Global Market Analysis

Record Year: Chemical Producers Run For Safety, As Capital Selectively Walks Away

Key Findings

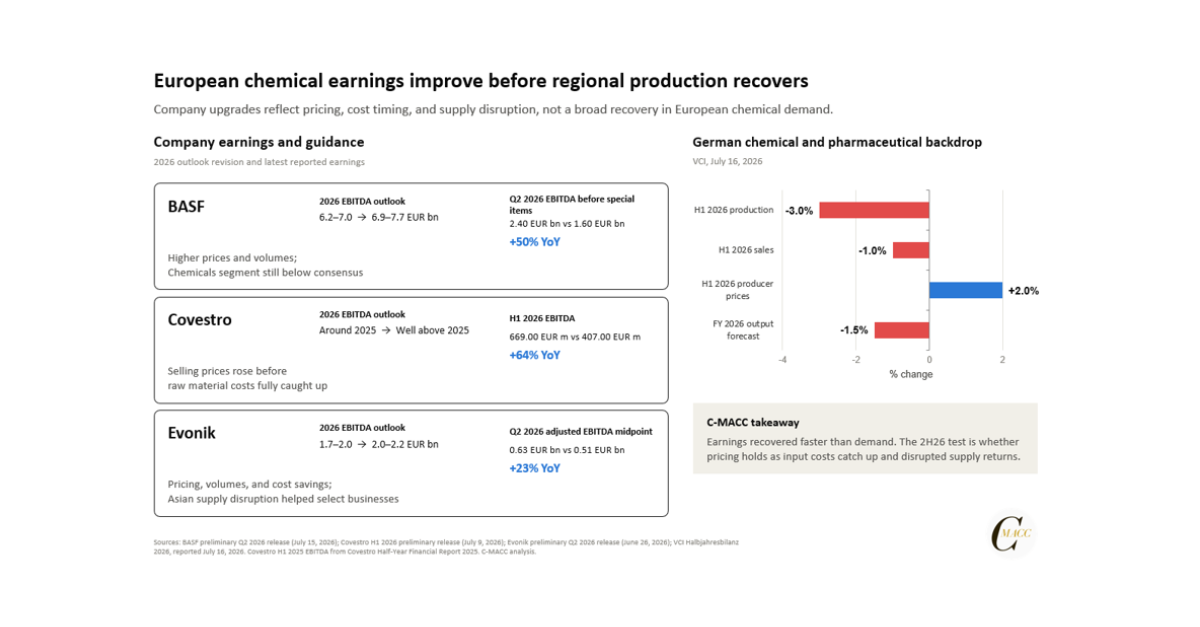

- General Thoughts: Supply shocks are shifting power from cost to control, concentrating value in integrated systems as export-driven convergence reshapes demand, margins, and capital allocation plans globally.

- Supply Chain/Commodities: USGC ethane and ethylene exports reward midstream and export infrastructure with global optionality while driving cost convergence and diluting US chemical cost advantages over time.

- Energy/Upstream: Regional gas price dislocations are concentrating capital in low-cost integrated systems, while uncertainty around long-term offtake contracting and demand visibility is constraining new investment.

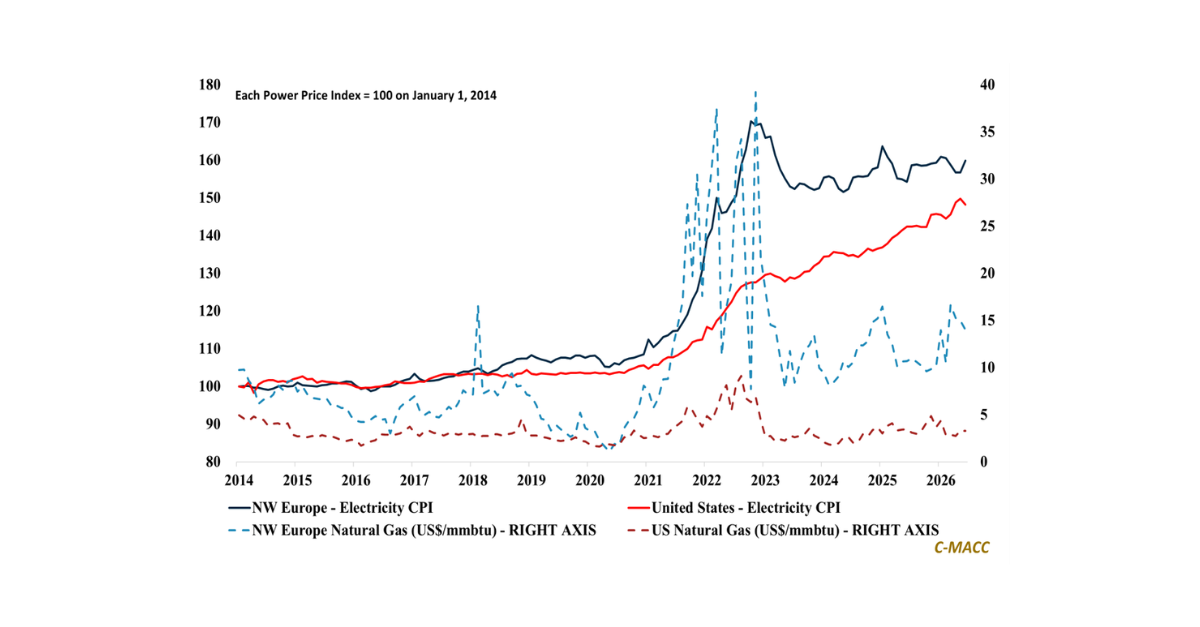

- Sustainability/Energy Transition: High Asian and European LNG prices support North American exporters but risk delaying decarbonization as cost-driven switching sustains coal demand across high-cost regions.

- Downstream/Other Chemicals: Energy policy momentum and fertilizer inflation are driving acreage shifts, but resilient biofuel demand and constrained inputs keep corn and soybeans tilted toward tighter balances.

Exhibit 1: Supply shocks are shifting power from cost to control across global markets.

Source: H.B. Fuller – 1QFY26 Earnings Presentation, March 2026

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!