Global Market Analysis

Delay of Game: Prices Lag Supply Until the Clock Runs Out and Reality Bites

Key Findings

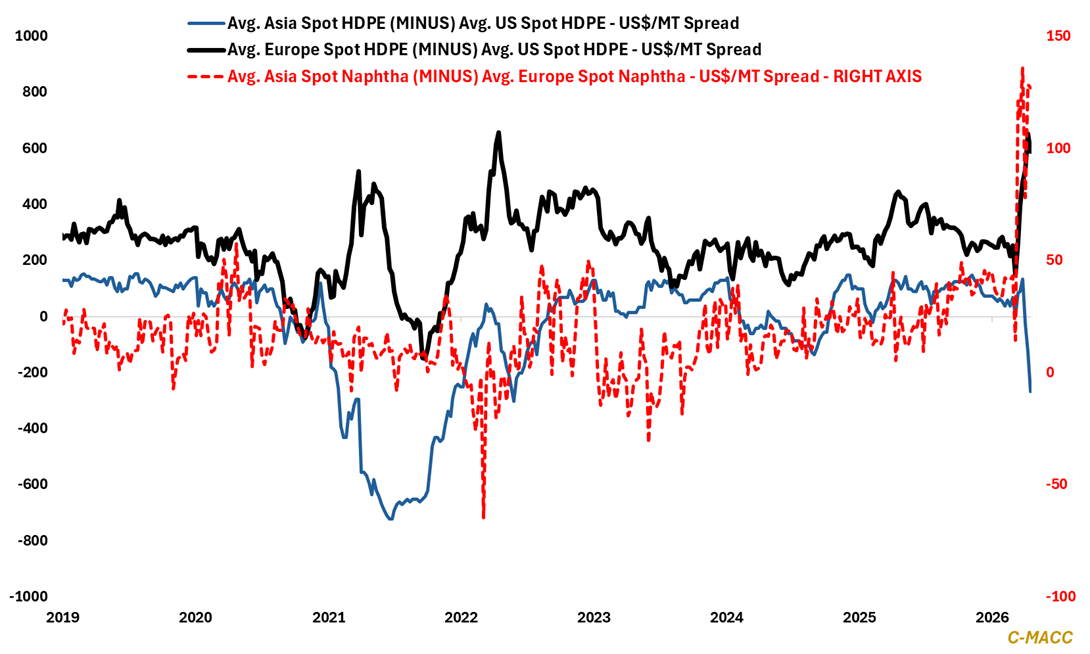

- General Thoughts: Asia polyethylene (PE) prices are too low relative to tightening supply, as feedstock shocks and run cuts have not cleared, setting up a delayed move higher toward European and US pricing.

- Supply Chain/Commodities: Refineries and governments direct feedstocks toward fuels and critical uses, reducing cracker co-product supply and forcing chemical markets to price scarcity despite uneven demand.

- Energy/Upstream: Control of pipelines, storage, and export terminals is setting pricing, as buyers lock in capacity early to avoid bottlenecks, shifting value from production to logistics access and delivery certainty.

- Sustainability/Energy Transition: Hyperscalers, utilities, and industrial buyers secure turbines, transformers, and grid access early, paying for delivery certainty as capacity limits, not demand, determine value.

- Downstream/Other Chemicals: Companies are balancing price increases against demand risk, limiting inventory commitments to avoid both pushing customers too far and locking in costs that may not last.

Exhibit 1: Feedstock stress, production adjustments, and inventory gaps drive divergent PE and naphtha spreads.

Source: C-MACC Estimates, April 2026

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!