Base Chemical Global Analysis

Global Weekly Catalyst No. 324

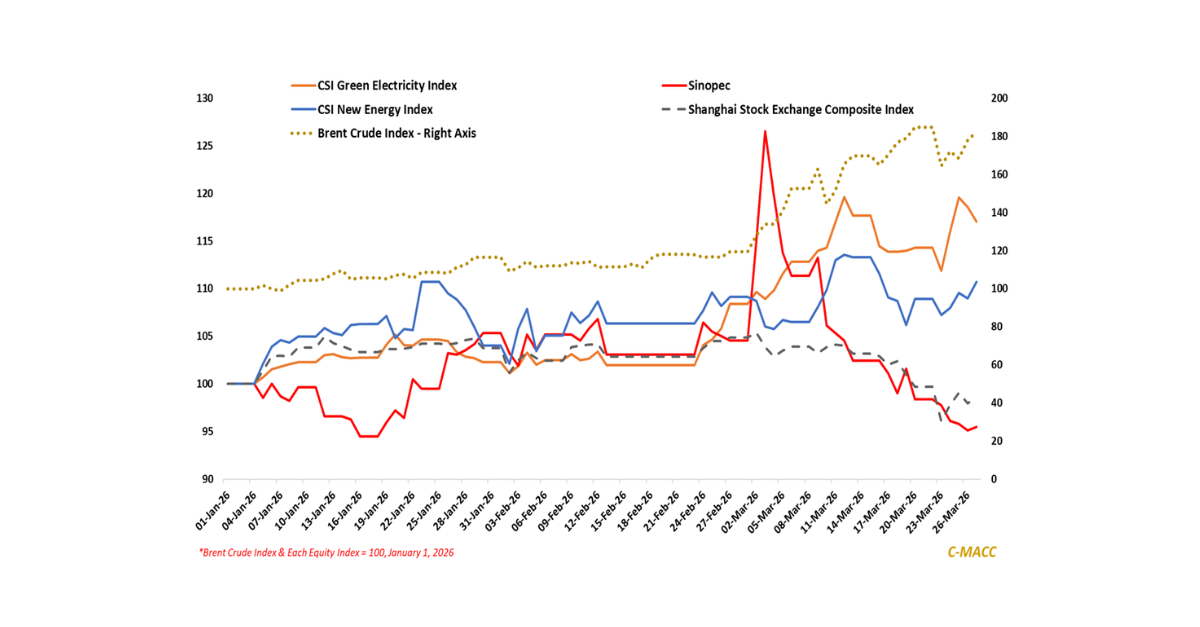

- General Thoughts: Global industrial markets have fractured into parallel pricing regimes where cost, logistics, and access determine outcomes. Markets are no longer clearing globally; they are clearing locally under constraint.

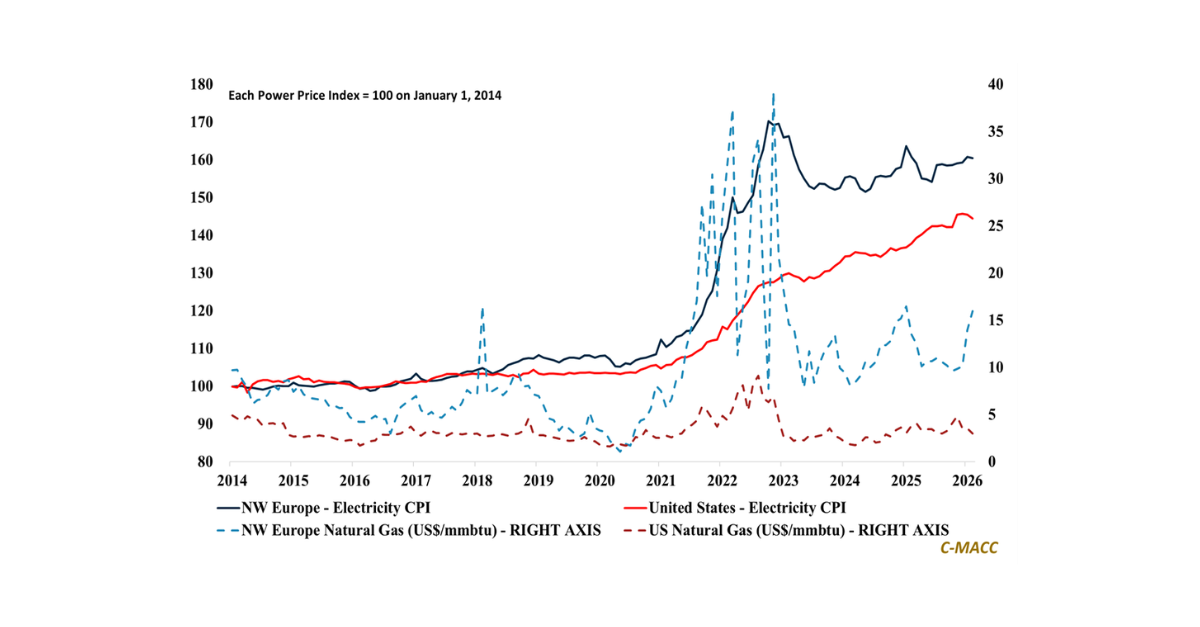

- Feedstocks & Energy: Global feedstock divergence is hardening into a structural capital filter, concentrating margins in gas-advantaged systems as oil-linked inflation and logistics risk extend cost curve dislocation into 2Q26.

- Olefins: Effective olefin supply is constricting at a system level, as feedstock shocks and operating constraints shift pricing power toward advantaged exporters and accelerate rationalization across high-cost assets globally.

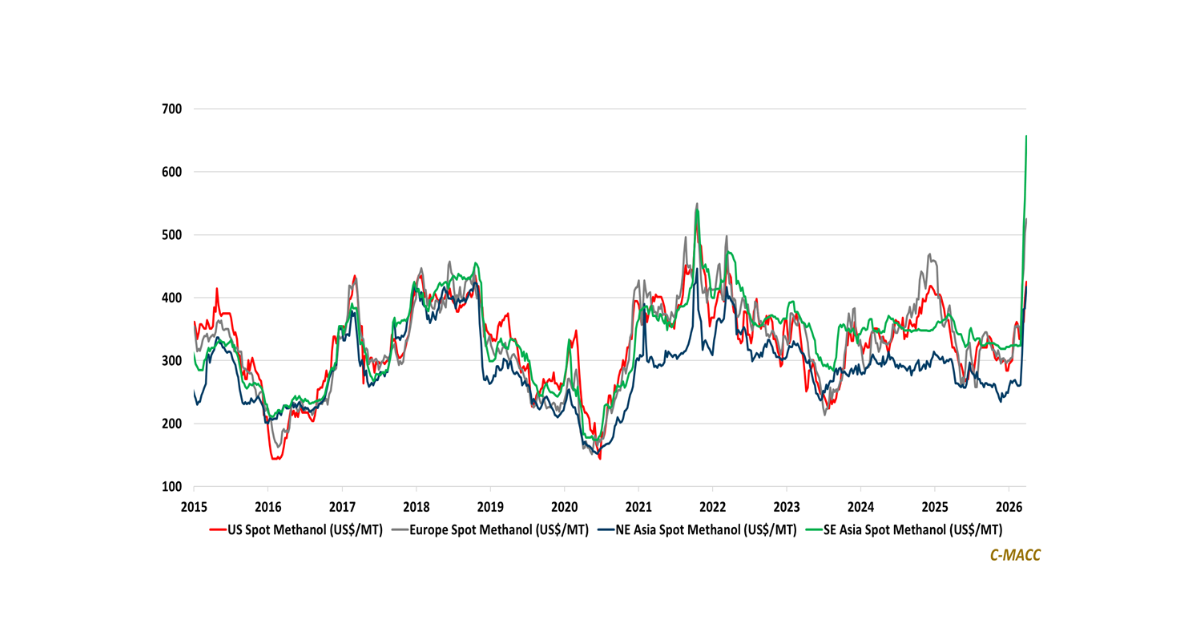

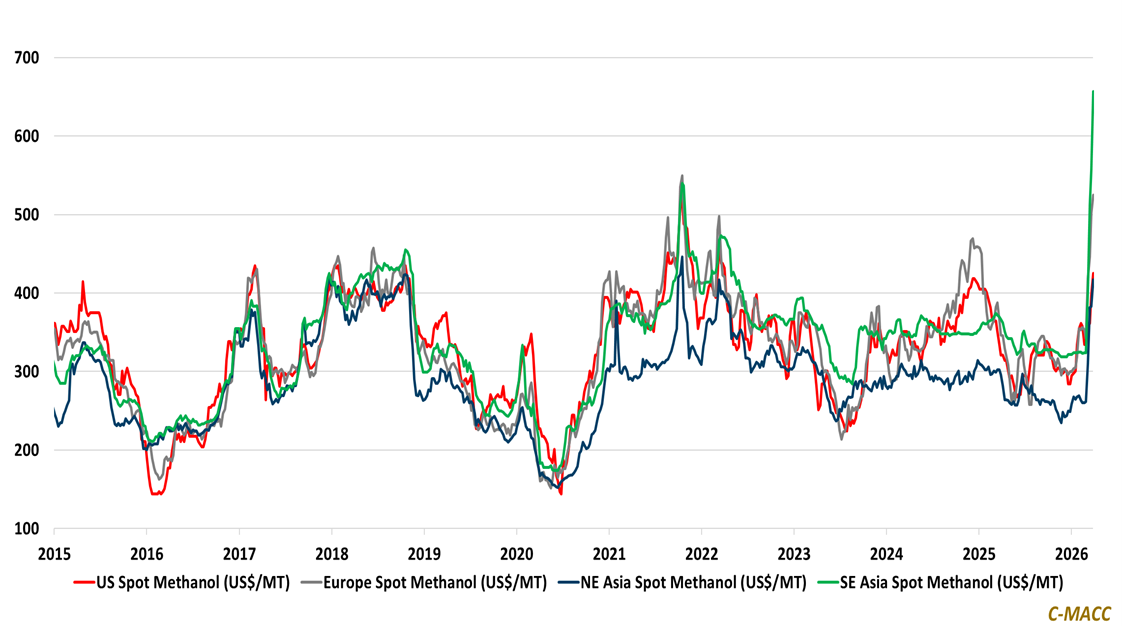

- Other Base Chemicals: Upstream strength is shifting margins decisively toward integrated base chemical producers, as tightness in methanol, benzene, and chlor-alkali amplifies cost divergence and exposes weak merchant demand.

- Agriculture: Nitrogen markets are tightening sharply, as export controls, diverging gas costs, and logistics risks push ammonia prices higher, eroding farm margins and elevating global food price risk.

- Refining & Biofuels: Product tightness and policy acceleration are concentrating value across refining and biofuel chains, as rising mandates, strong cracks, and feedstock demand reshape margin leadership globally.

Exhibit 1 – Chart of the Day: Methanol dislocations expose break between advantaged systems and import markets.

Source: Bloomberg, C-MACC Estimates, March 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!