Global Market Analysis

Margins on the Run: Chasing Profits in a Shifting World

Key Findings

- General Thoughts: On average, global crude oil refinery and ethylene margins look better YTD – until you dig deeper. Do not mistake falling costs for strength, as most margin support pockets will likely reverse by mid-year.

- Supply Chain/Commodities: Global chemical margins mask deep regional rifts—Saudi integration surges, Europe restructures, and USGC ethane cracks under pressure—feedstock flexibility and integration are differentiators.

- Energy/Upstream: Global petrochemical dynamics will shift if US shale tightens and COTC strategies abroad gain relative ground. Siemens Energy’s rebound signals a lasting upswing in electrification and infrastructure demand.

- Sustainability/Energy Transition: France’s hydrogen pullback and potentially shaky carbon removal economics spotlight a critical question: can clean tech scale without firmer economics—or will policy alone carry the load?

- Downstream/Other Chemicals: Trump’s tariff shockwaves are redrawing global freight flows—container and trucking markets now face a volatile mix of frontloading, margin pressure, and long-term structural upheaval.

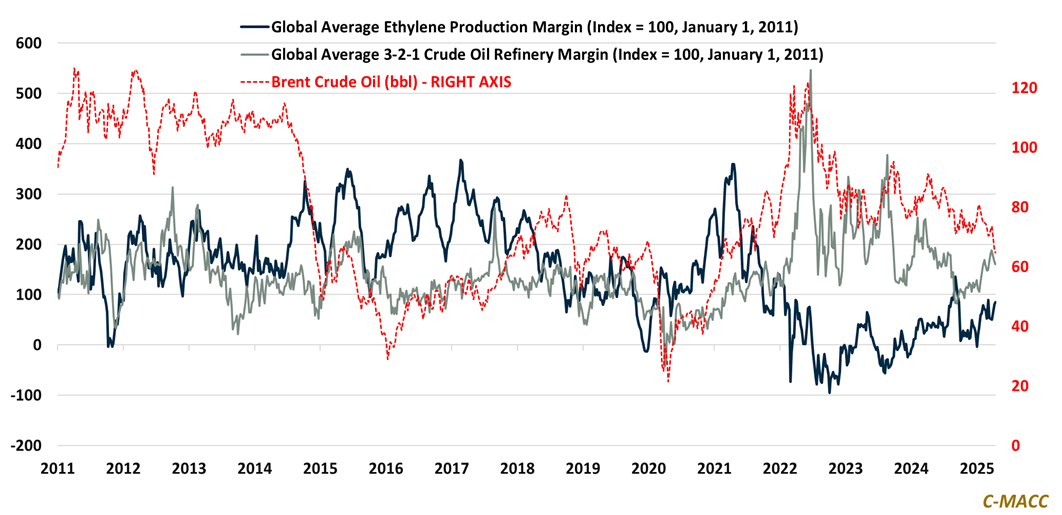

Exhibit 1: Global average ethylene and refinery margins have increased YTD, incentivizing stronger 2Q25 run rates.

Source: Bloomberg, C-MACC Analysis, April 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!