C-MACC Sunday Executive Summary

Rethink Tank: Asia’s Olefins Pain Separates Who Can Remain

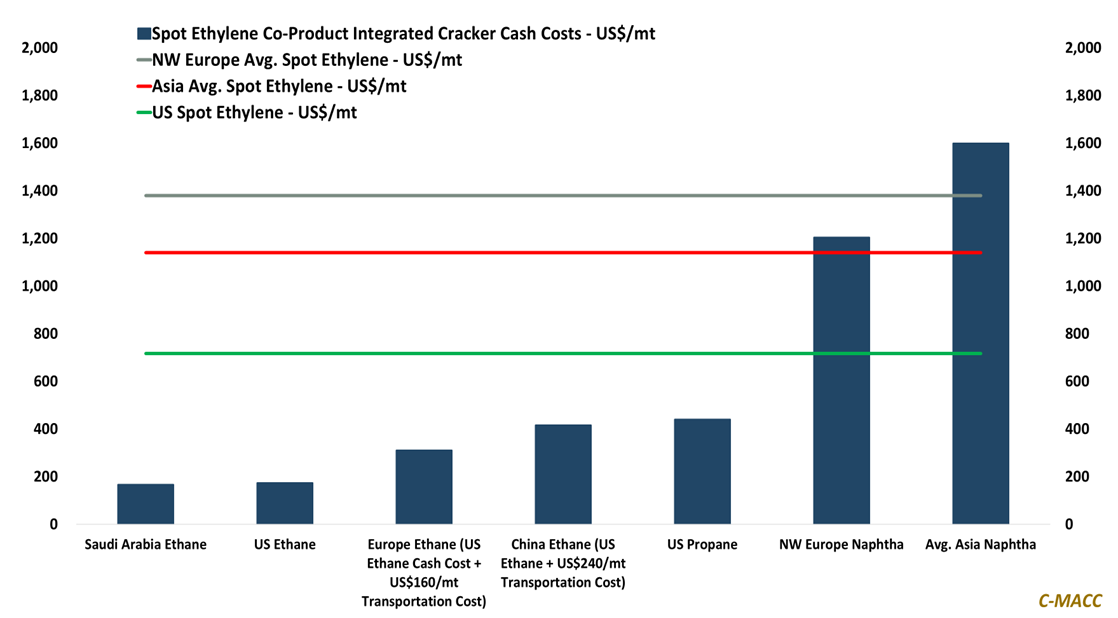

- Asia’s olefins cost-recovery squeeze is forcing ex-China asset reviews, as naphtha-based production costs exceed those in Europe and Chinese exports limit derivative price recovery.

- Europe’s elevated co-product prices relative to Asia and reduced imports support cracker margins, while Asian producers face weaker offsets, cash-preservation pressure, and tougher buyer negotiations.

- US reliability and Middle East route recovery add cargo options, but China-linked pricing, logistics friction, and netback competition should keep Asia’s recovery structurally uneven.

- Japan’s cracker consolidation, petrochemical spin-off reviews, and Korea’s restructuring show ex-China Asia shifting from margin defense toward portfolio-level capital rationing.

- Additionally, aluminum, gas, circular plastics, and freight show pricing power shifting from commodity exposure toward controlled delivery, qualified demand, and power access.

- Companies Mentioned: Mitsubishi Chemical Group, Asahi Kasei, Mitsui Chemicals, Lotte Chemical, HD Hyundai Chemical, Alcoa, Hydro, Qatalum, APAR, Entergy, Meta, Energy Transfer, Williams, PureCycle, Plastic Ingenuity, Reliable Caps, Procter & Gamble, Amcor, Berry, Dow, LyondellBasell, Borouge, OMV, TotalEnergies

- Products Mentioned: Naphtha, Ethylene, Propylene, Polypropylene, Polyethylene, Hydrogen, Aluminum, Copper, Natural Gas, Crude Oil, Coal, LNG

Exhibit 1: Asia’s Naphtha Cost Premium Is Outrunning Derivative Pricing Across Key Product Chains.

Source: Bloomberg, C-MACC Analysis, May 2026

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!