C-MACC Sunday Executive Summary

In Energy Markets, Scarcity Is the New Alpha

- Clean energy minerals have underdelivered against narrative hype, with lithium down, prices anchored near marginal cost, and forecasts consistently failing to grasp the gritty, sobering economics of actual supply chains.

- Copper’s scarcity concerns are legitimate: aging mines, delayed projects, rising capital expenditures, and structural inertia suggest that supply will struggle to meet demand, favoring the commodity over equities.

- Lithium’s two-speed market favors low-cost, policy-backed producers like SQM and Rio Tinto, while high-cost operators struggle as prices fall below marginal cost amid fragmented incentives and investor overreach.

- Hydrogen’s momentum fractured in 2025 as policies buckled under political shifts, market fragmentation, and institutional pressure—proof that ambition without durable systems invites failure and stranded infrastructure.

- From the resurgence of natural gas to freight volatility and pressure on methanol margins, the energy transition is colliding with real-world bottlenecks. Winners will understand constraints, capital, and consequences first.

- Companies Mentioned: Tesla, SQM, Rio Tinto, Standard Lithium, ExxonMobil, BHP, Methanex, Celanese, Wacker, Kuraray, LyondellBasell, Mitsui, Entergy, We Energies, Cheniere, Canadian Natural Resources, Energy Transfer, Kyushu Electric, Eastman, Calpine, Dick’s Sporting Goods, Best Buy, Boeing, Toyota

- Products Mentioned: Lithium, Copper, Nickel, Cobalt, Methanol, Acetic Acid, Vinyl Acetate Monomer (VAM), Ethylene, Natural Gas, LNG (Liquefied Natural Gas), Coal, Hydrogen, Ammonia

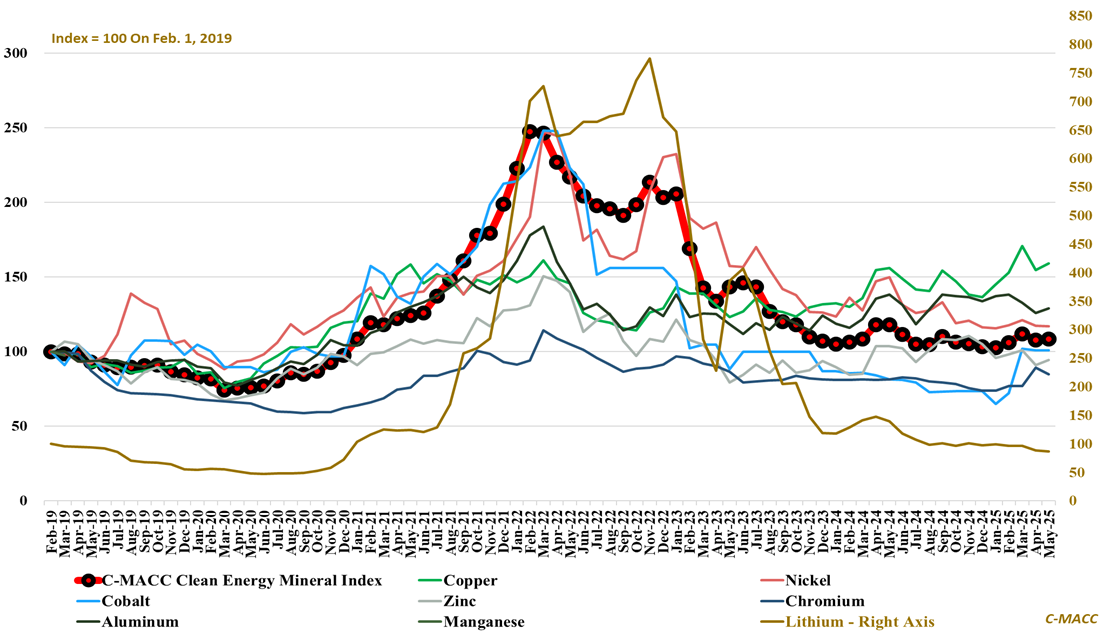

Exhibit 1: The C-MACC Clean Energy Mineral Index has increased 5% YTD, up only 8% since the start of 2019.

Source: Bloomberg, C-MACC Analysis, June 2025

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!