C-MACC Sunday Executive Summary

Margin Call: Defense Is Back, But Discounts Look Too Broad

- Chemical equities are turning defensive again, but the split is sharper as commodity and specialty sentiment weakens while fertilizers and industrial gases retain support.

- Consensus is right that commodity chemicals face oversupply, but may underprice margin support if crude rebounds, USGC hurricane season outages tighten supply, or high-cost regions restructure materially.

- Specialty chemicals should not get a free pass, but H.B. Fuller and Evonik show value-added products can hold price through qualification and service after raw-material relief reaches customers.

- Yara’s USGC ammonia acquisition and Air Products’ LCEC exit show capital favoring existing demand-backed capacity over speculative projects still needing contracted customers.

- Additionally, supply assurance, power access, contract timing, and bankable demand shape who retains value as Chinese exports pressure global prices and transition capital favors visible cash flow.

- Companies Mentioned: Dow, LyondellBasell, H.B. Fuller, Evonik, Yara, Air Products, Air Liquide, Linde, Methanex, Sipchem, Alcoa, South32, Shell, Cheniere, ExxonMobil, Samsung, Northvolt, Sinopec, BYD

- Products Mentioned: Crude Oil, Polyester, Ammonia, Polyethylene, Ethane, Methanol, Natural Gas, Aluminum, Copper, Caustic Soda, Chlor-Alkali, Naphtha, Propylene, Ethylene, Aromatics, Coal, Diesel, Jet Fuel, LPG, Hydrogen, Polypropylene, Polyvinyl Chloride, Gasoline

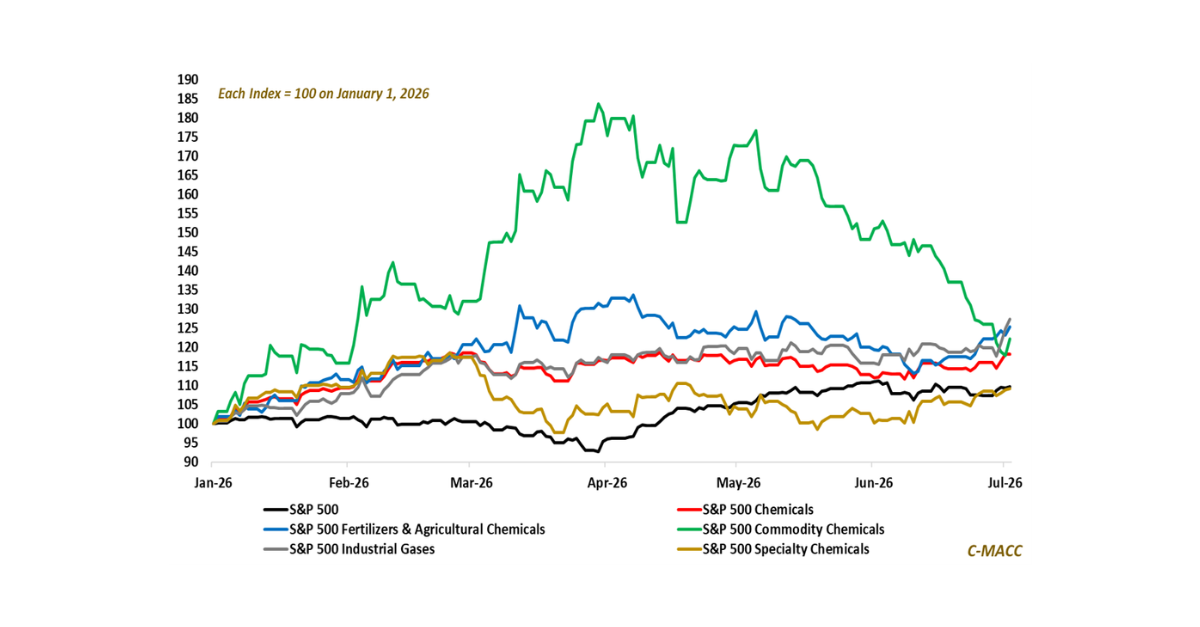

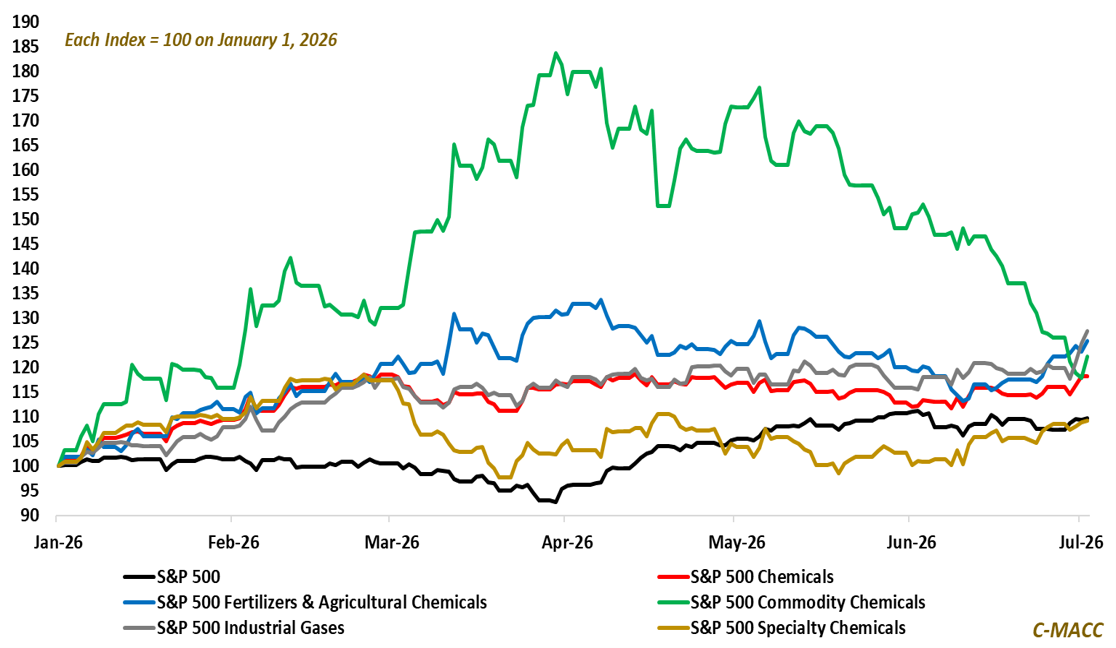

Exhibit 1: US Commodity Chemicals Lost Early Leadership as Fertilizers and Industrial Gases Held Ground.

Source: Bloomberg, C-MACC Analysis, July 2026

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!