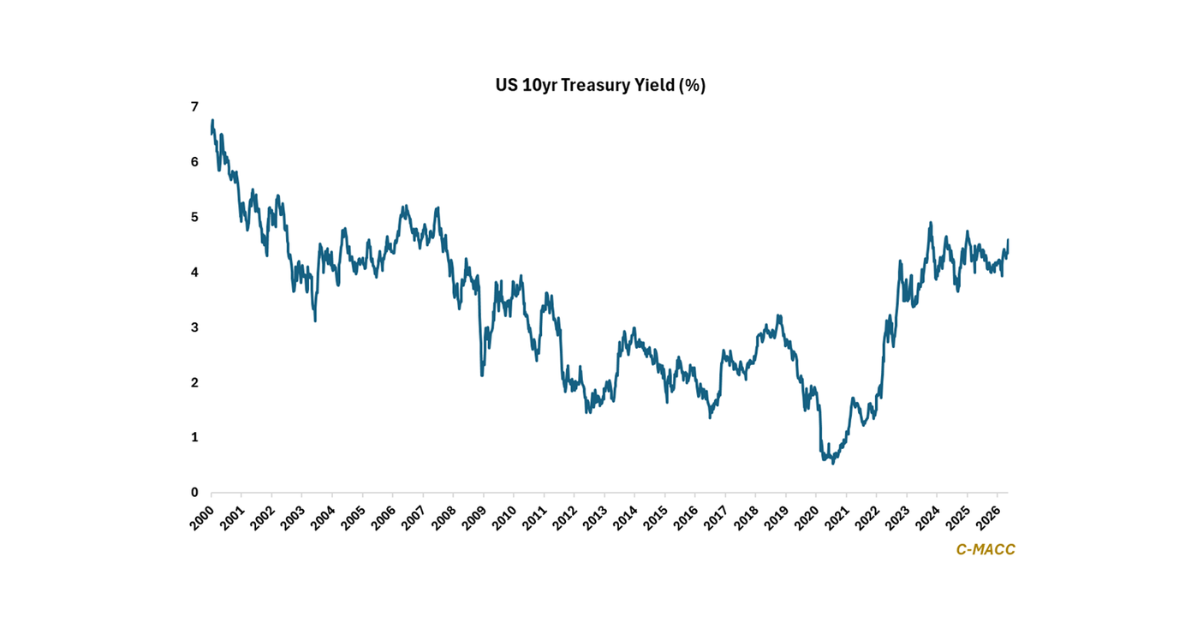

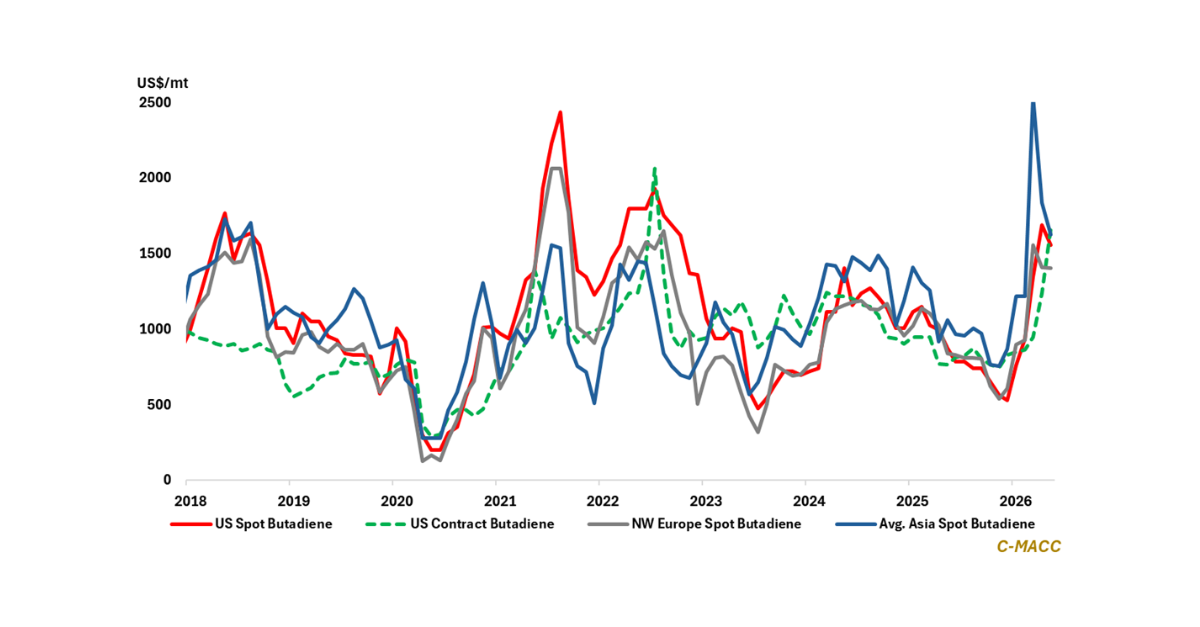

Daily Chemical Reaction

Costs & Integration Matter – North America Feedstock Cost Advantage, China’s Role In Chemical Oversupply Evident In 1Q24

Key Findings

- General Thoughts: Global chemical markets will likely remain oversupplied in 2024 as North America pushes its cost position and China boosts production at the expense of most producers in Asia Ex-China and Europe.

- Supply Chain/Commodities: We discuss the differences between the Dow and BASF 1Q24 results and outlooks, Alpek results in Plastics & Chemicals, and Reliance & Shin-Etsu results to frame performance in Asia Ex-China.

- Energy/Upstream: We discuss Reliance Industries’ views of global gas and LNG markets, the business setting for its crude-to-chemicals business, and Equinor facing shareholder pressure to do more in energy transition.

- Sustainability/Energy Transition: We discuss the WM push into sustainable products benefiting from its waste integration relative to those having to compete for waste and Valero’s ambitions in clean fuels as a growth vehicle.

- Downstream/Other Chemicals: We discuss Dow’s views of its global end-markets, North American rail carloads in chemicals being among only a few sectors showing YTD growth, and China export price weakness YoY.

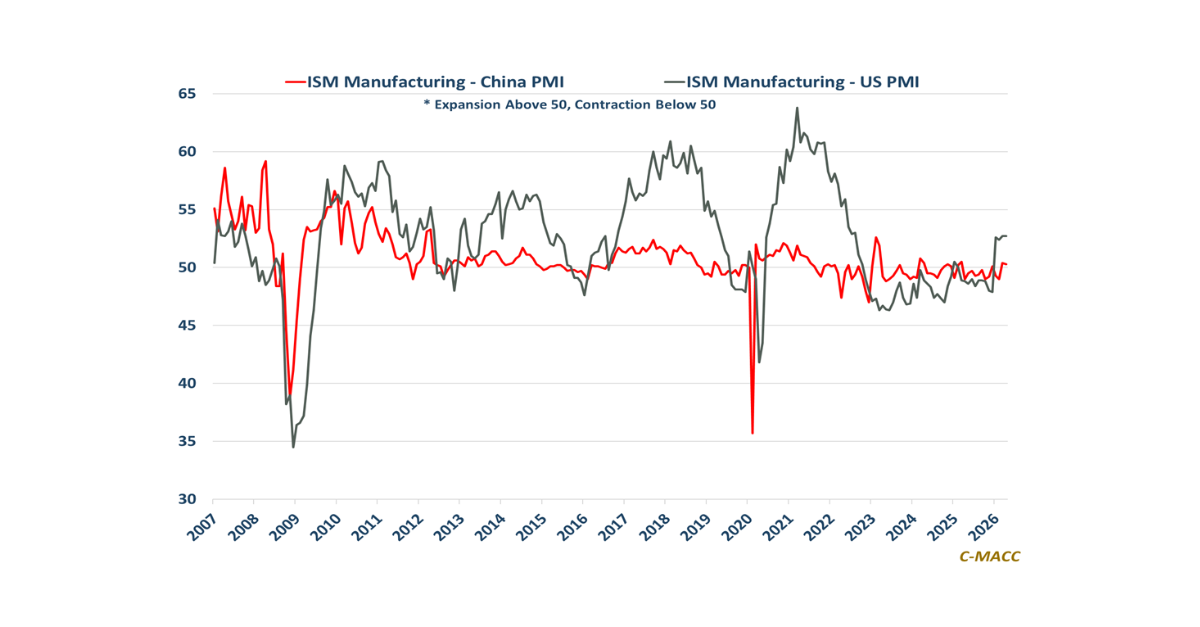

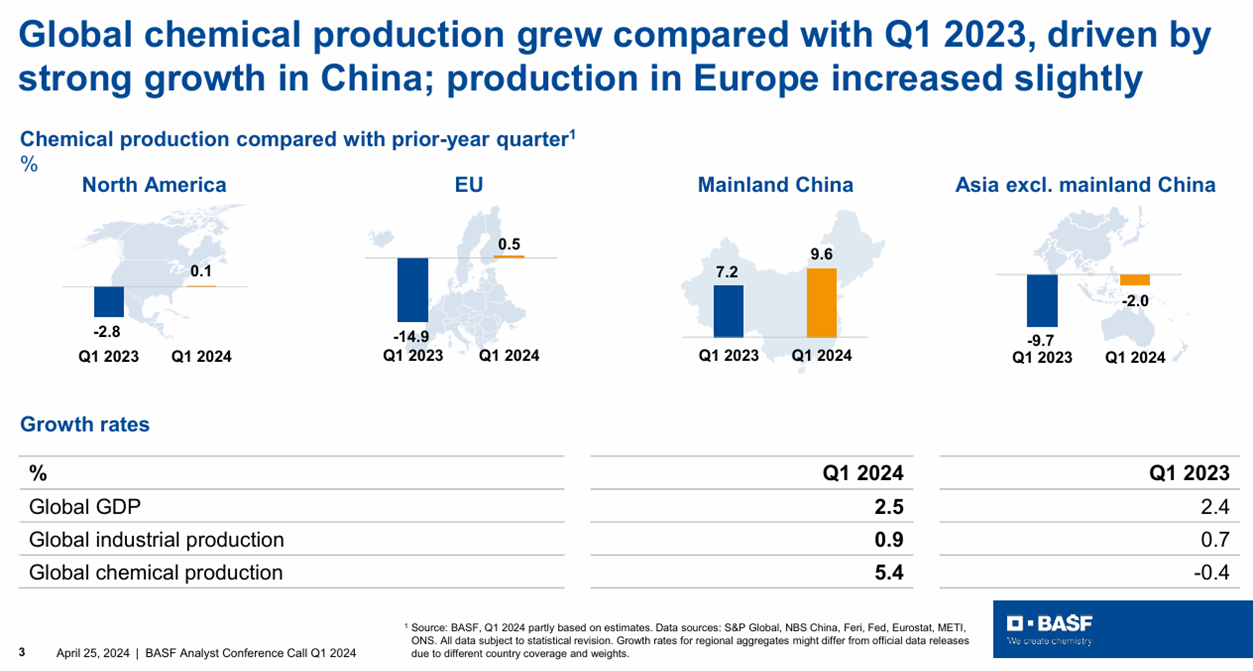

Exhibit 1: China grew its chemical production YoY in 1Q23 and 1Q24, leading the charge on global oversupply.

Source: BASF – 1Q24 Earnings Presentation, April 2024

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!