Base Chemical Global Analysis

Global Weekly Catalyst No. 323

- General Thoughts: Energy divergence, supply disruption, and logistics risk are forcing a structural shift toward integrated, feedstock-secure systems as merchant models lose reliability and margin resilience.

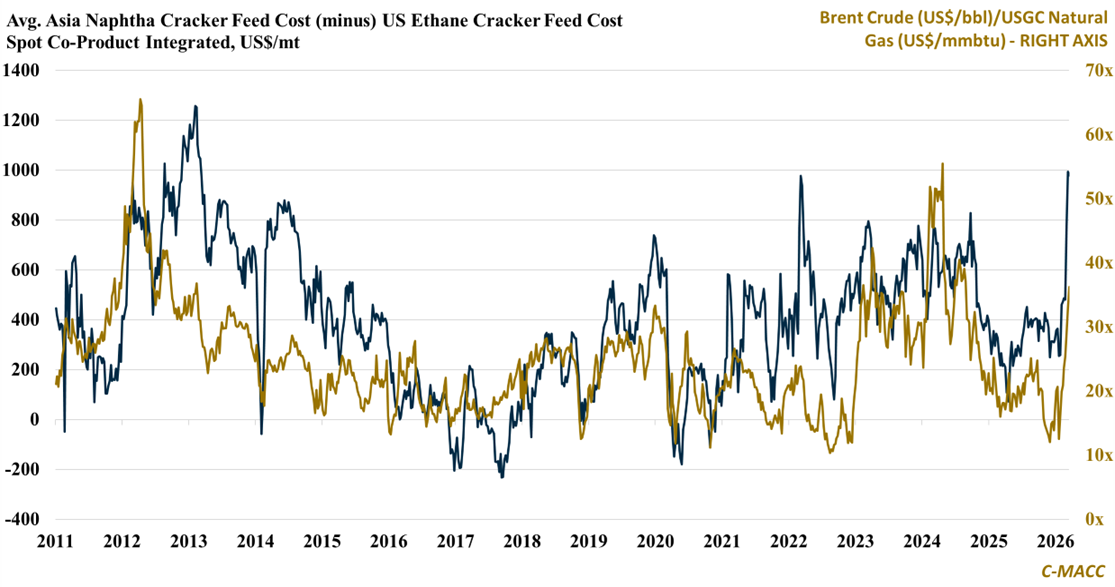

- Feedstocks & Energy: Widening oil and gas spreads are resetting global cost curves, concentrating advantage in North America and structurally impairing import-dependent systems across Europe and Asia.

- Olefins: Asian operating cuts and higher naphtha costs are reducing effective supply, shifting pricing power toward feedstock-advantaged producers and undermining prior assumptions of persistent oversupply.

- Other Base Chemicals: Rising methanol and benzene prices are shifting margins upstream, benefiting integrated producers while compressing downstream profitability for merchant buyers exposed to volatile replacement costs.

- Agriculture: Nitrogen price escalation, driven by export restrictions and divergent gas costs, is raising global crop input risk and reinforcing structural competitiveness for North American ammonia producers.

- Refining & Biofuels: Tight product balances and stronger blending economics are expanding refinery and ethanol margins, reinforcing fuels as the primary channel for monetizing global energy dislocation.

Exhibit 1 – Chart of the Day: Asian naphtha cracker margins collapse as the US ethane advantage widens structurally.

Source: Bloomberg, C-MACC Estimates, March 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!