Global Market Analysis

Sentiment High, Margins Thin: Fragile Gains Ahead

Key Findings

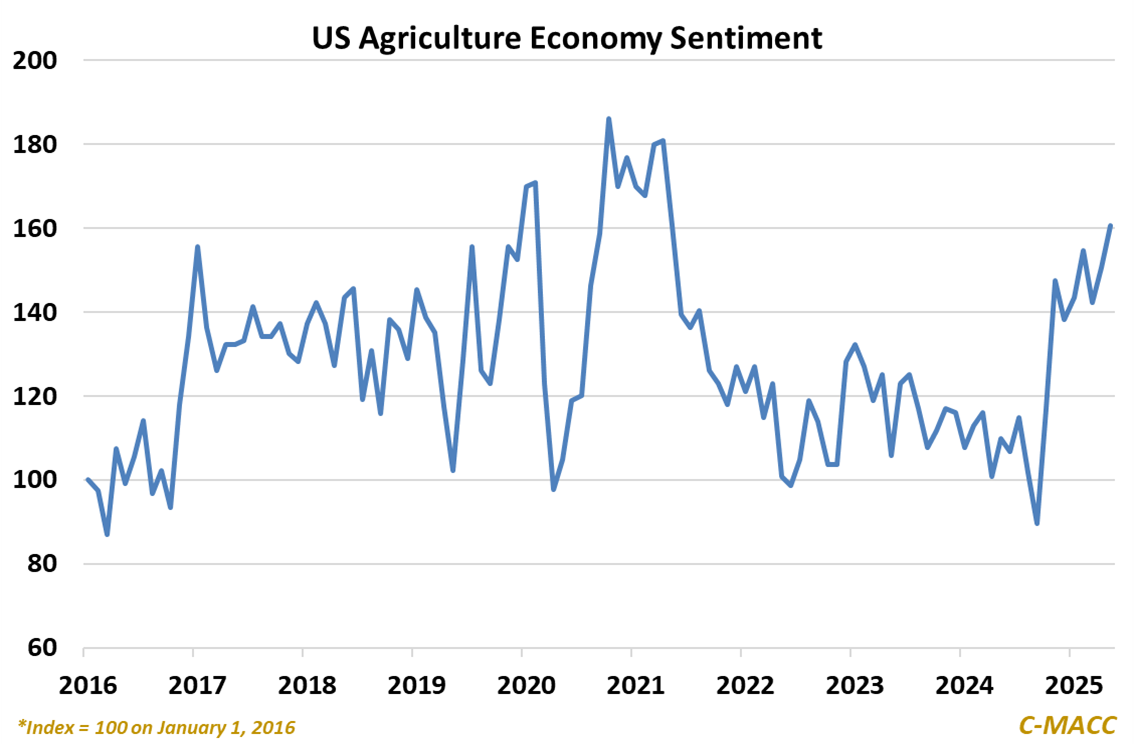

- General Thoughts: US farmer sentiment has surged, but beneath the optimism lie structural pressures, including crop price weakness, lower margins, and a volatile demand setting, which creates a precarious setup for 2H25.

- Supply Chain/Commodities: Strong global plantings are trending positively for crop input use, bringing destocking activity to a halt, which will benefit suppliers in 2H25. US ammonia margins are lower YoY, now near YTD lows.

- Energy/Upstream: US shale’s capital discipline, strong free cash flow, and depressed valuations could set the stage for rerating, while global gas consolidation and infrastructure demand reinforce long-term sector resilience.

- Sustainability/Energy Transition: Global ethanol and SAF markets expose a widening gap between climate targets and policy execution, as stalled US reforms, EU cost burdens, and trade frictions destabilize corn and fuel markets.

- Downstream/Other Chemicals: Strained US barge infrastructure and slow towboat investment pose a risk of disrupting freight and agricultural markets, potentially lessening positive sentiment toward international trade.

Exhibit 1: US agriculture economy sentiment has surged to a multi-year high – risk of decline appears high in 2H25.

Source: Bloomberg, C-MACC Analysis, June 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!