The Hydrogen Economy # 37

Blue is Bankable – Competitive and Likely Fundable Through LNG-Type Contracts

Key Points

- The US LNG export industry developed through fixed-margin offtake agreements that supported funding. We believe that the US blue hydrogen/ammonia industry should evolve in a similar manner.

- With the benefit of 45Q, blue ammonia should have a lower cash cost than grey ammonia for the better projects – suggesting that new capacity should be financeable. The risk is that cash cost-based pricing gets in the way.

- Grey hydrogen/ammonia facilities in the US are mostly depreciated, and in weaker markets, pricing does not reflect full costs – including capital. Full-cost blue hydrogen/ammonia cannot compete with cash-cost grey.

- For the first time since we started this report, we have no projects to discuss in detail. This is not surprising given the slowdown in hydrogen momentum – there have been some updates of projects already covered.

- We look at some of the challenges that power may face with the availability of equipment and materials, focusing on copper. We also look at expected power prices in Germany.

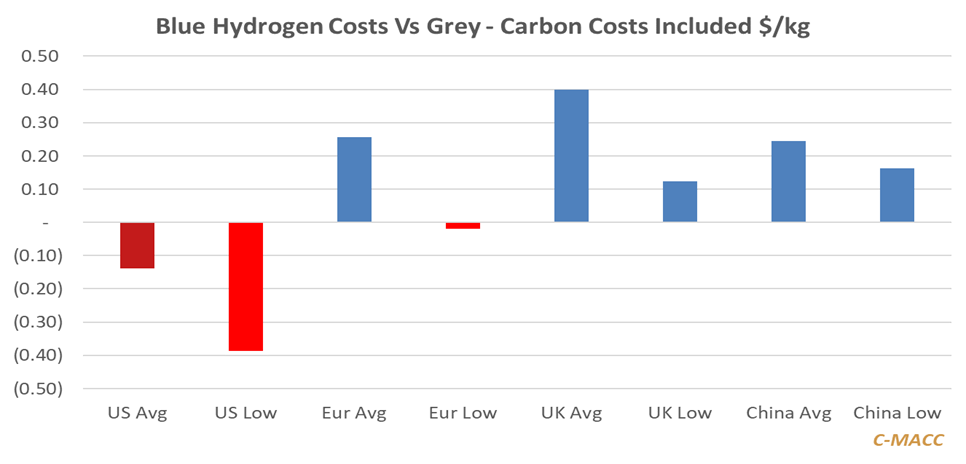

Exhibit 1: We see production economics supporting blue hydrogen investment, but only strong demand pull will support fixed economics offtake deals.

Source: Capital IQ and C-MACC Analysis

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!