, and weakens returns under stress.

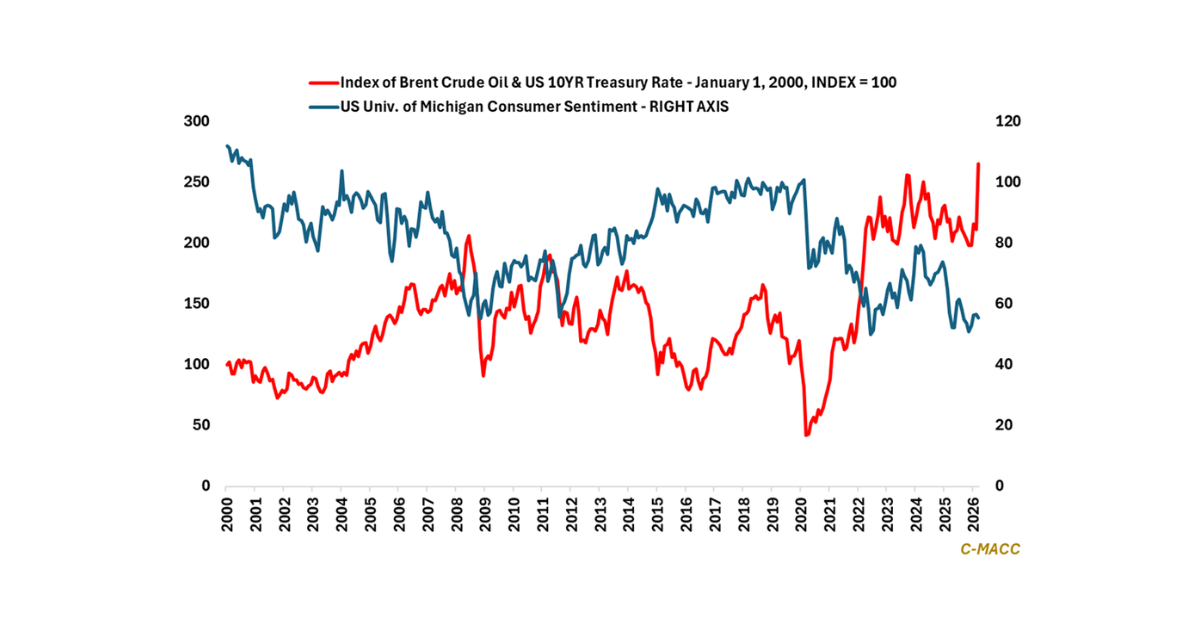

- Oil-linked feedstock systems import persistent volatility into cost structures, shifting advantage toward integrated energy architectures that absorb shocks across power, natural gas, and logistics.

- Capital shifts away from exposed assets toward durable hydrocarbon and infrastructure systems as higher return thresholds constrain reinvestment and discourage marginal capacity expansion.

- Demand recovery will not rescue weak portfolios, as selective end-market strength widens divergence between feedstock-secure assets and those unable to sustain returns through cycles.

- Otherwise, tightening feedstocks, freight disruption, LNG inflexibility, and power constraints are converging to reprice industry economics, shifting capital and capacity toward feedstock-secure systems.

- Companies Mentioned: Braskem, ExxonMobil, Wacker Chemie, Lanxess, Envalior, BP, ADNOC, OMV, Borouge Group International, Heartland Polymers, Dow, Invista, Enterprise, Delta Air Lines, 3M, Maersk, CMA CGM, COSCO

- Products Mentioned: Polypropylene, Propylene, Methanol, Propane, Ethane, NGLs, Ammonia, Hydrogen, Naphtha, LNG, Natural Gas, Electricity, Crude Oil, Gasoline

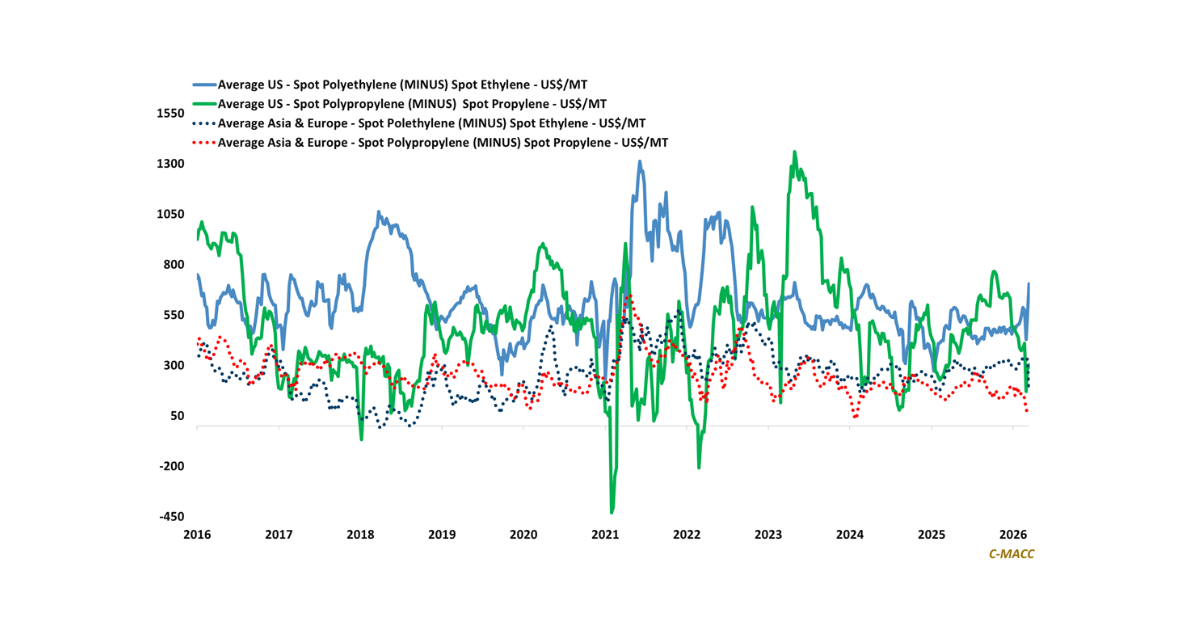

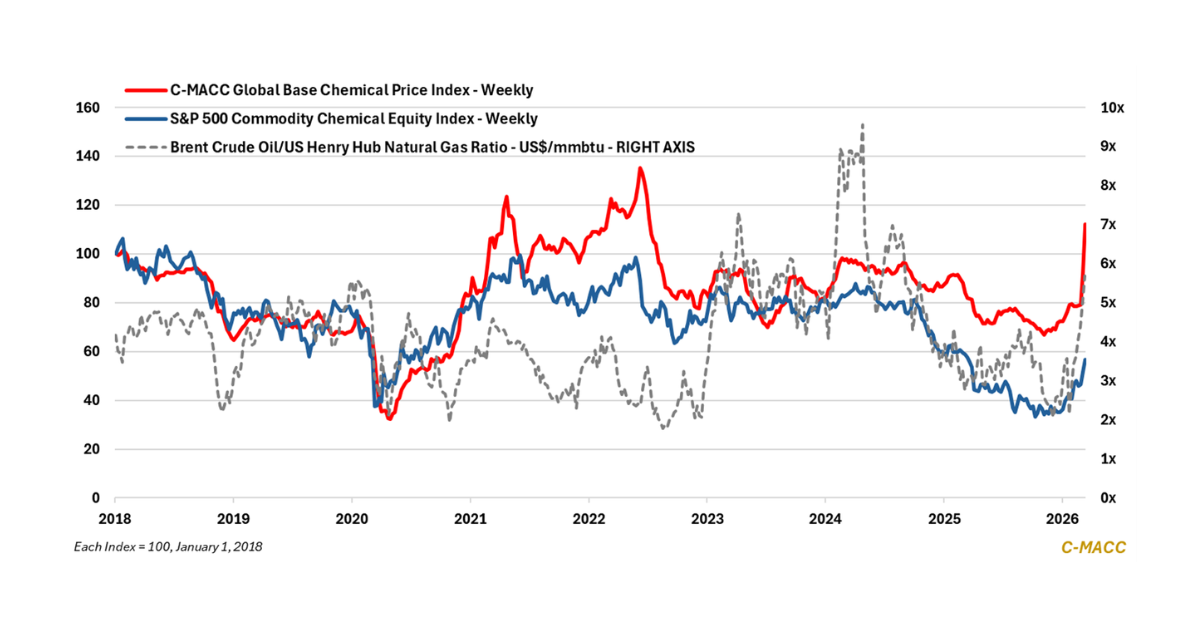

Exhibit 1: Non-integrated polymer margins remain compressed outside feedstock-secure, coordinated systems.

Source: Bloomberg, C-MACC Analysis, March 2026

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!