Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

- General Thoughts: Volatility is rewarding integrated reach as feedstock dislocation, shipping delays, and buyer hesitation favor sustained pricing power while delaying physical market normalization despite ceasefire headlines.

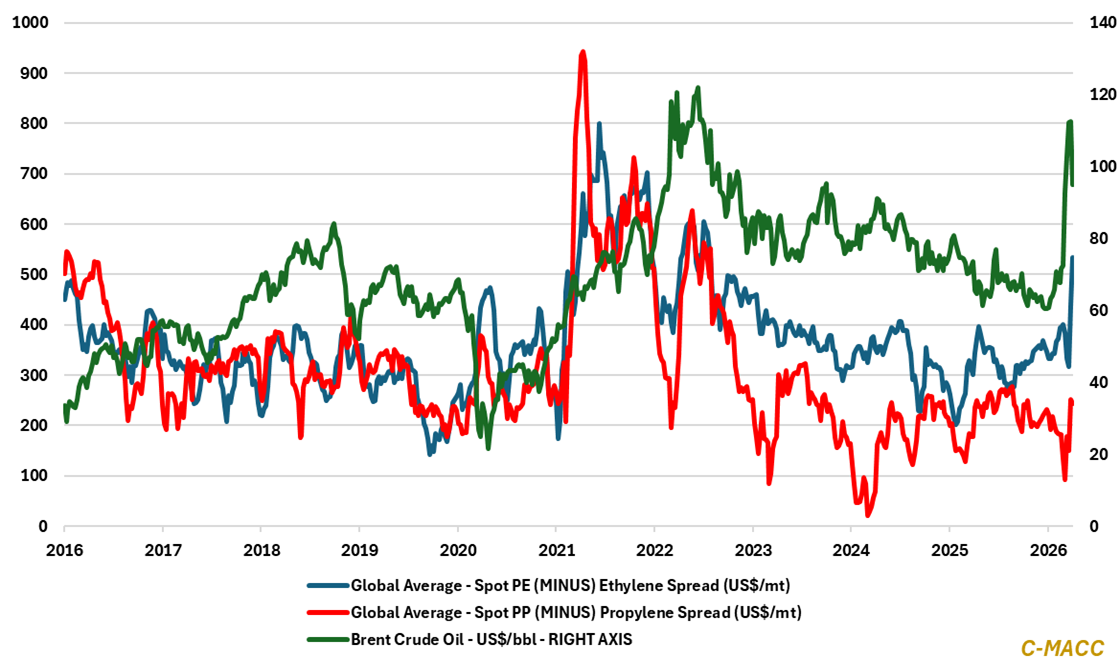

- Polyethylene (PE): Global PE pricing is being set by cost curve shifts and the unwind of early-year buyer overconfidence, as outages and delayed arrivals support strength while trade friction and export optionality increasingly cap upside.

- Polypropylene (PP): Global PP pricing is being set by propylene dislocation, with outages steepening the cost curve and rapidly widening margin dispersion across regions, reinforcing integrated producer advantage globally.

- Polyvinyl Chloride (PVC): Global PVC pricing is being capped by carbide-based competition, as supply tightness fails to offset affordability pressure and substitution into lower-cost material, where specs allow, across global markets.

- Other Sector Developments: Ceasefire-driven declines in energy and feedstocks will only feed through with a lag, as logistics, insurance, and availability constraints delay normalization across physical markets absent further disruption.

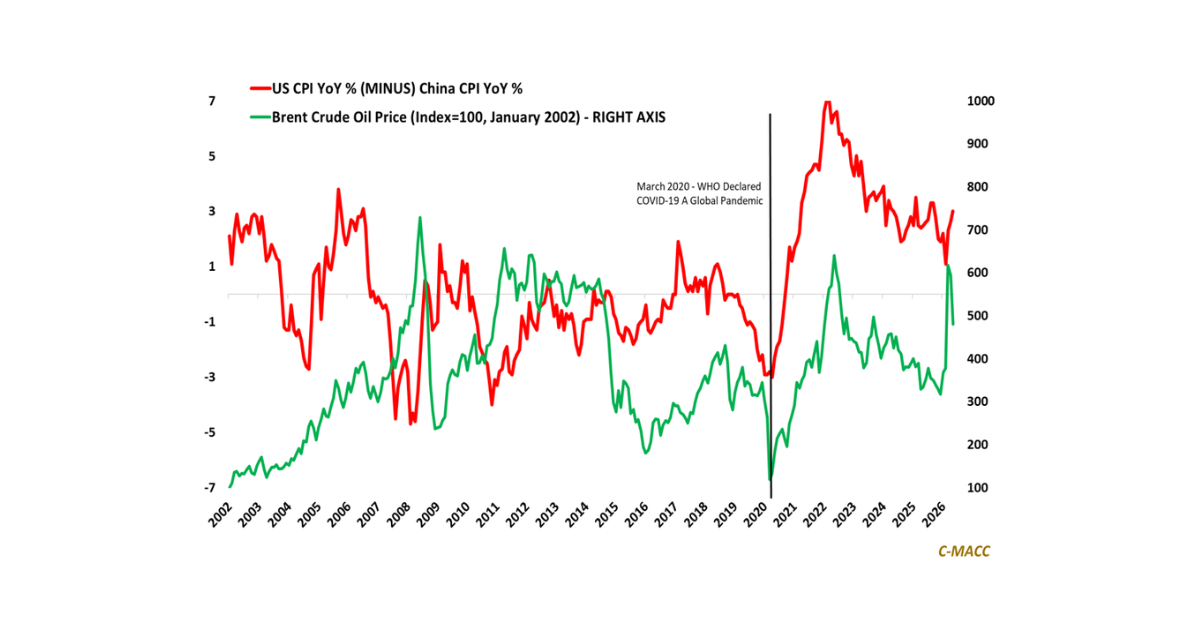

Exhibit 1 – Chart of the Day: Crude moves first, margins follow later as timing gaps shift polymer economics globally.

Source: C-MACC Estimates & Analysis, April 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!