C-MACC Sunday Executive Summary

Profit Pending: Better Margins Still Need Real Business

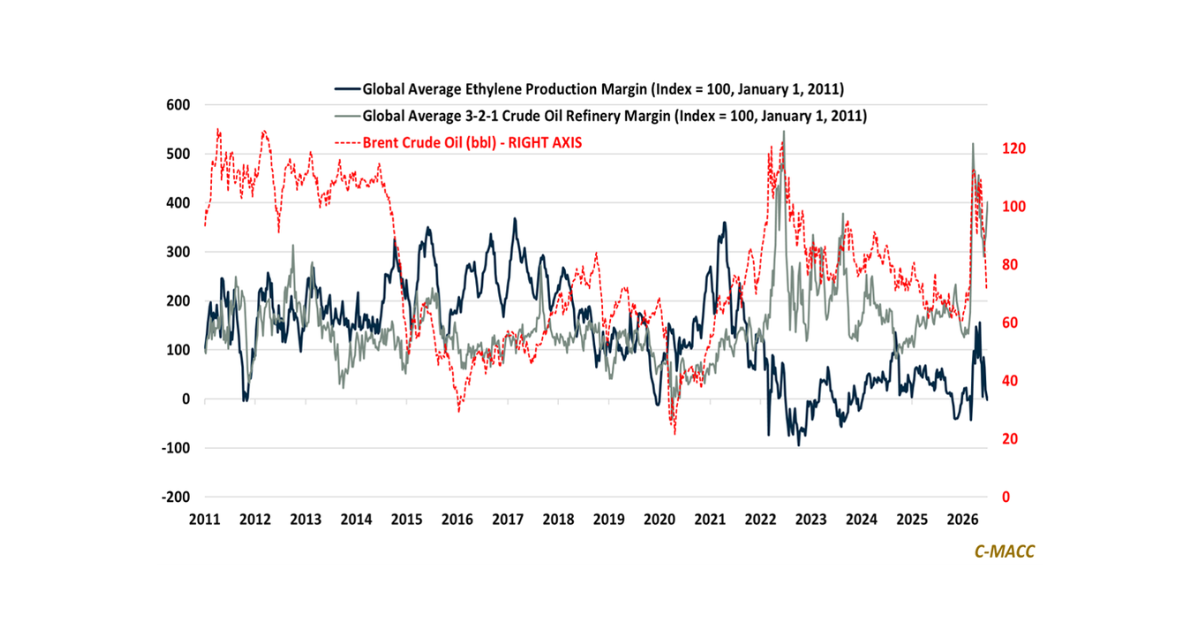

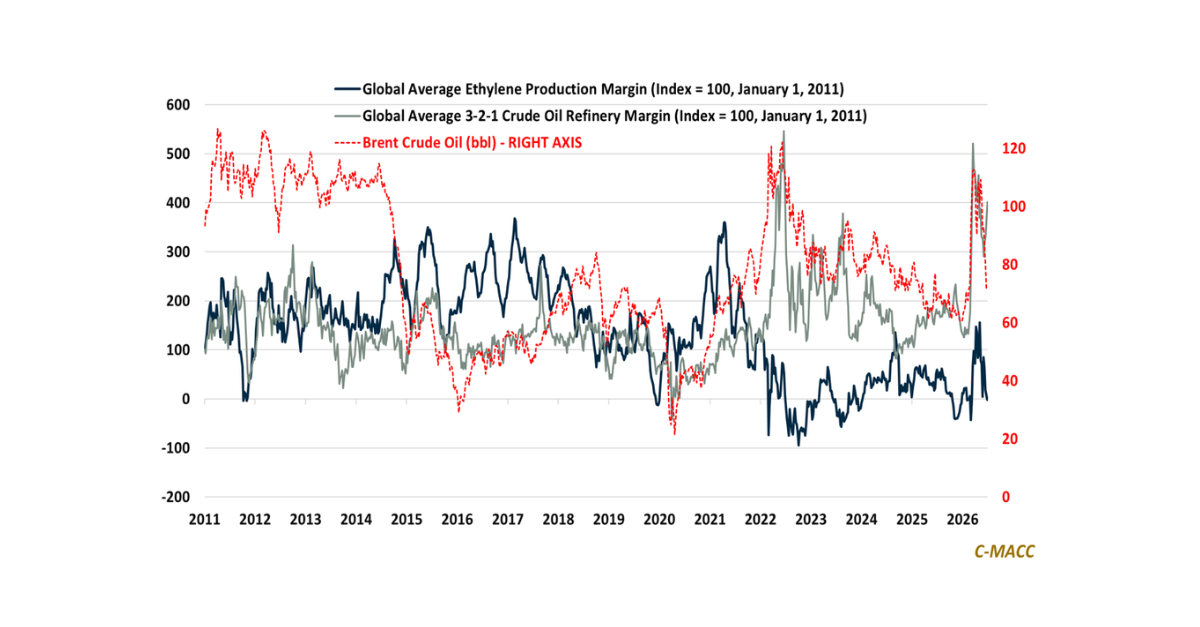

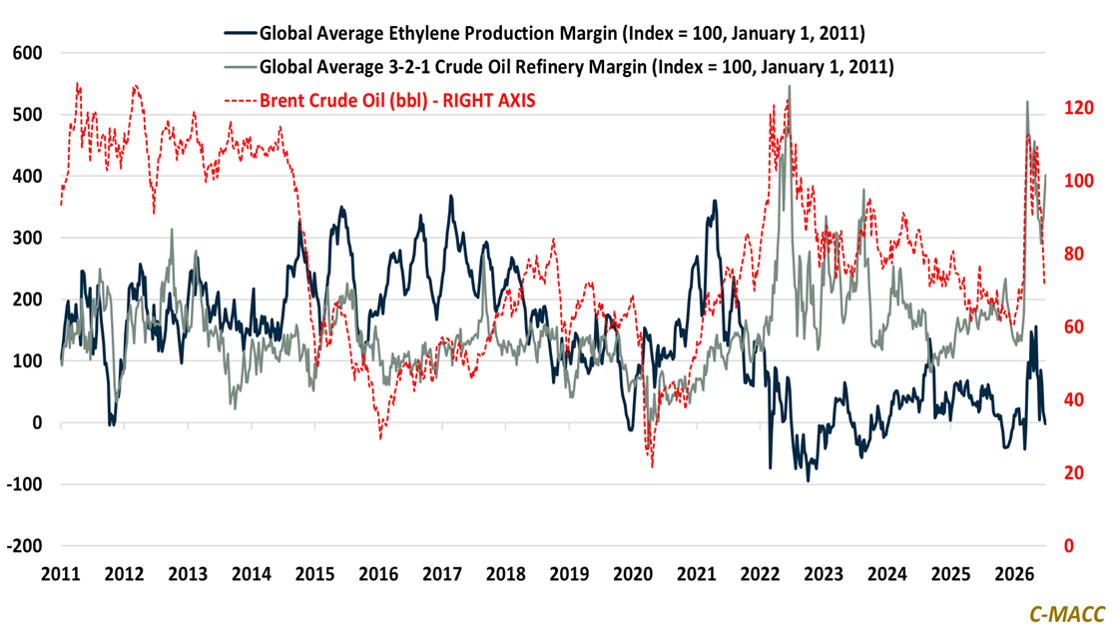

- Global refining margins still outperform ethylene because tight fuel supply supports plant rates, although renewed Middle East tension has interrupted the latest decline in chemical production economics.

- Shell and OMV updates show why stronger calculated spreads can overstate earnings improvement when lower plant rates, weaker sales volumes, and wider discounts reduce the gain producers retain.

- Solstice is buying established positions in semiconductor manufacturing with Element Solutions, but the transaction creates value only if those capabilities lift underlying sales and cash faster than financing costs.

- During 2Q26 reporting season, the decisive test is whether higher margins accompany stronger physical volumes and recurring cash generation or leave 2H26 forecasts dependent on temporary price support.

- Additionally, market support should favor producers that place advantaged supply before competing capacity returns, linking export access and buyer timing across chemicals, minerals, and agriculture.

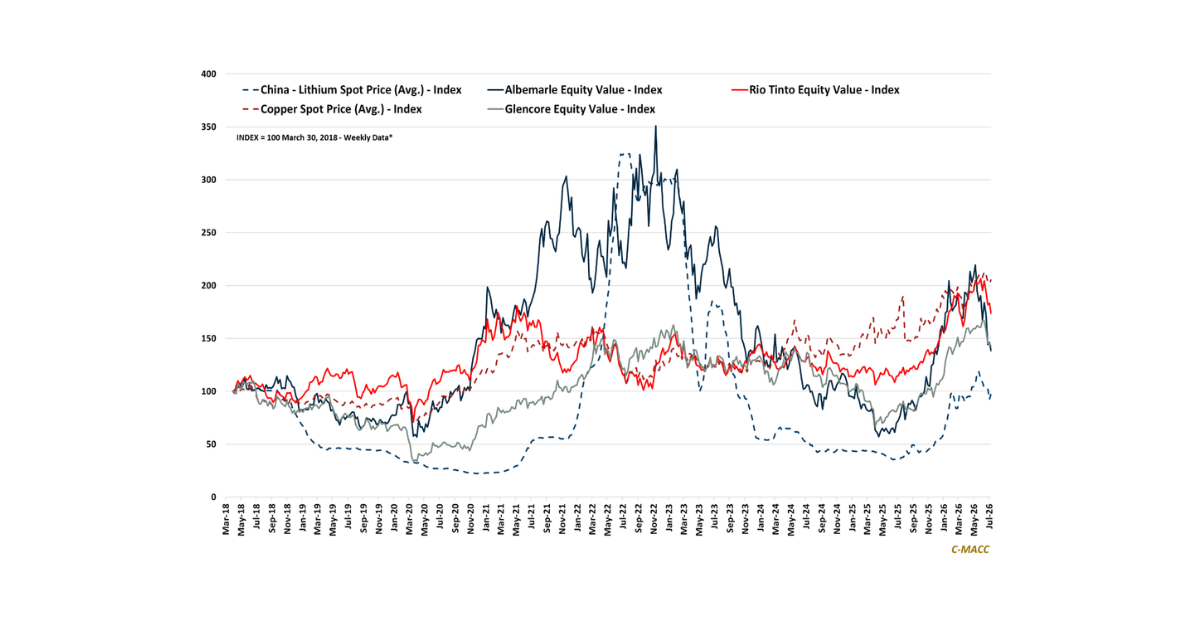

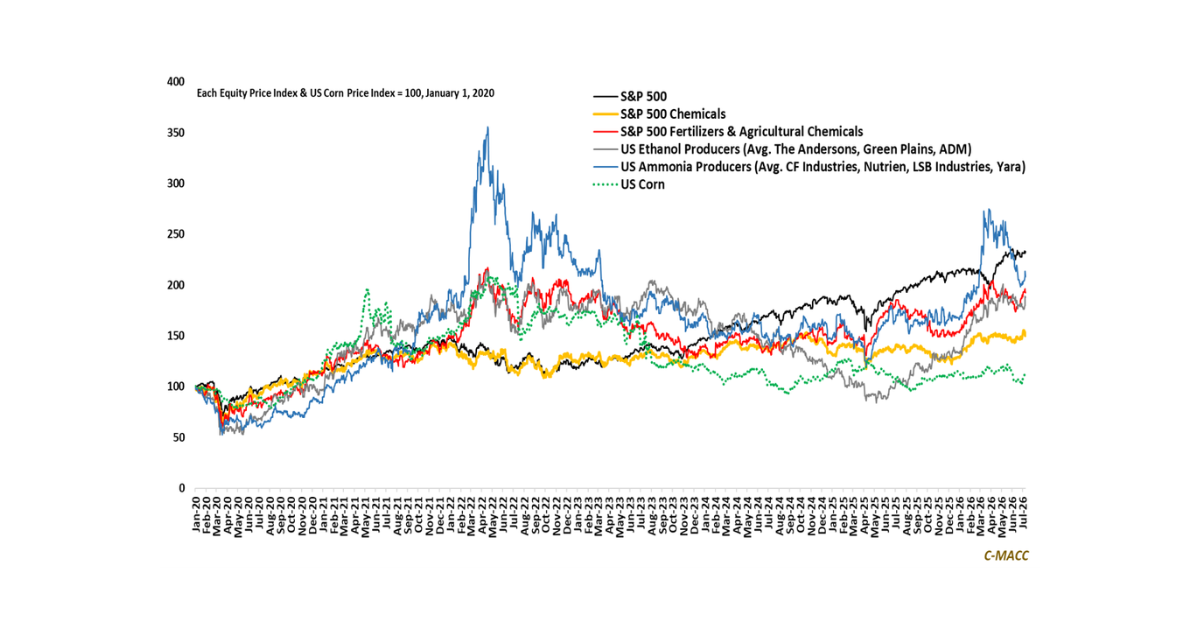

- Companies Mentioned: Shell, OMV, Borouge International, Solstice, Element Solutions, Yara, Gulf Coast Ammonia, Venture Global, Cheniere, Gulf Coast Express, Energia, Albemarle, Rio Tinto, Glencore, CATL, Sigma Lithium, Dow

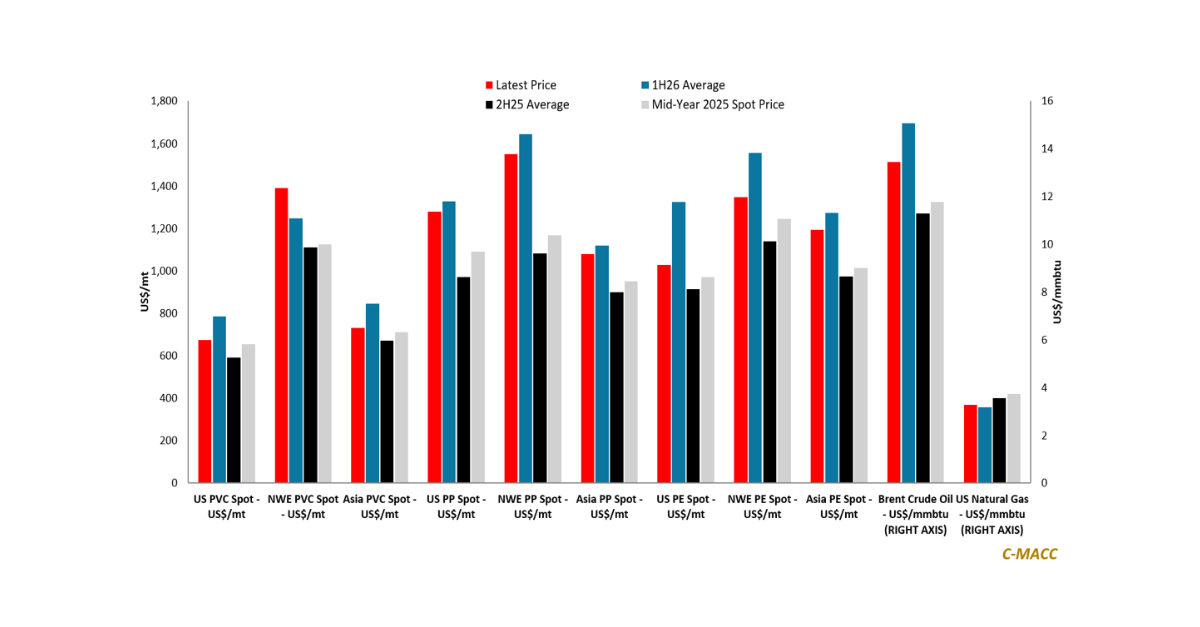

- Products Mentioned: Ethylene, Crude Oil, Naphtha, Ethane, Gasoline, Diesel, Jet Fuel, Propylene, Copper, Ammonia, Corn, Natural Gas, Polyethylene (PE), Polypropylene (PP), Polyvinyl Chloride (PVC), Nitrogen, Methanol, Chlor-Alkali, Lithium, Aluminum, Iron Ore, Nickel, Cobalt, Soybeans, Ethanol

Exhibit 1: Middle East Tension Stalls Ethylene Margin Erosion as Refining Retains Stronger Support.

Source: Bloomberg, C-MACC Analysis, July 2026

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!