Daily Chemical Reaction

So What’Cha Want? Low Prices or More Viable Industry, Most Western Energy Transition Goals Cannot Depend on Both!

Key Findings

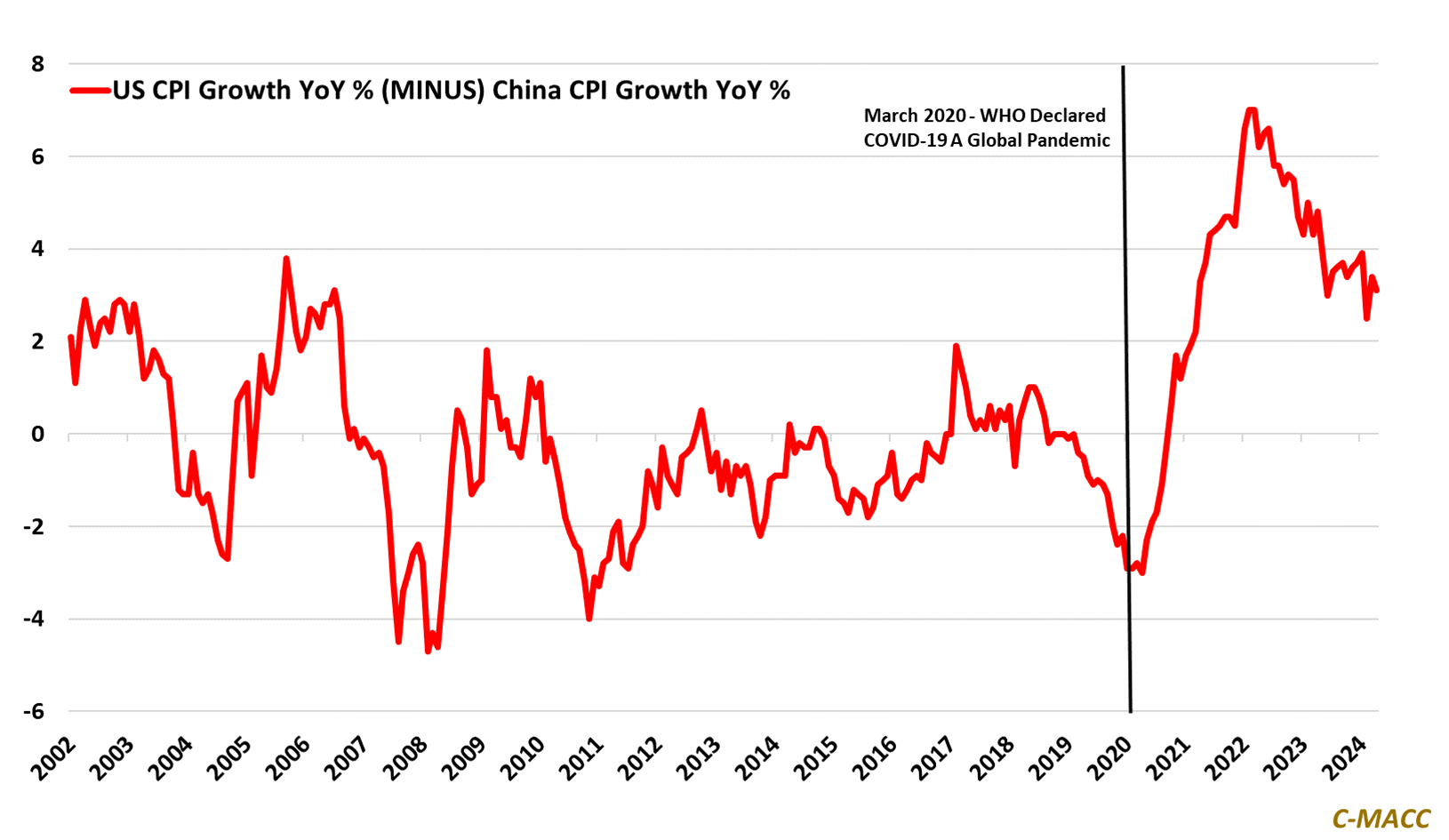

- General Thoughts: We discuss US and China CPI trends ahead of the May data releases tomorrow, as the relative development is as (if not more) important to Western industry than the absolute regional postings and trends.

- Supply Chain/Commodities: We discuss the push toward critical mineral regional supply security in high-cost areas despite low prices and the pull on low-cost chemical feedstock imports to some growth areas, such as India.

- Energy/Upstream: Global natural gas prices have risen relative to Crude oil compared to the start of 1Q24, flattening the global cost curve for many chemical products – the North American cost advantage is still significant.

- Sustainability/Energy Transition: European parliament election results are being viewed as less friendly to energy transition, which comes at a time when regional clean project incentives need to rise further to stimulate growth.

- Downstream/Other Chemicals: The US Dollar has strengthened relative to most major global currencies since 2024, which we view as more of a negative for US end-product exports than the global pull on its low-cost energy.

Exhibit 1: US CPI strength relative to China is a plus for consumers of Chinese goods, a negative for Western industry.

Source: Bloomberg, C-MACC Analysis, June 2024

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!