Base Chemical Global Analysis

Global Weekly Catalyst No. 326

- General Thoughts: Reliable access to inputs and delivery is overtaking cost advantage for producers and buyers, as constrained flows and logistics risk expose mispriced capacity, compress margins, and shift pricing power.

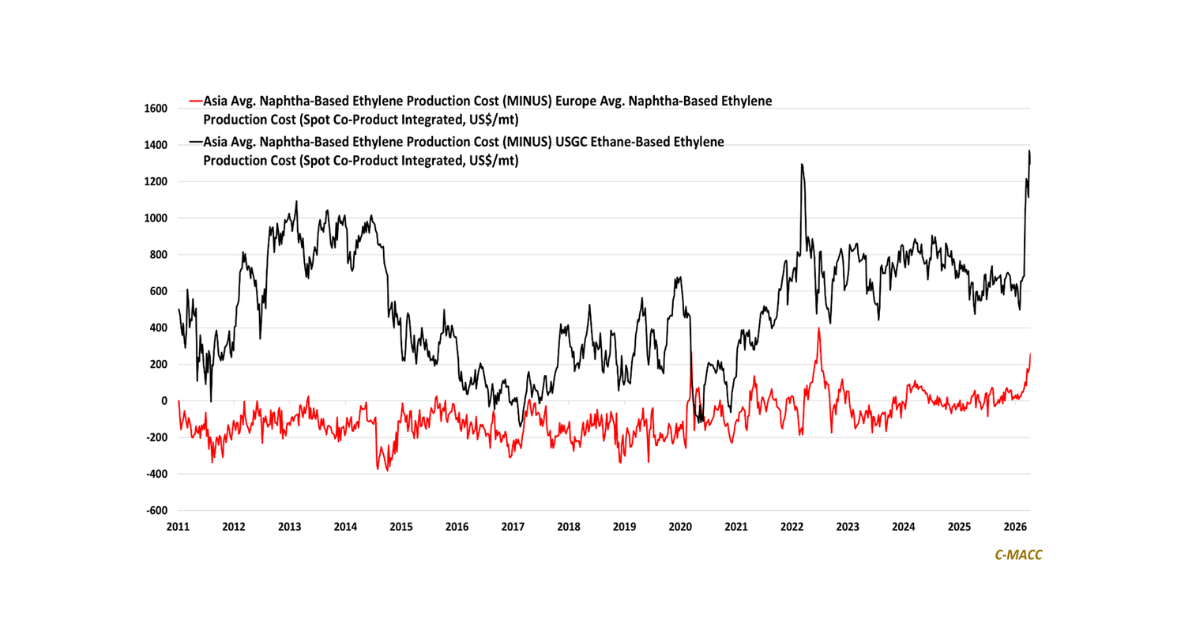

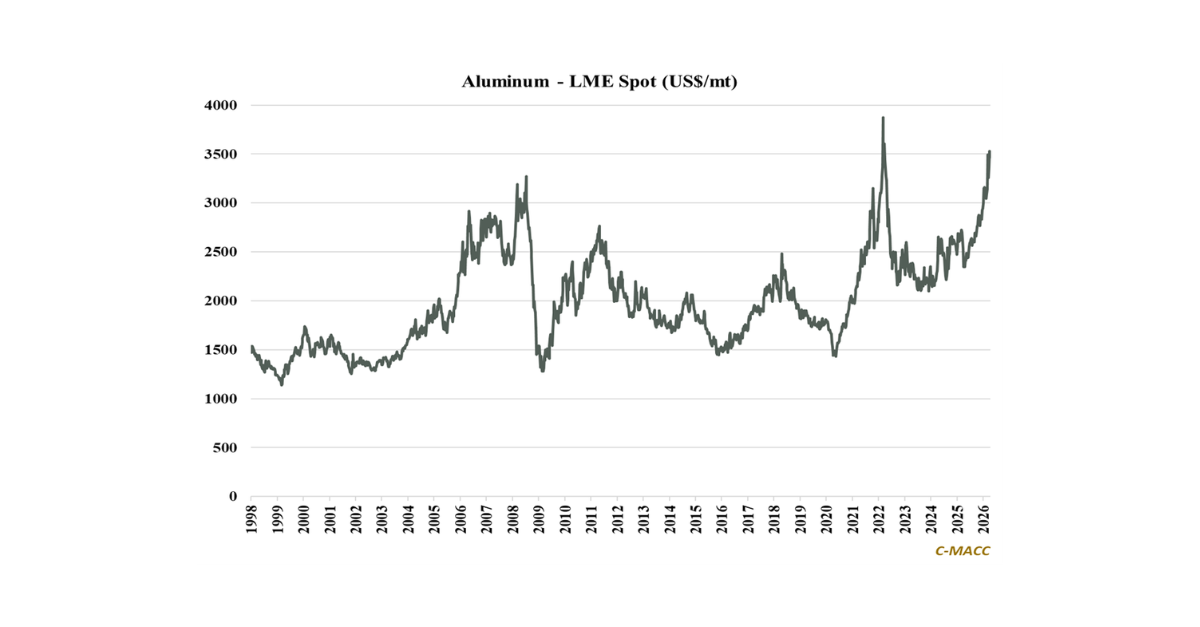

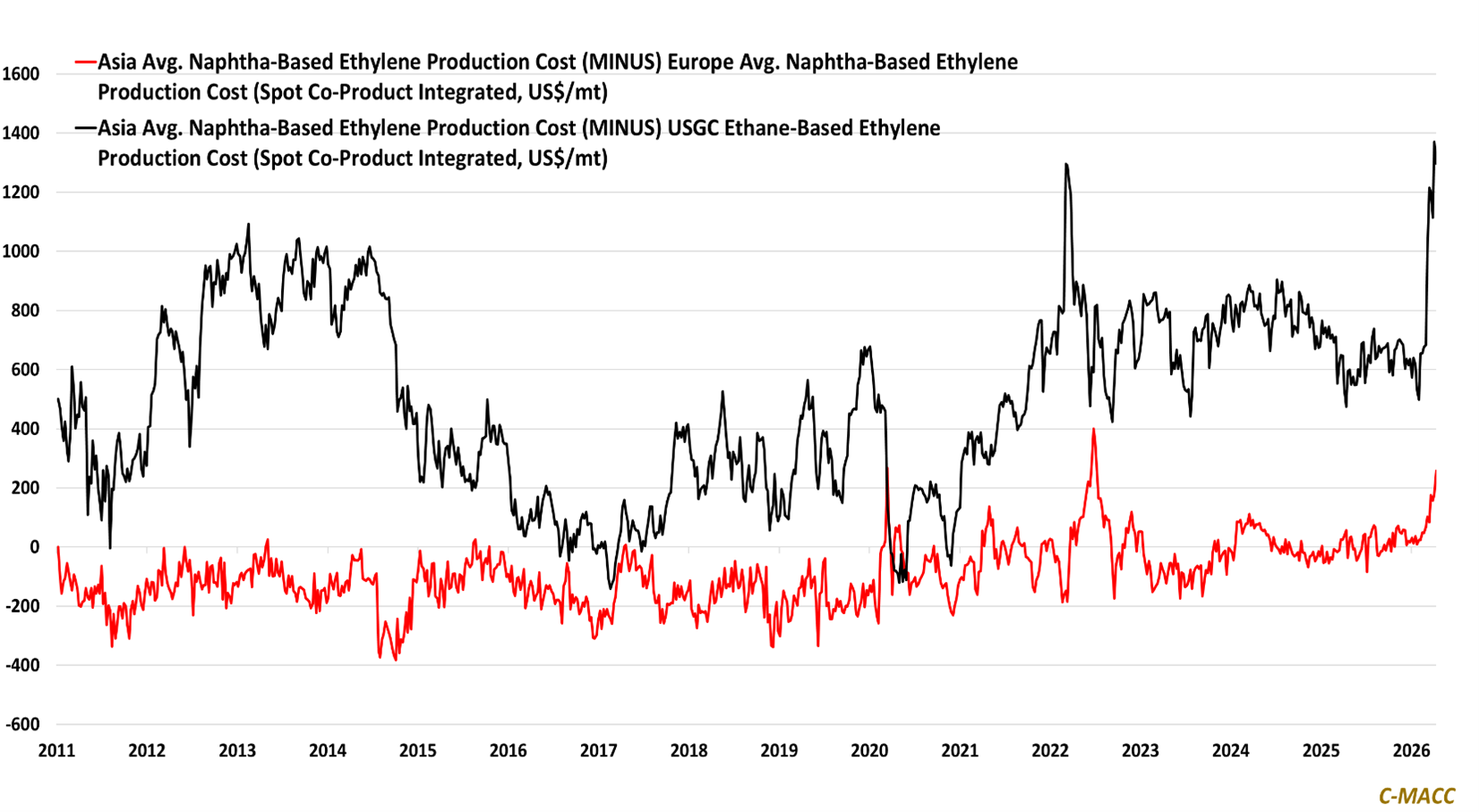

- Feedstocks & Energy: Global feedstock dislocations are persisting and deepening, with Asia’s rising naphtha premium versus Europe and US NGLs extending structural cost advantages toward North America through 2Q26.

- Olefins: Global olefins are repricing around operability, with Asia’s production run cuts and higher naphtha costs extending pricing power and margin advantage toward more reliable and relatively cost-advantaged producers.

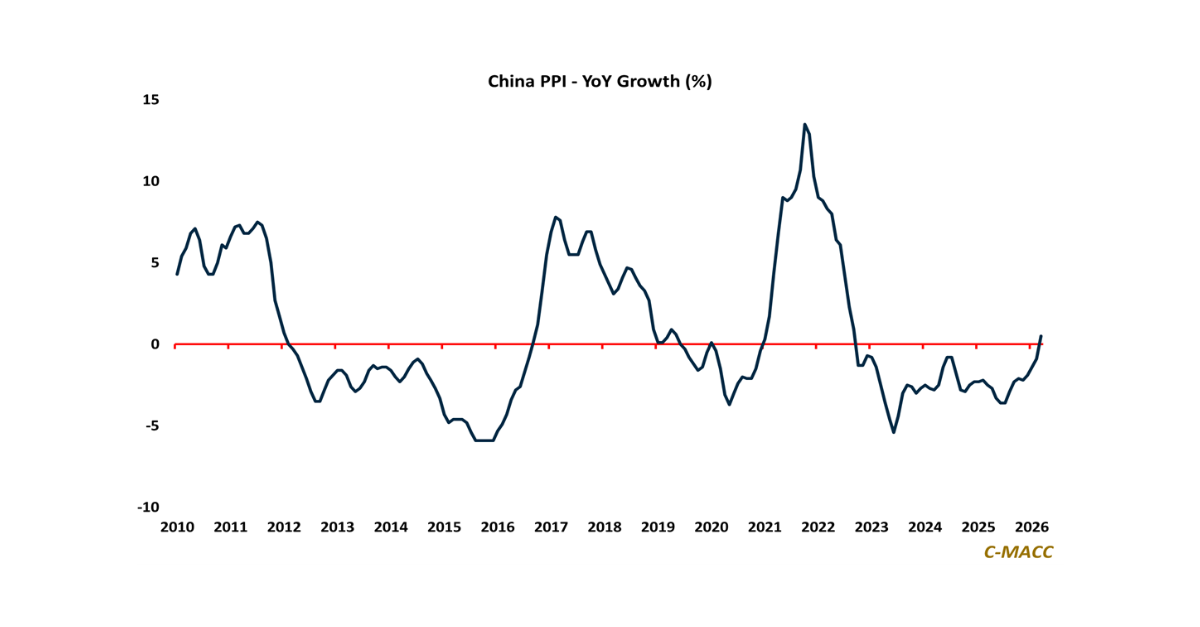

- Other Base Chemicals: Upstream inflation is outpacing downstream pass-through, reinforcing margin expansion for integrated producers and prompting demand rationing across the methanol, benzene, and chlor-alkali chains globally.

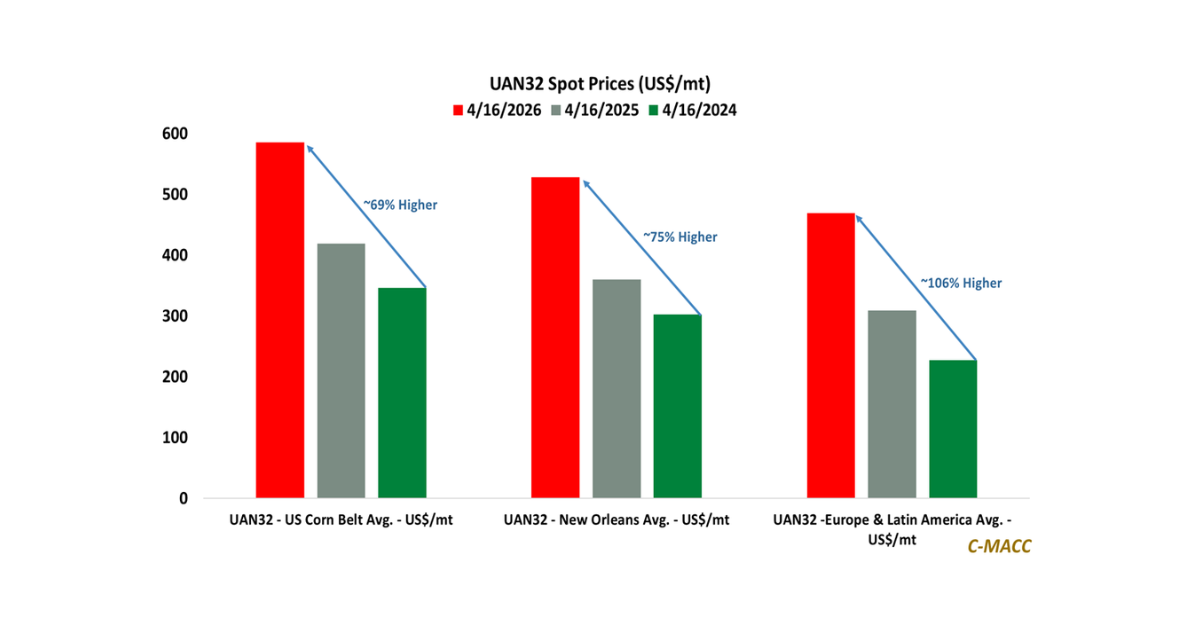

- Agriculture: Global nitrogen markets remain tighter than expected, sustaining strength in ammonia and urea and advantaging gas-rich producers, while pushing farmers to optimize application rates amid compressed margins.

- Refining & Biofuels: Global refining margins remain elevated as distillate strength has outpaced crude, with US ethanol markets benefiting from higher gasoline prices and strengthening policy support for blending expansion.

Exhibit 1 – Chart of the Day: Asian integrated ethylene production costs have surged relative to the US and Europe.

Source: C-MACC Estimates, April 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!