C-MACC Sunday Executive Summary

Gas, Gas, Maybe: Cheap Supply, Costly Access & The Premium on Delivery

- Natural gas markets are increasingly defined by infrastructure, access, and the ability to reliably convert production into delivered, monetizable demand across regional and global systems.

- Strong demand growth does not fully lift prices, as regional bottlenecks, timing mismatches, and infrastructure delays limit efficient balance across interconnected global gas markets.

- Value is shifting away from production and processing toward power delivery, logistics, and systems that control demand access, reliability, and timing across increasingly complex global regions.

- Capital will increasingly favor integrated systems that secure demand pathways, while standalone producers and processors face structural margin pressure despite favorable global feedstock economics.

- Additionally, co-product tightness, fertilizer affordability pressures, LPG dislocation, water constraints, and tightening capital collectively reinforce the importance of access, integration, and system control.

- Companies Mentioned: Enterprise Products, Energy Transfer, Phillips 66, Dow, LyondellBasell, ExxonMobil, Navigator Gas, Borealis, CF Industries, Woodside, Targa Resources, BP, Shell, TotalEnergies, DuPont, Westlake, JPMorgan, Bank of America

- Products Mentioned: Natural Gas, LNG, Ethane, Propane, LPG, Ammonia, Benzene, Butadiene, Propylene, Naphtha, Crude Oil, Gasoline, Sulfur, Phosphate, Fertilizers, Water

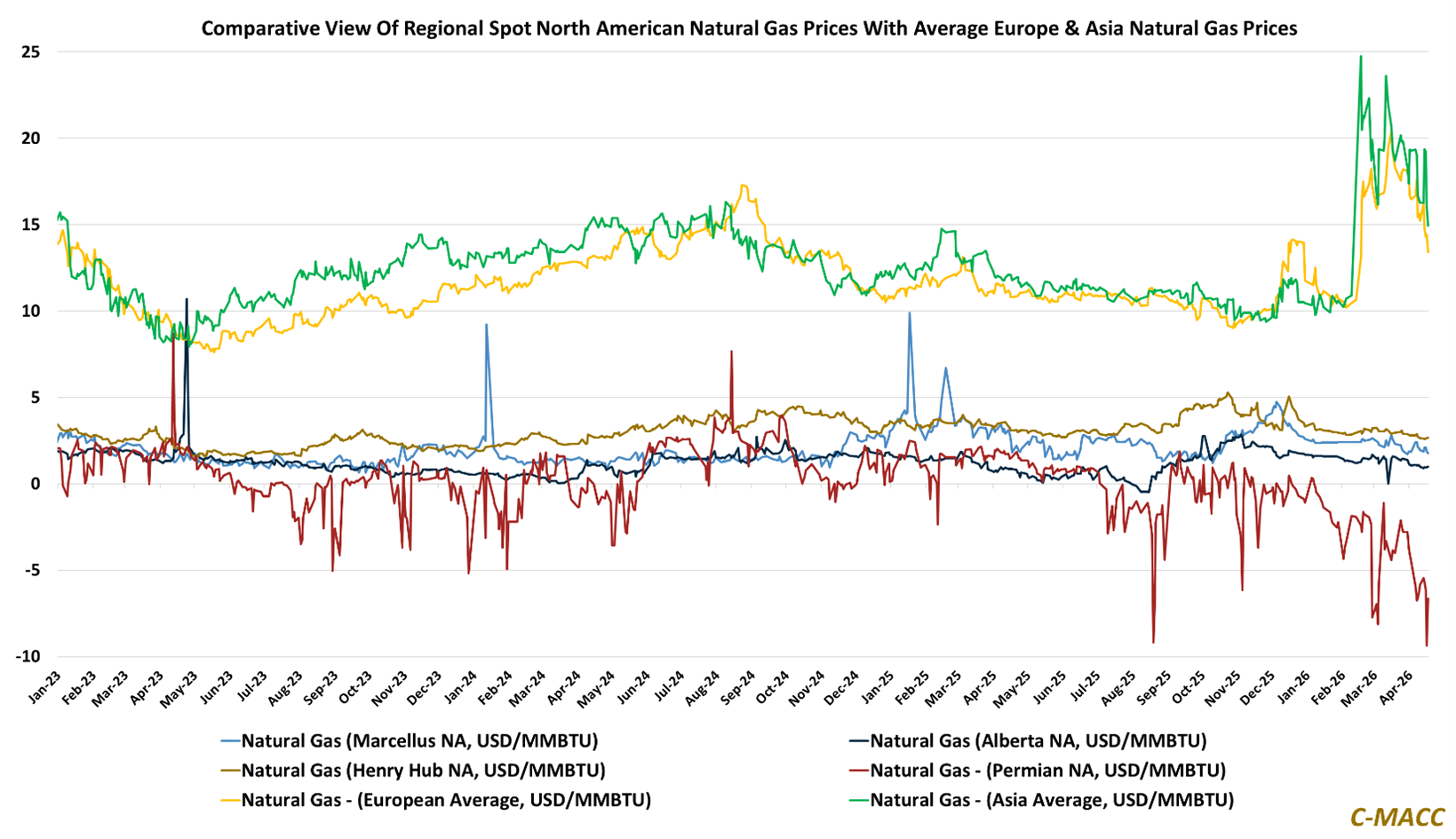

Exhibit 1: Global gas dislocation persists, with regional bottlenecks, distorting price signals and access.

Source: Bloomberg, C-MACC Analysis, April 2026

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!