Base Chemical Global Analysis

Global Weekly Catalyst No. 279

- General Thoughts: The Aramco and Braskem 1Q earnings call highlighted a strategic divergence, as one bets on global integration and scale, while the other focuses on feedstock agility, regional resilience, and sustainability.

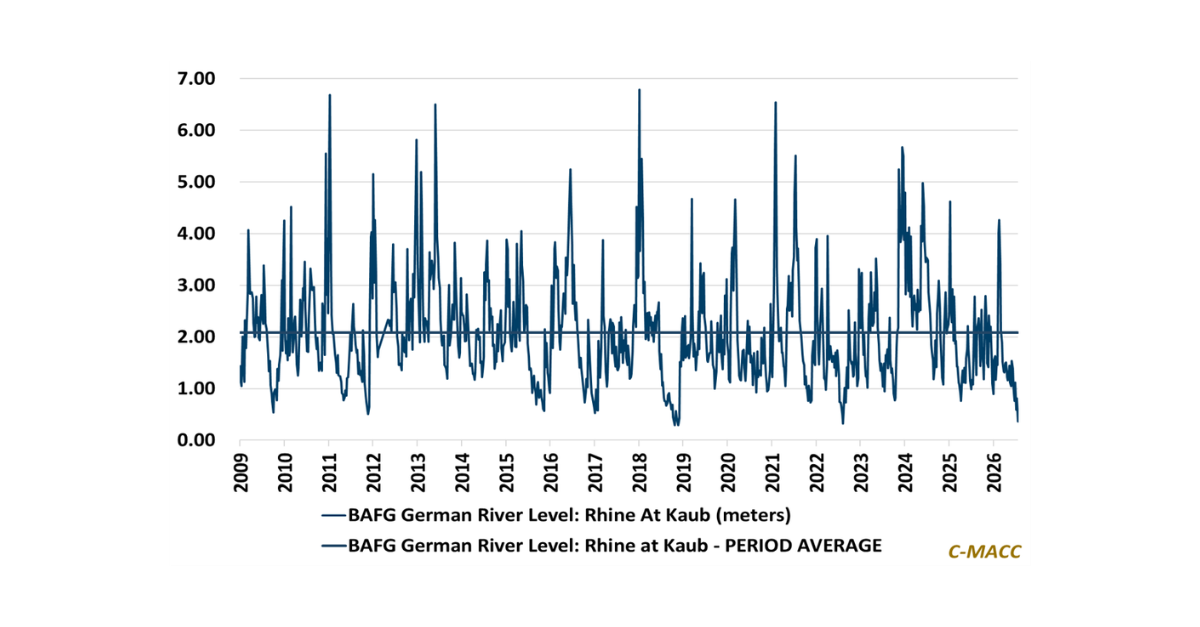

- Feedstocks & Energy: Global feedstock economics are fracturing—old models are breaking down as regional volatility, shifting co-product values, and supply chain mismatches redefine what “low-cost” really means.

- Olefins: USGC olefins saw brief support last week from production issues, but global softness, weak derivative demand, and looming international capacity additions suggest recent spot price strength could be short-lived.

- Other Base Chemicals: Methanol’s continued global slide highlights a widening global imbalance, as resilient supply outpaces lackluster demand, raising pressure on Southeast Asia just as arbitrage support begins to crack.

- Agriculture: Tight supply and strong domestic corn-driven demand support US (and global) nitrogen prices. However, rising natural gas costs and looming global supply improvements could flip sentiment by 2H25.

- Refining & Biofuels: US refining margins remain strong amid regional strain despite tightening crude flows. At the same time, a new UK trade deal looks like a plus for ethanol exports, though structural headwinds persist.

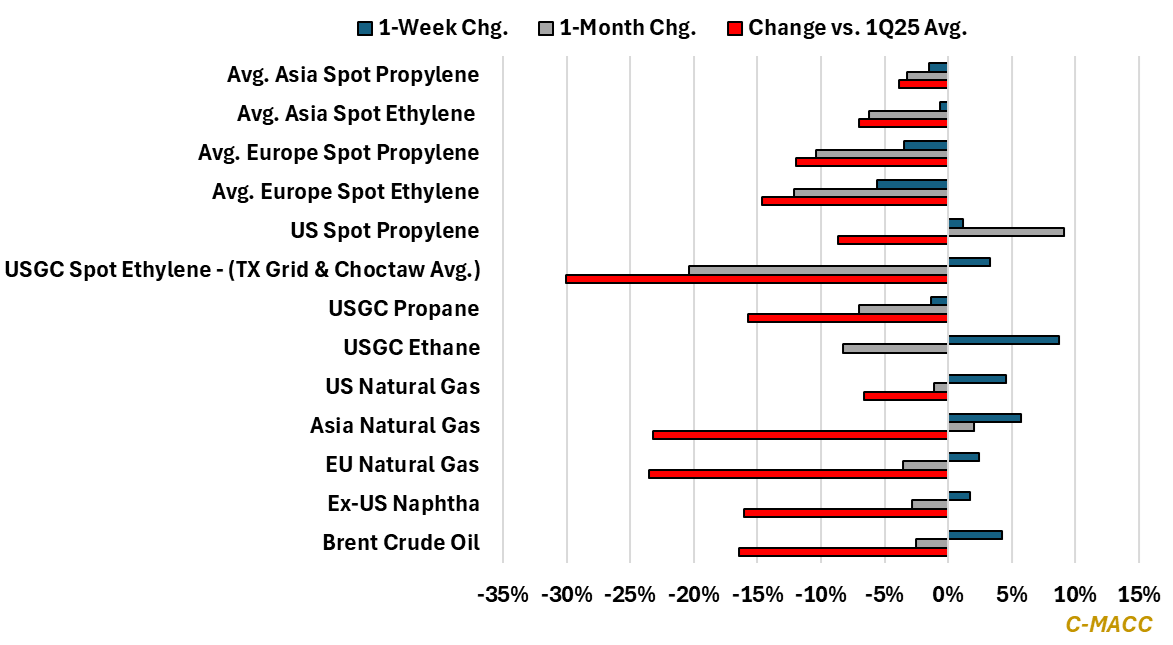

Exhibit 1 – Chart of the Day: Global feedstocks and base chemical prices are broadly lower than their 1Q25 averages.

Source: Bloomberg, C-MACC Analysis, May 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!