Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

- General Thoughts: Falling global polymer prices test which producers can defend returns, as excess supply, PE grade splits, PP route differences, PVC policy friction, and feedstock relief reshape markets into late 2H26.

- Polyethylene (PE): Global spot PE prices weakened last week as lower naphtha, May US inventory growth, and Southeast Asian discounting reinforced broader pressure on regional contracts amid rising expectations for lower 2H26 prices.

- Polypropylene (PP): Global PP margins are splitting by producer type as lower propylene prices temporarily help non-integrated producers, while integrated feedstock control looks more durable as China-linked cargo pressure builds.

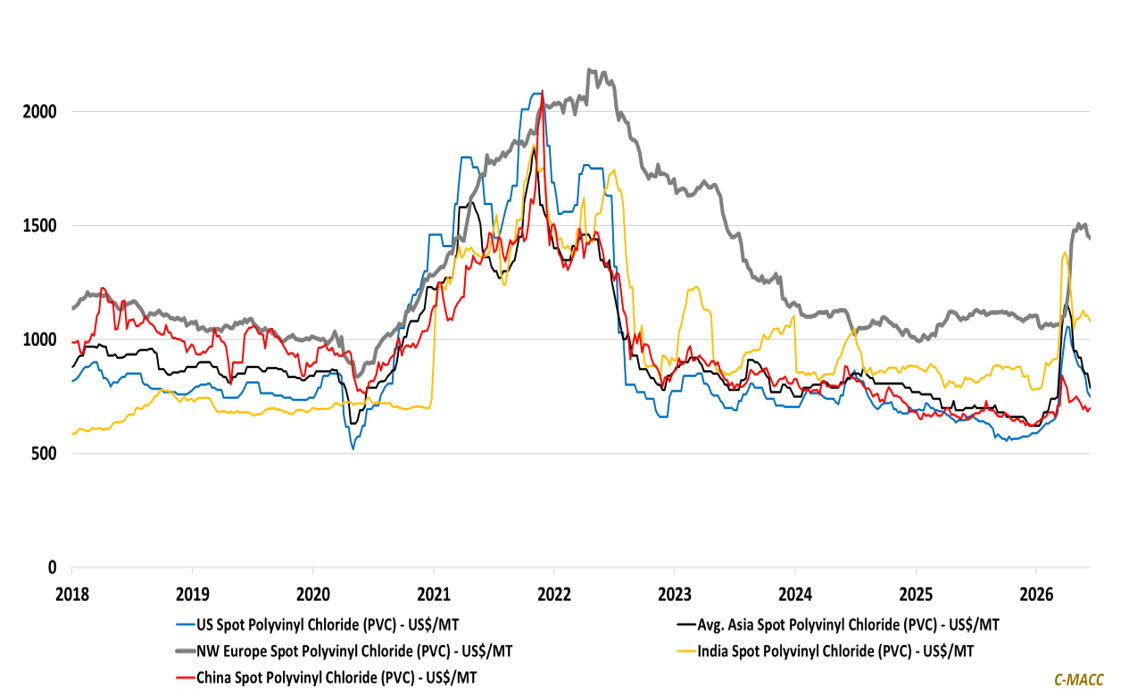

- Polyvinyl Chloride (PVC): Global PVC buyers lack urgency, as weak housing, lower EDC-linked costs, and China’s carbide-based supply pull export bids down, putting downward pressure on regional contracts and prices into 2H26.

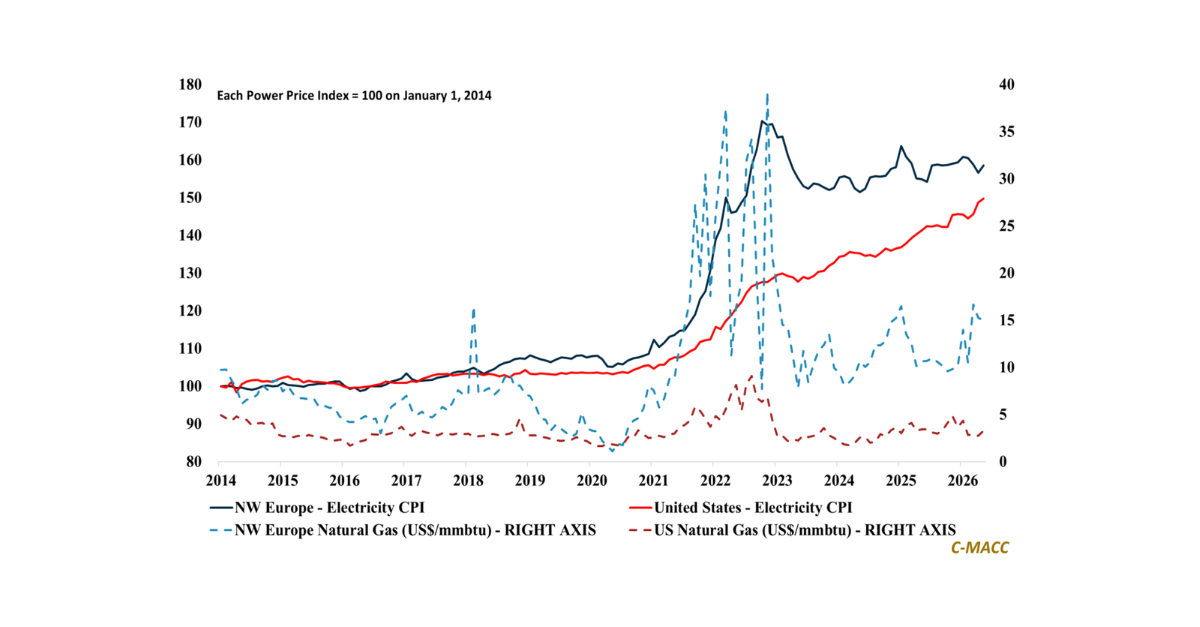

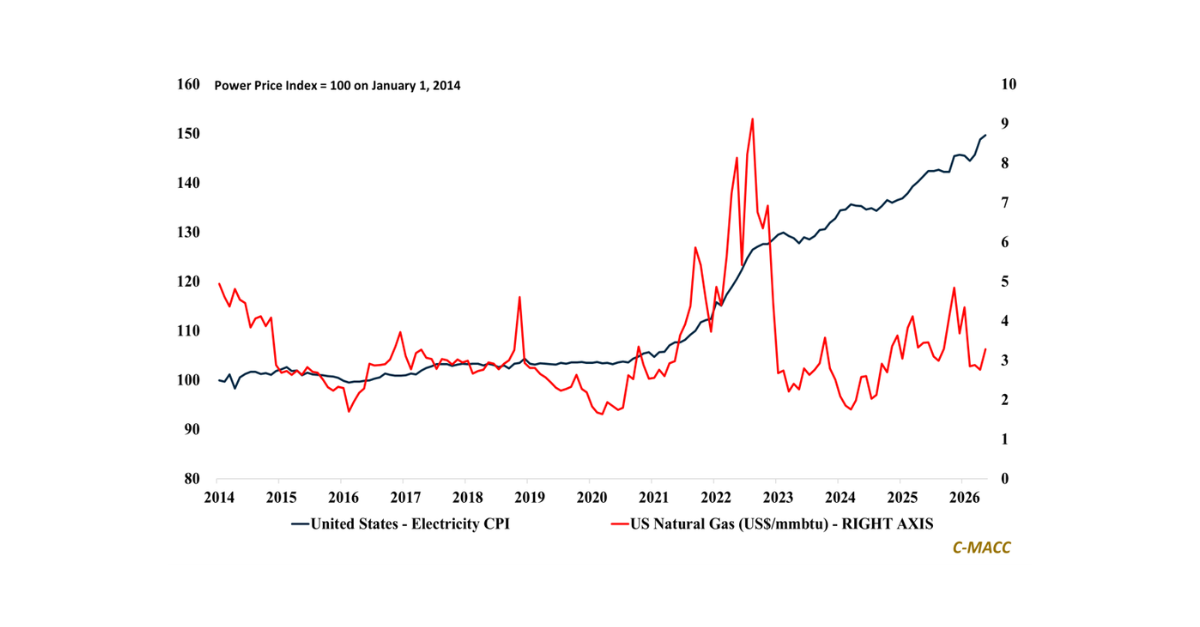

- Other Sector Developments: Naphtha and seaborne LPG prices have fallen from their 1H26 highs versus ethane, but buyers should stage coverage rather than call a bottom before plant restarts absorb cargoes and tighten margins.

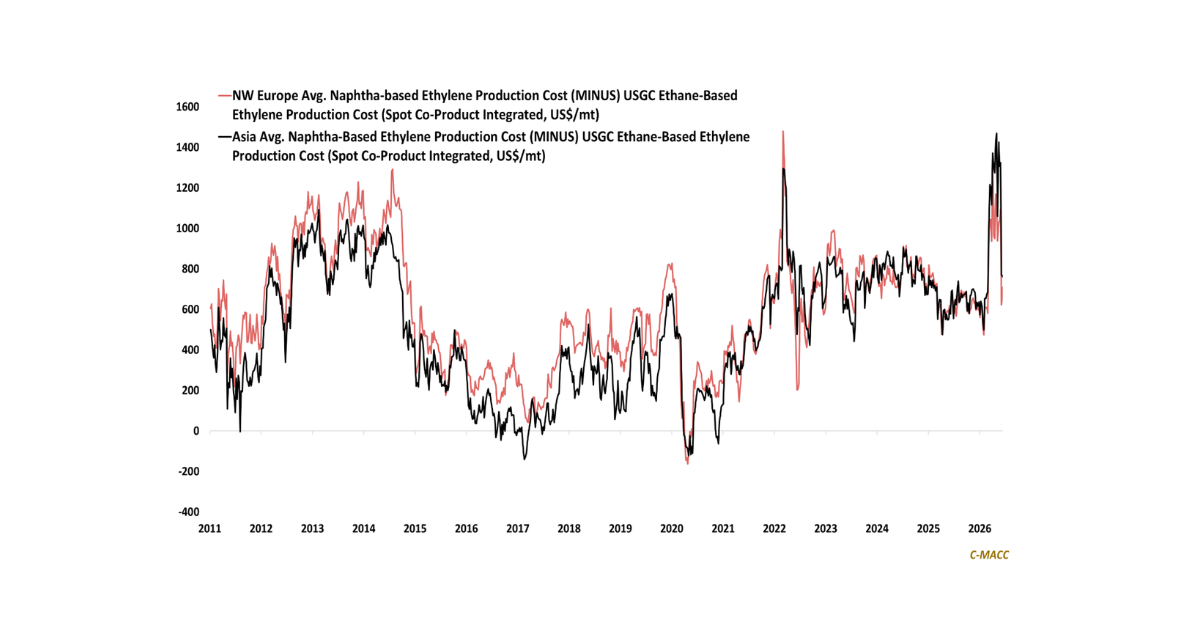

Exhibit 1 – Chart of the Day: PVC Price Gaps Show Where Global Supply Pressure Will Test Regional Returns.

Source: C-MACC Estimates, June 2026

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!