Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

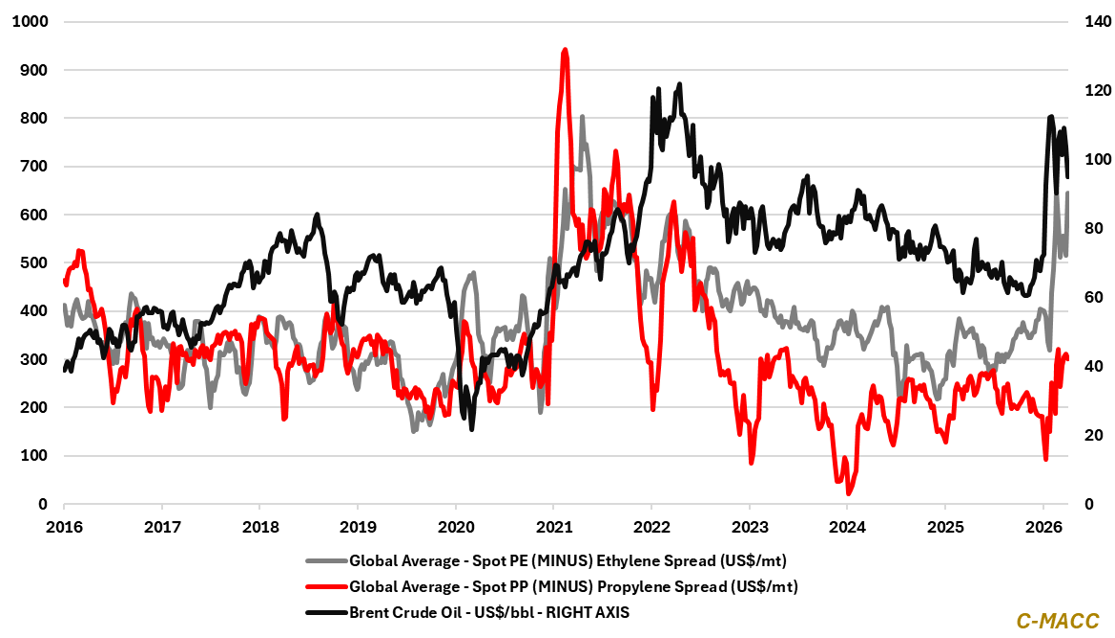

- General Thoughts: Global polymer-to-monomer spreads remain above levels supported by feedstock costs and trade flows, leaving prices exposed as freight stabilizes, buyers preserve cash, and contract benchmarks face pressure.

- Polyethylene (PE): Global PE prices have outrun ethylene cost support, making regional contract premiums harder to defend as China’s PE trade balance shifts, US export values weaken, and buyers delay restocking.

- Polypropylene (PP): Global PP margins are holding for the wrong reason, as falling PGP supports spreads despite weak demand, leaving producers exposed to sharper compression once feedstock declines stop doing the work.

- Polyvinyl Chloride (PVC): The global PVC market reflects staggered trade flows rather than demand strength, with Asia mostly adjusted from 1Q26, the US holding a floor, and Europe facing the next reset as imports meet legacy pricing.

- Other Sector Developments: Asian and European naphtha has eased from wartime peaks, but oil draws and Hormuz friction keep feedstock risks for olefins elevated. At the same time, the US hurricane season adds background risk.

Exhibit 1 – Chart of the Day: Polymer-To-Monomer Spreads Signal Pricing Risk as Supply and Trade Flows Normalize

Source: Bloomberg, C-MACC Estimates, June 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!