Global Market Analysis

Margins Hold, Volumes Fade: Global Trade Reshapes Industrial Chemistry

Key Findings

- General Thoughts: Global refining margins have risen YTD on tight product balances, but chemical producers face persistent margin compression as oversupply, weak demand, and policy-driven volatility cloud the 2H25 outlook.

- Supply Chain/Commodities: Europe’s chemical sector faces structural strain as restructurings accelerate, margins decouple from utilization, and global cost competitiveness shifts to more integrated, cost-advantaged regions.

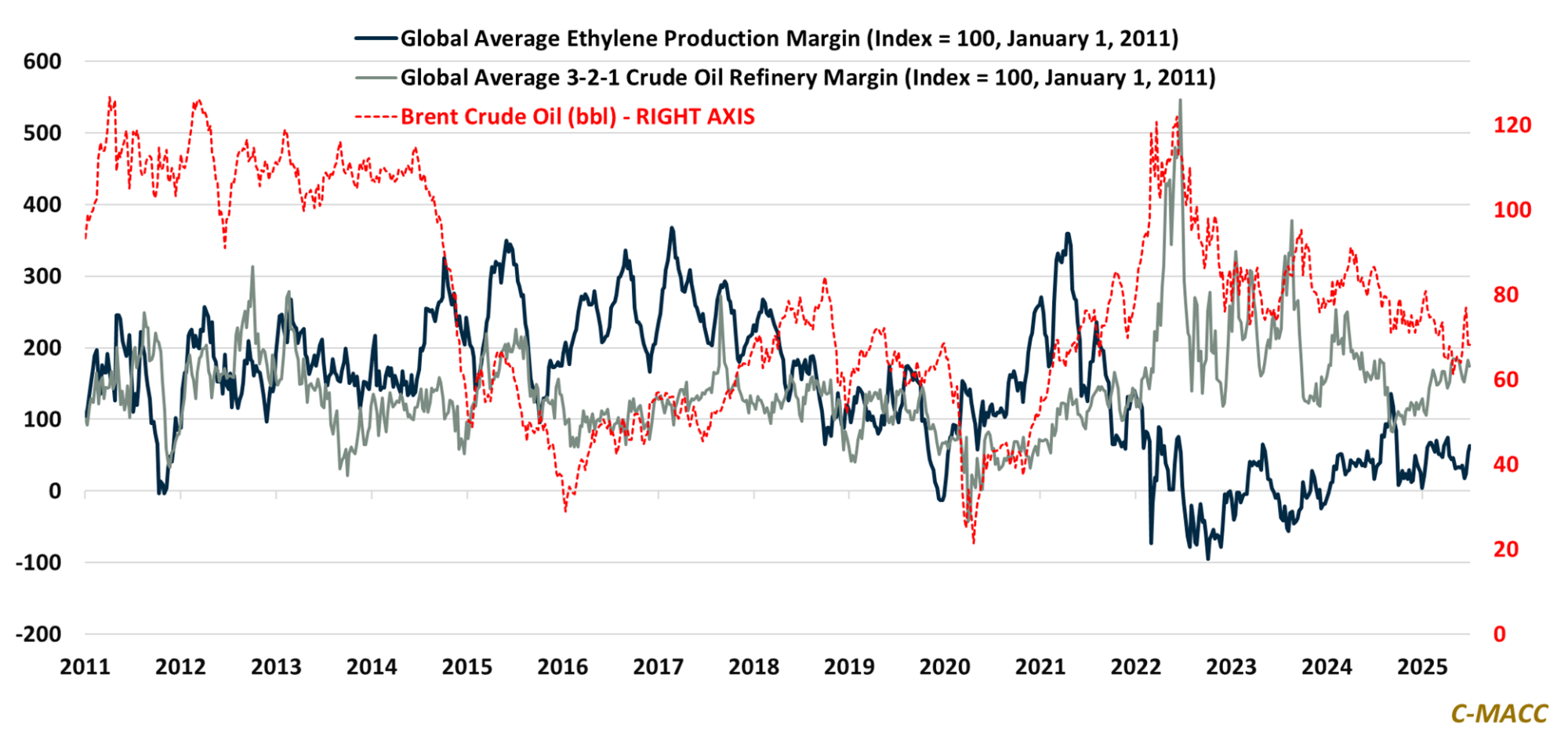

- Energy/Upstream: Global refining margins climbed on tight product markets and low crude input costs. However, global tightness and structural feedstock imbalances in naphtha signal sustained volatility into 2H25.

- Sustainability/Energy Transition: EU Parliament’s proposed vehicle plastics mandate favors integrated recyclers and established resin players, while intensifying margin pressure across non-integrated, high-cost recyclers.

- Downstream/Other Chemicals: Strong US crop progress, a weaker dollar, and Brazil’s harvest delays/logistic issues are aligning to boost US corn’s export competitiveness amid rising policy risk and shifting global trade flows.

Exhibit 1: Tight capacity utilization has benefited global refinery margins YTD, less so for global ethylene producers.

Source: Bloomberg, C-MACC Analysis, July 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!