Global Market Analysis

No Gas No Glory: Access Is Driving Industrial Strategy

Key Findings

- General Thoughts: Low-cost US natural gas is becoming more contested as power producers, exporters, petrochemical buyers, and industrial consumers secure access and defend feedstock-cost advantages.

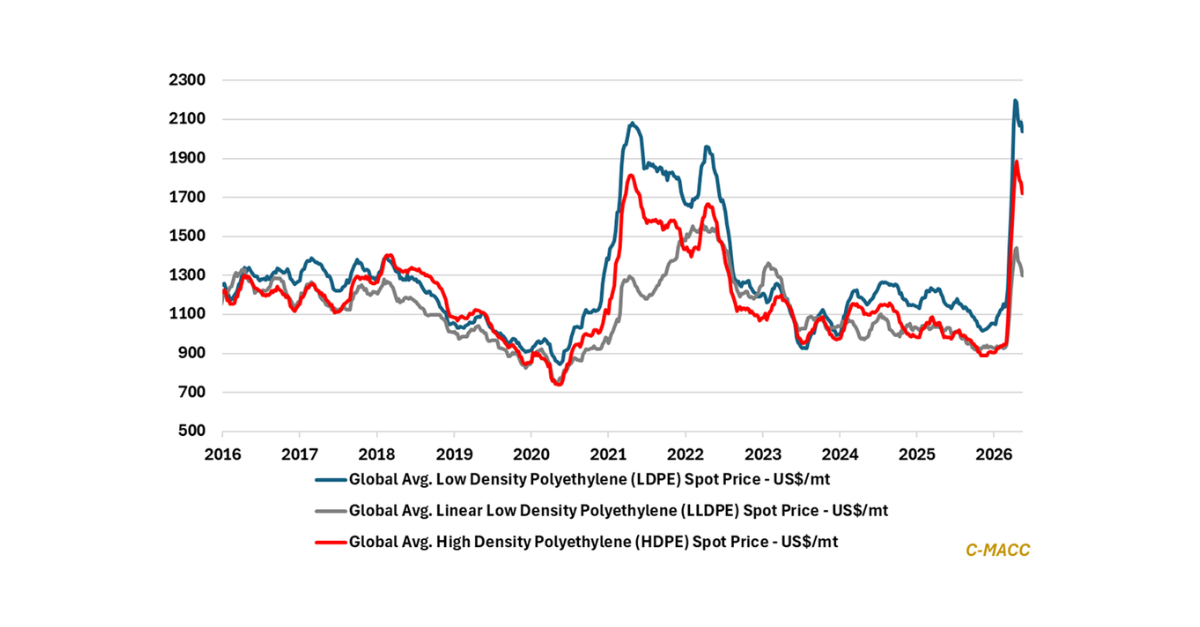

- Supply Chain/Commodities: Return pressure in Europe and Asia is forcing chemical producers to test ownership clarity, fixed-cost resilience, and cash conversion as lower-cost supply regions capitalize.

- Energy/Upstream: Higher-cost overseas NGL and olefin markets are strengthening North American export leverage, while domestic chemical buyers face a more contested feedstock advantage.

- Sustainability/Energy Transition: Europe’s carbon and gas burden strengthens lower-cost supply regions across industrial chains as BASF restructuring shows Europe’s cost stack forcing harder capital choices.

- Downstream/Other Chemicals: US soybean premiums are revealing how renewable fuels, Brazil’s cost squeeze, and China’s slower buying are repricing the agricultural, energy, and chemical chains.

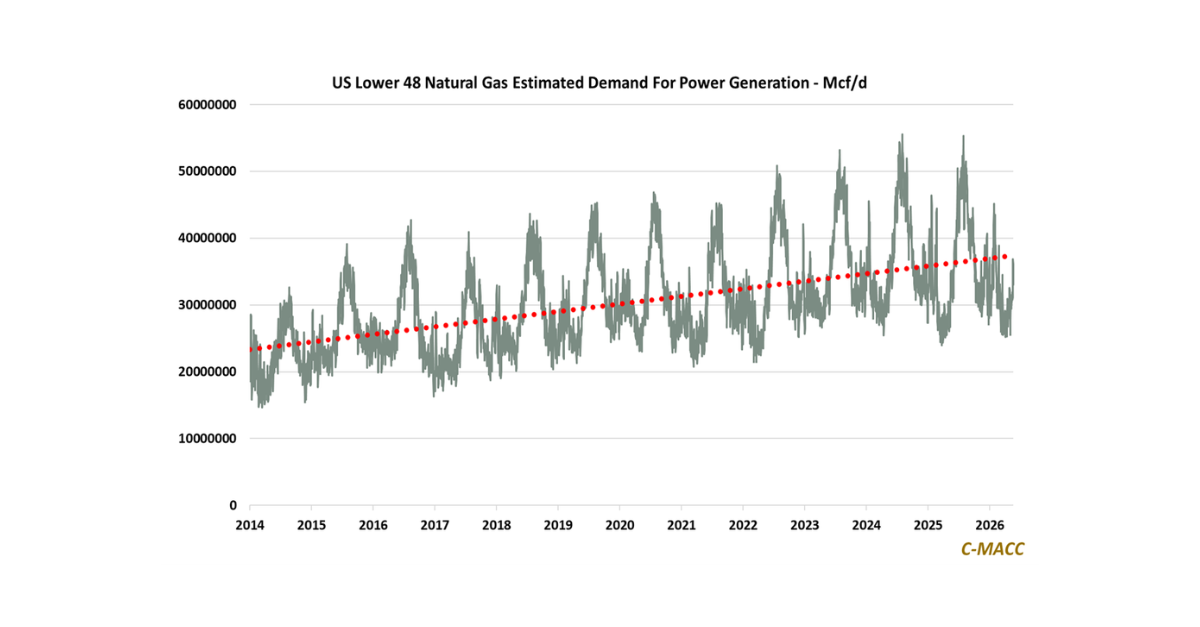

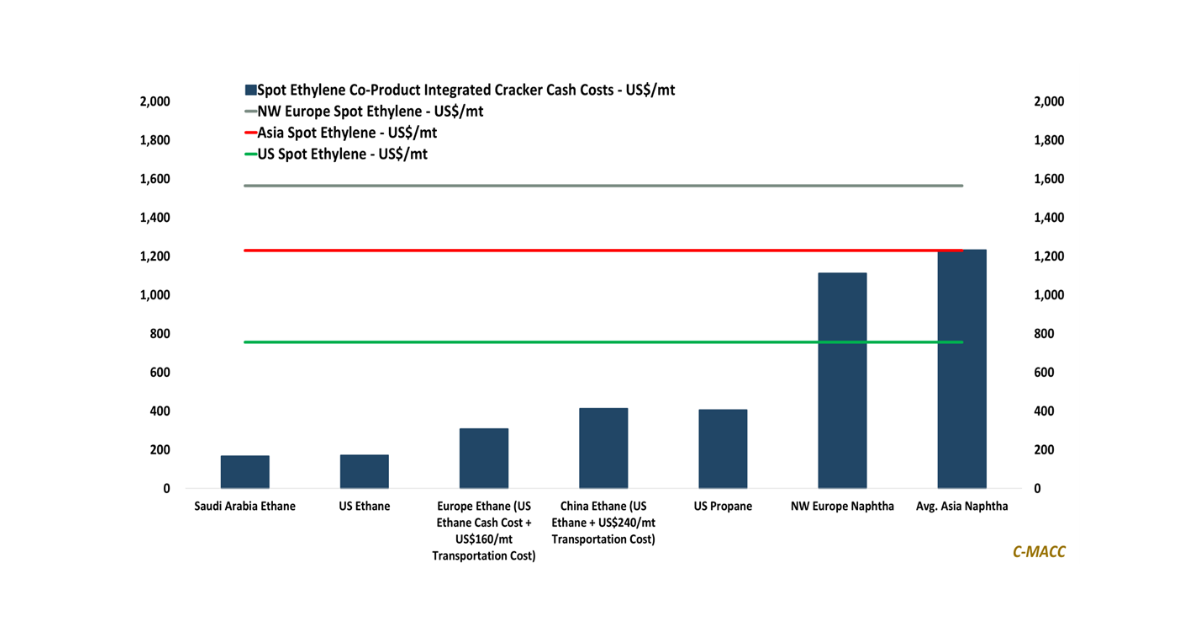

Exhibit 1: Rising cross-market demand turns low-cost US gas access into a strategic battleground.

Source: Bloomberg, C-MACC Analysis, May 2026

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!