Base Chemical Global Analysis

Global Weekly Catalyst No. 325

- General Thoughts: Global industrial markets are no longer equilibrating through trade, as constrained logistics and feedstock access prevent arbitrage from normalizing regional price dislocations across systems.

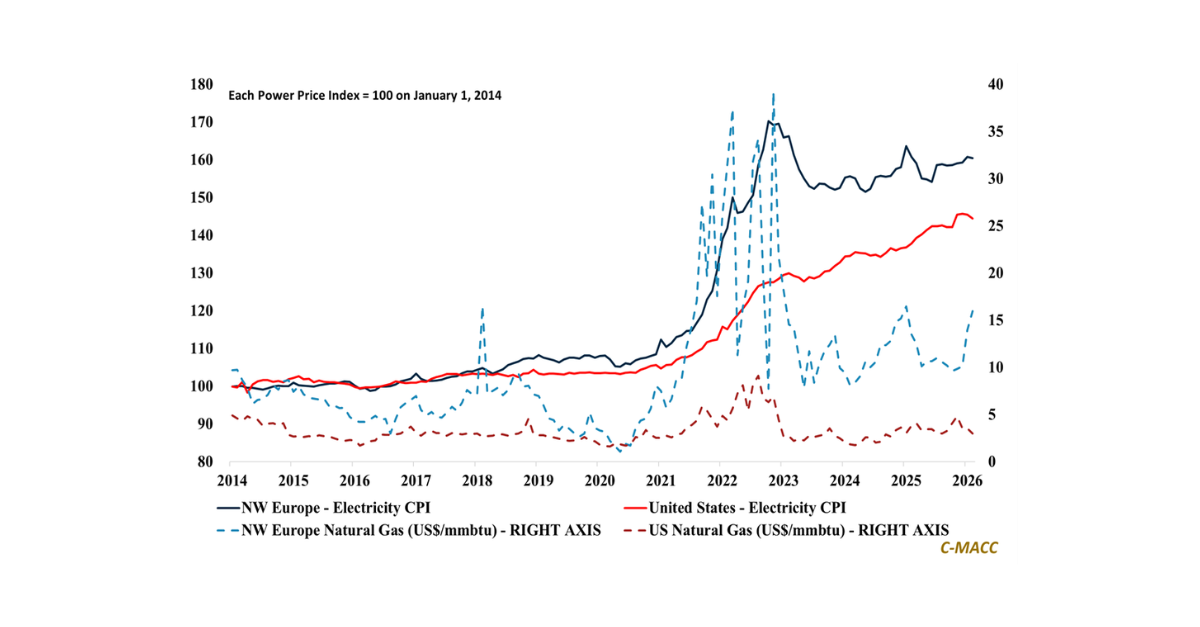

- Feedstocks & Energy: Oil-linked petrochemical feedstock inflation and logistics constraints are resetting global cost curves, concentrating margins in gas-advantaged systems, and shaping industrial competitiveness through 2Q26.

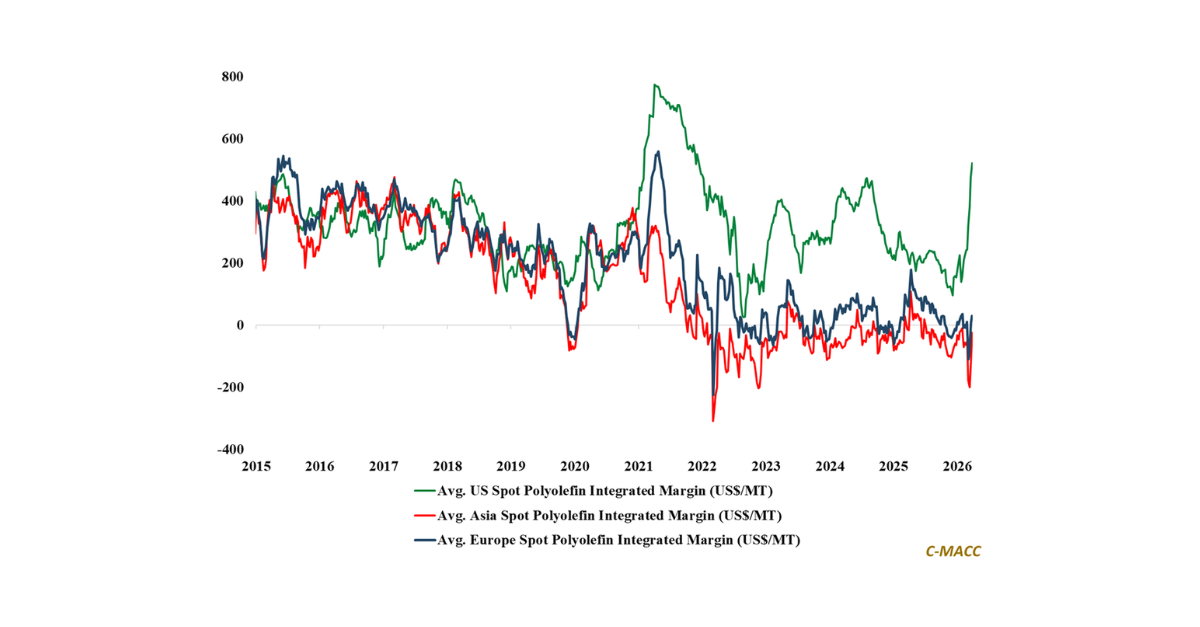

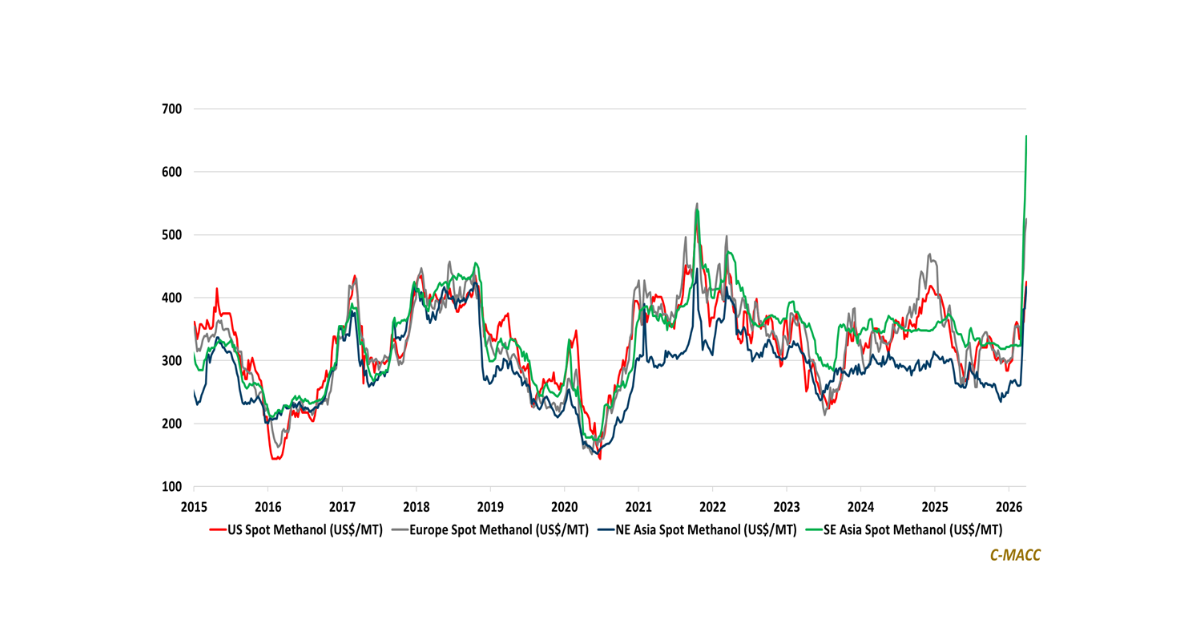

- Olefins: Forward global supply assumptions look overstated, as constrained operability, delayed restarts, and restructuring compress effective capacity and shift pricing influence toward those with durable feedstock access.

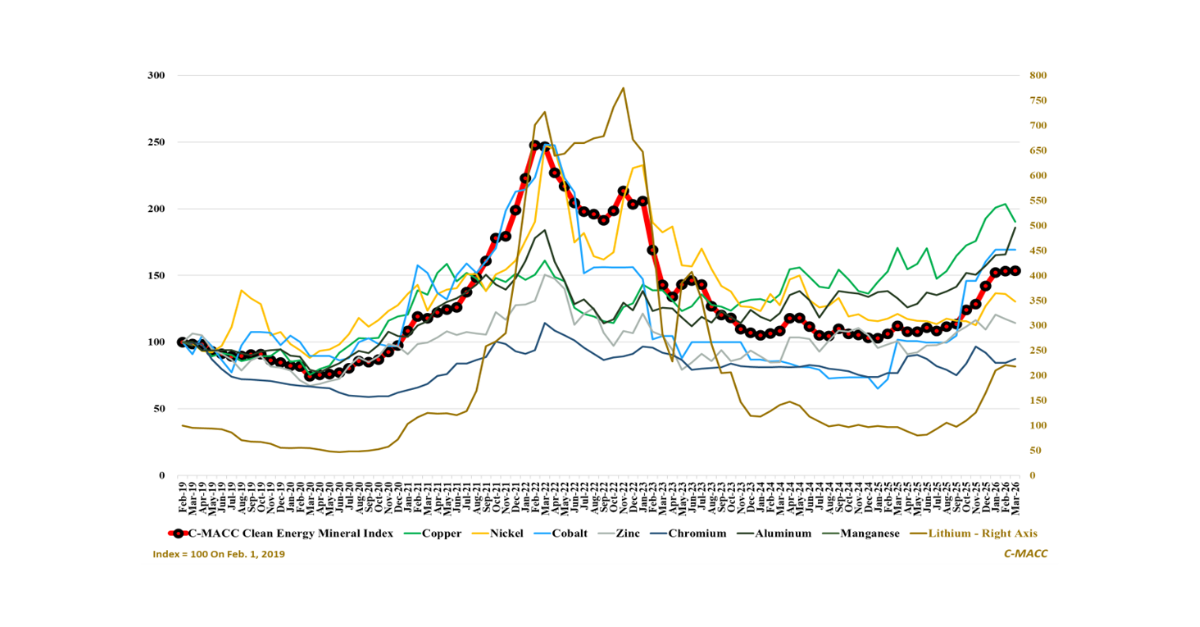

- Other Base Chemicals: Global base chemical margins are shifting upstream, becoming increasingly feedstock- and power-driven, forcing downstream demand elasticity and exposing structural limits to cost pass-through.

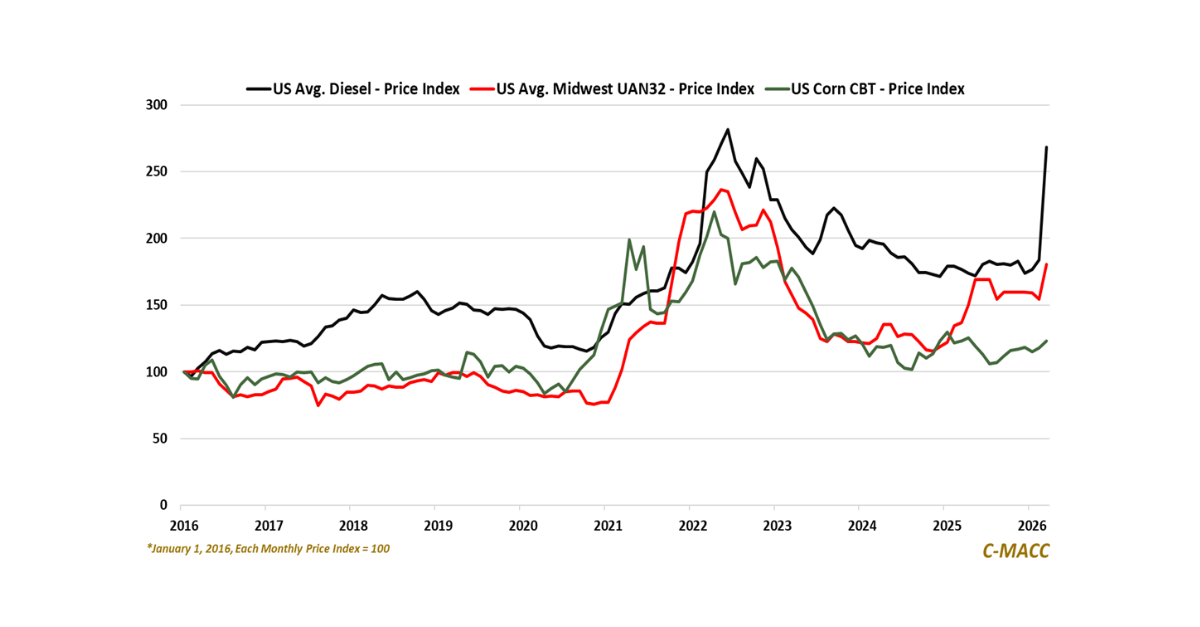

- Agriculture: Nitrogen availability is increasingly setting agricultural demand, as affordability constraints force earlier procurement, lower application intensity, and widening divergence in crop economics globally.

- Refining & Biofuels: Global refining and biofuel value pools are expanding in tandem, as product scarcity and policy-driven demand align to reward integrated systems with flexibility across fuels and agricultural inputs.

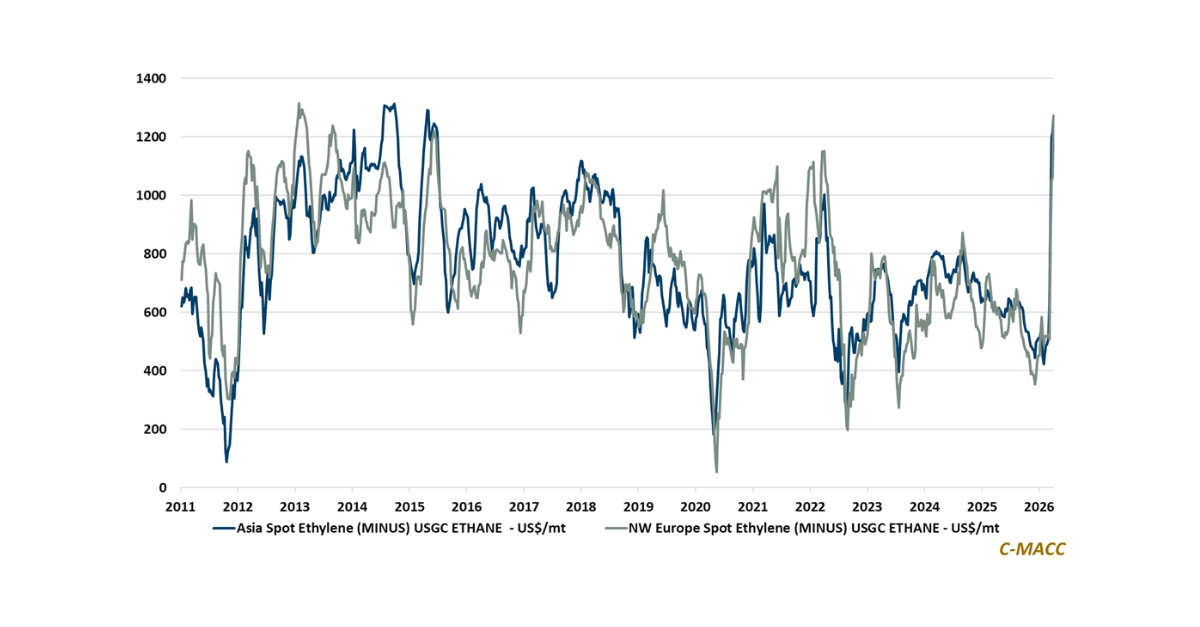

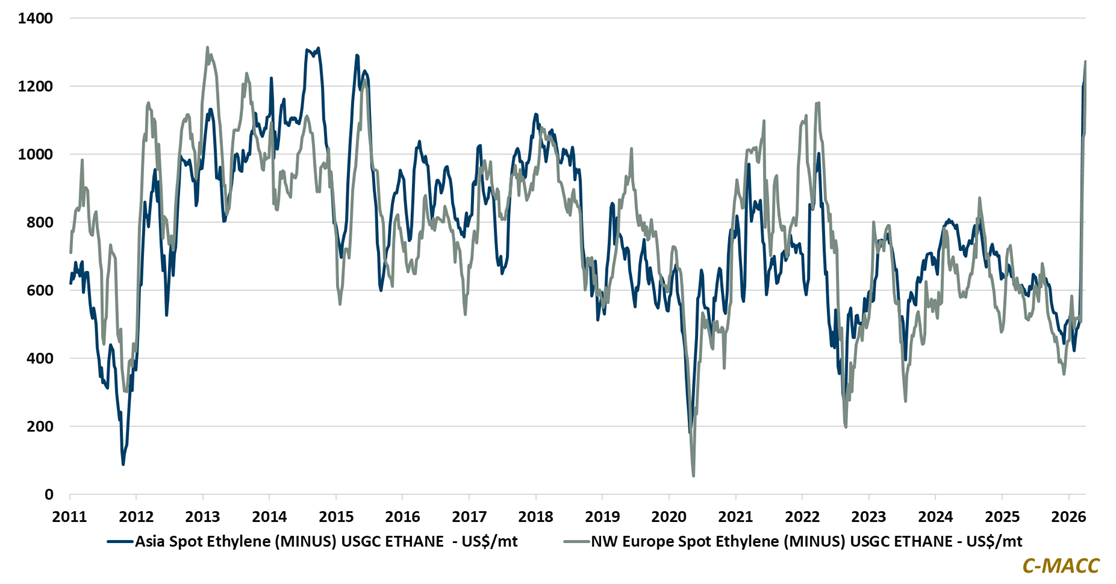

Exhibit 1 – Chart of the Day: Asian and European spot ethylene decouples from USGC ethane cost advantage.

Source: Bloomberg, C-MACC Estimates, April 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!