C-MACC Sunday Executive Summary

Factory Reset? China’s Prices Rise & Cheap Relief Leaves the Building

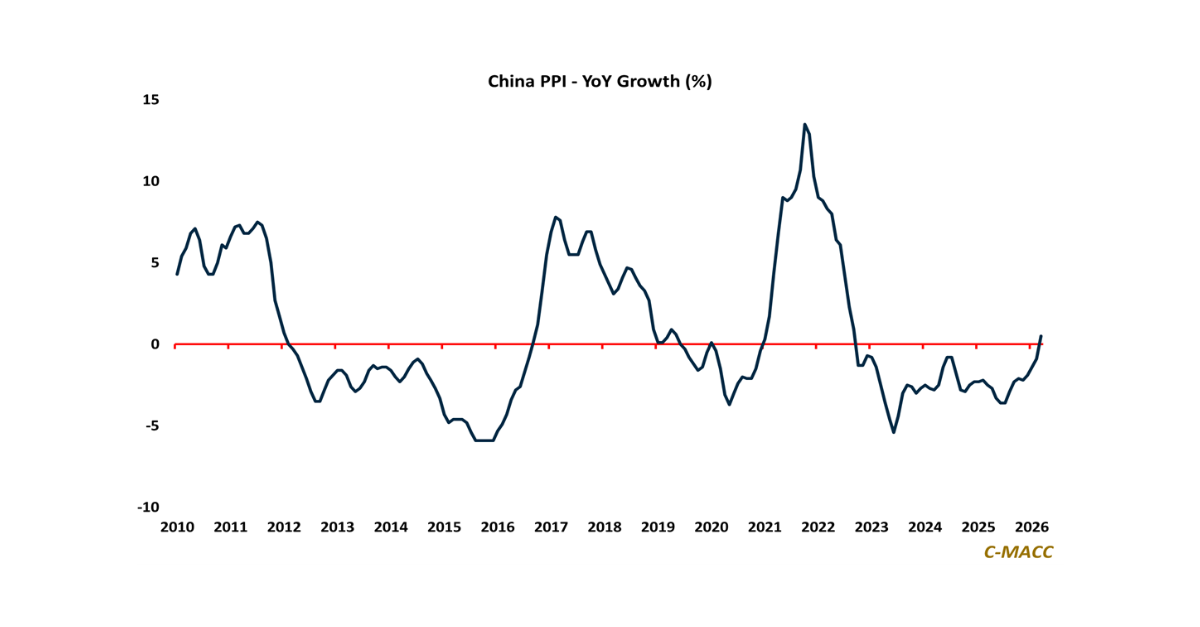

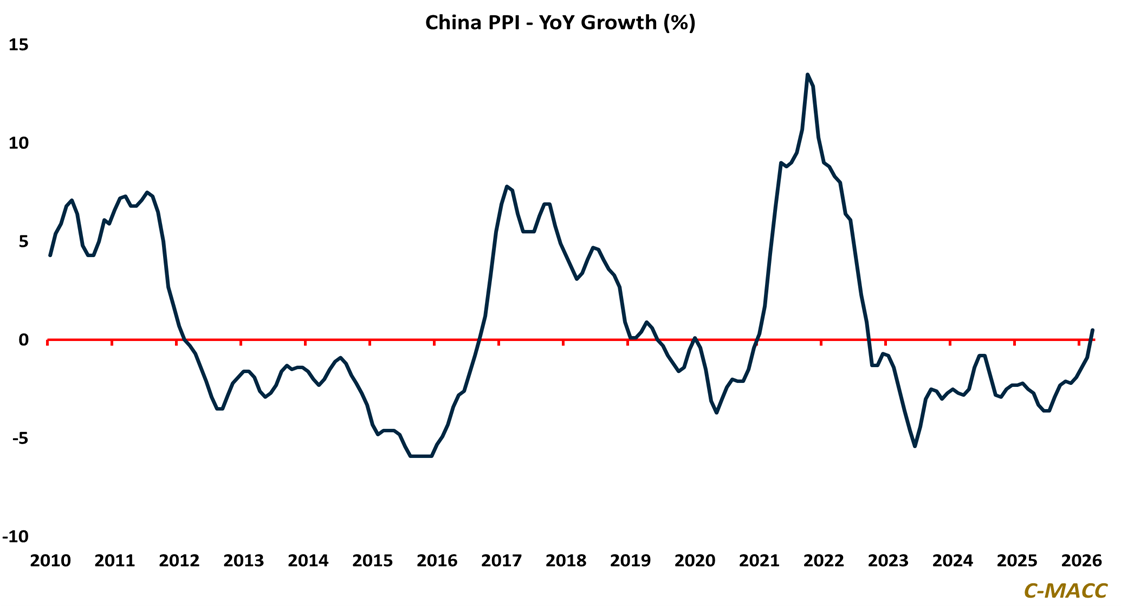

- China’s 0.5% YoY factory-gate inflation in March removed a trusted global relief valve, forcing markets to underwrite firmer resin and intermediate floors, slower cost deflation, and less dependable trade relief.

- Beijing’s refining and chemical restructuring is not a retreat but a directed reallocation toward advantaged assets, rewarding feedstock access, logistics control, and policy-aligned optionality across value chains.

- Western chemical producers that expanded exposure to China to capture growth now face a harsher equation: tepid demand, higher costs, and returns increasingly unlikely to clear original return thresholds.

- The next twelve months should reward US ethane, selective coal-advantaged Chinese chains, and flexible regional operators, while exposing oil-linked systems still built on broad Chinese disinflation assumptions.

- Otherwise, procurement depth, feedstock routing, and power certainty are separating winners from volume holders as cost shocks expose weak buffers across industrial systems.

- Companies Mentioned: ExxonMobil, LyondellBasell, BASF, Sinopec, Flint Hills, Enterprise, PPG Industries, Braskem, Pinnacle Polymers, RPM International, H.B. Fuller, Sherwin-Williams, Axalta Coating Systems, Sika, Pembina Pipeline, Reliance Industries, WhiteWater, MPLX, Enbridge, Energy Transfer, Kinder Morgan, Chevron, Alcoa, Metlen, Glencore, Ford, General Motors, Dow, Westlake

- Products Mentioned: Oil, Ethylene, Naphtha, Ethane, Coal, Propylene, Polypropylene, LPG, Propane, Natural Gas, LNG, Aluminum, Power

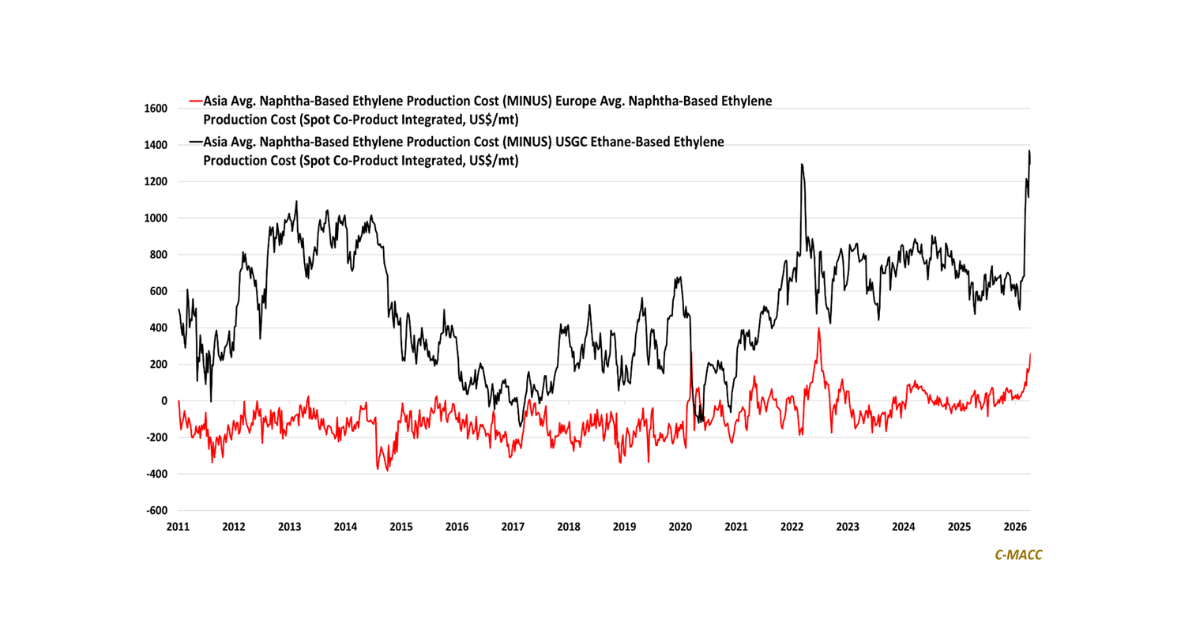

Exhibit 1: China stops exporting easy disinflation as energy and policy raise global chemical floors.

Source: Bloomberg, C-MACC Analysis, April 2026

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!