Daily Chemical Reaction

Farm Income Faces Downward Pressure – Input Supplier Profit Impacts Mixed; Crop Consumers Rejoice, For Now!

Key Findings

- General Thoughts: US corn and soybean prices fell to fresh YTD lows this week amid expectations for strong US (and global) production, supporting our weak agriculture economy views for 2H24 ahead of a better 2025/26.

- Supply Chain/Commodities: We discuss chemical sector 2Q reports, including Albemarle, and the different return settings currently facing seed and crop protection player Corteva relative to US fertilizer producer LSB Industries.

- Energy/Upstream: We discuss highlights from a few energy sector results and updates, ranging from Chevron to Shell, and Exelon efforts to boost power delivery with a low-risk plan that we think will likely assure a tight market.

- Sustainability/Energy Transition: We discuss low-carbon hydrogen/ammonia developments at LSB Industries and Air Products, following their 2Q24 earnings calls, and how clean energy subsidies could be assuring trouble ahead.

- Downstream/Other Chemicals: Elevated global freight rates are benefiting shippers, as shown with the Maersk profit guidance increase for 2024, but it is posing an elevated cost for US agriculture exports into some markets.

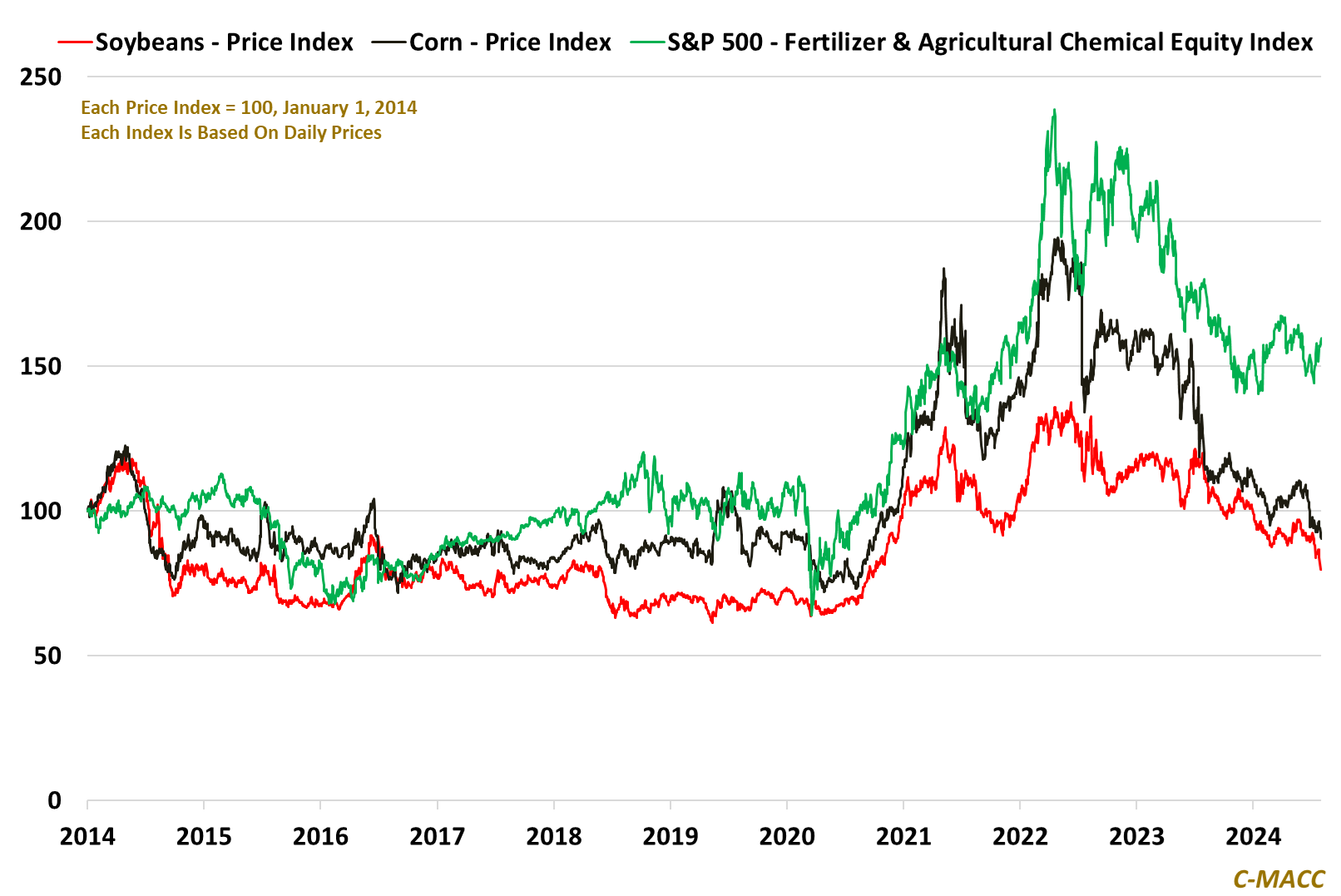

Exhibit 1: US soybean and corn prices hit a YTD low this week, implying lower farmer income, a key gauge for on-farm input & other spending. In contrast, the S&P 500 Fertilizer & Agricultural Chemical equity index reflects support.

Source: Bloomberg, C-MACC Analysis, August 2024

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!