Global Market Analysis

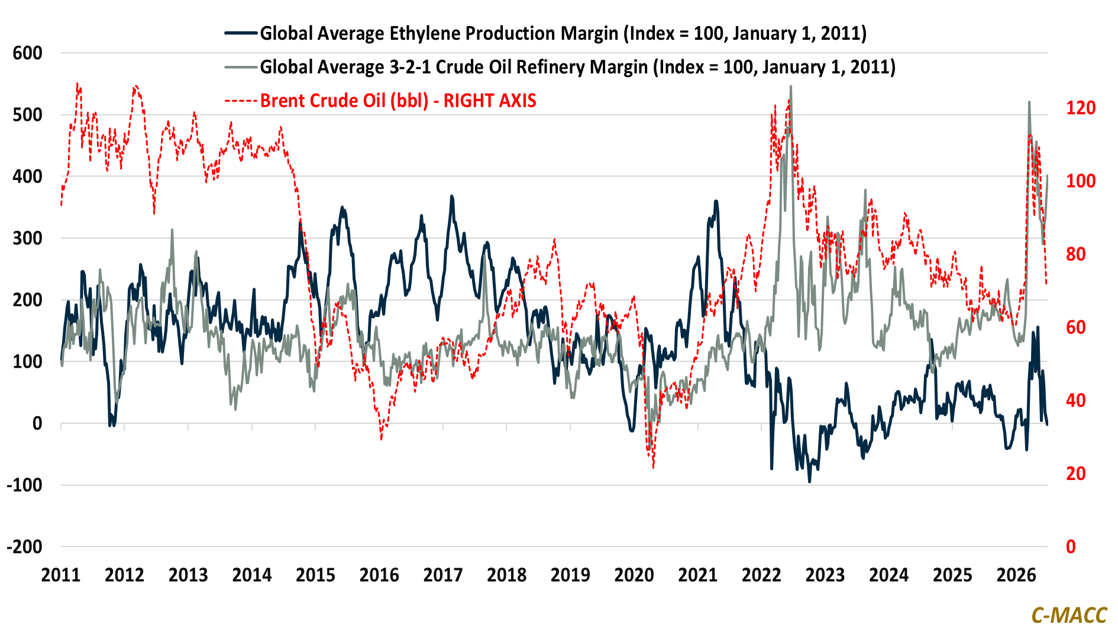

Oil’s Split Decision: Refiners Rally While Chemicals Fight a Flatter Curve

Key Findings

- General Thoughts: Global chemical markets return to oversupply as cost curves flatten, while constrained refining supports firmer margins and steers capital toward fuels, integration, and advantaged export systems.

- Supply Chain/Commodities: Shell’s chemical and refinery margin indicators rose in 2Q26, but 3Q26 trends point to divergence as war-premium spreads fade and global refined-product tightness persists.

- Energy/Upstream: Lower crude oil prices have narrowed feedstock spreads, but Japan’s naphtha-stockpile push shows buyers will pay for supply security after Hormuz risk reprices inventories and optionality.

- Sustainability/Energy Transition: H2BE reframes EU hydrogen from climate ambition to cluster defense, where subsidy design, CCS scale, and deliverability determine the investability of chemical assets.

- Downstream/Other Chemicals: US chemical rail’s rebound signals that buyers are shifting from inventory protection to replenishment, as stabilized global cost curves spur competitive, reliable export flows.

Exhibit 1: Lower Crude Pressures Chemical Margins as Refining Constraints Keep Fuel Markets Firm.

Source: Bloomberg, C-MACC Analysis, July 2026

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!