Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

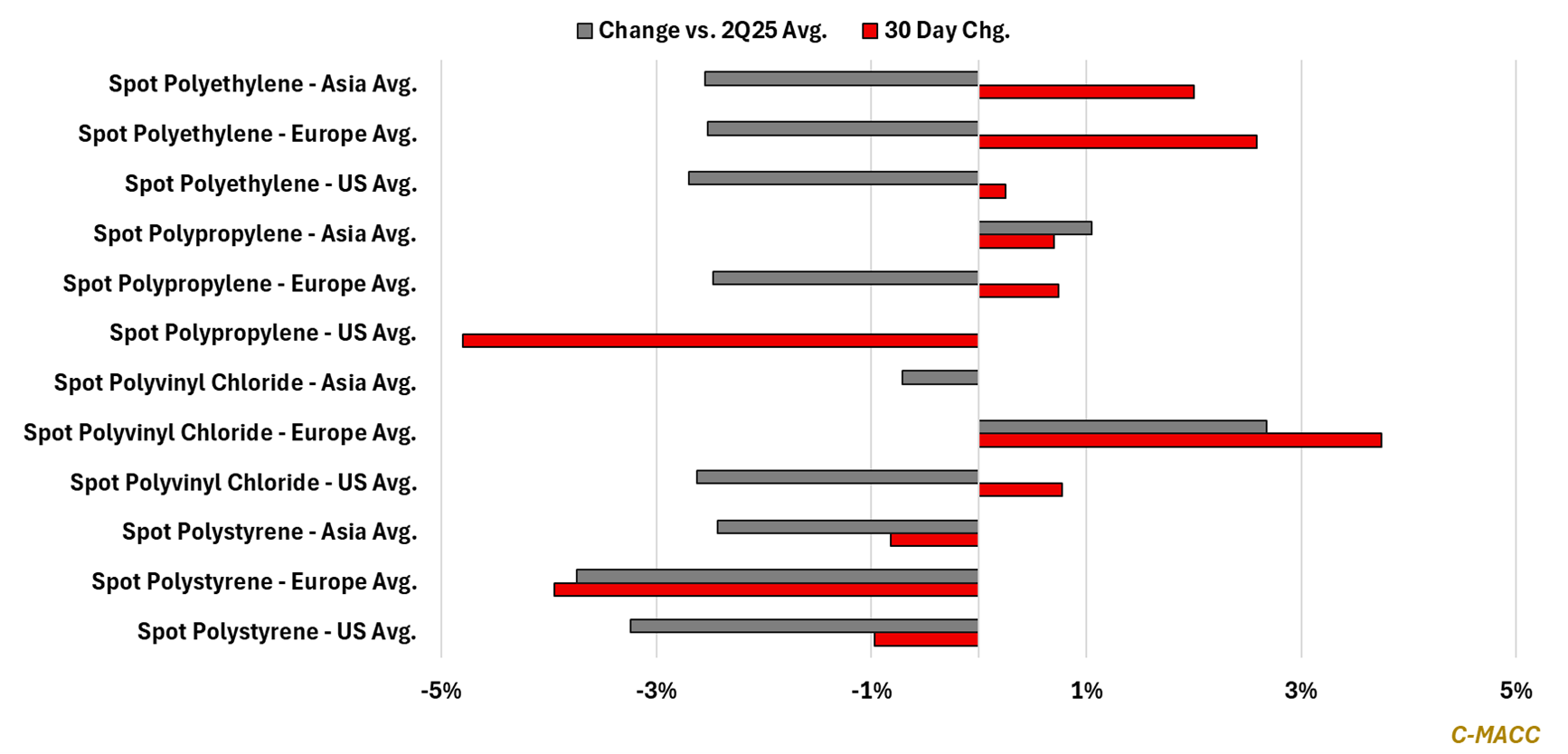

- General Thoughts: Oversupply persists across most polymer markets despite some evidence of price strength during the past 30 days. We anticipate a weak 2H25 for most global polymer markets before improvement emerges in 2026.

- Polyethylene (PE): Global PE spot prices show some support from earlier cost spikes, but fading momentum, weak demand, and regional margin pressure suggest range-bound conditions are more likely than otherwise in 2H25.

- Polypropylene (PP): Global PP spot prices face renewed pressure as soft demand, falling feedstock costs, and ample supply override pricing efforts, pointing to likely margin stress and cautious producer strategies in 2H25.

- Polyvinyl Chloride (PVC): Despite global PVC oversupply, plant closures, rising Chinese prices, and regulatory shifts suggest limited near-term downside, with structural changes shifting markets for a more balanced 2026 recovery.

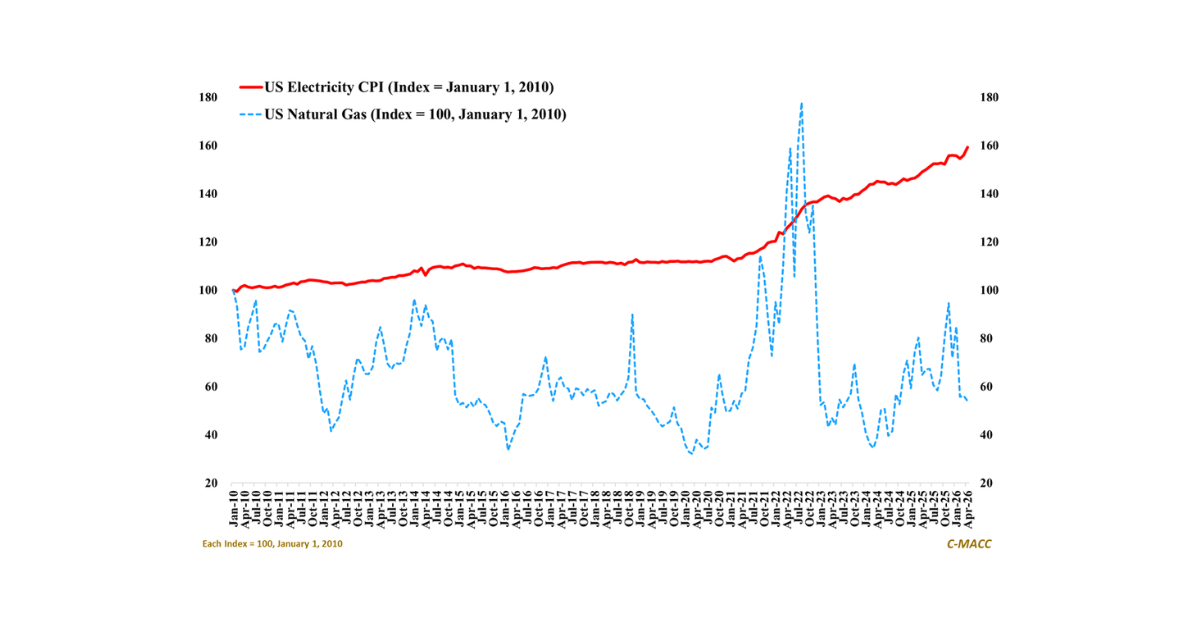

- Other Sector Developments: Crude oil prices support in the US$70/bbl range suggests polymer prices will unlikely return to 2Q25 lows in 3Q25, and absent unplanned events, 1Q25 price points look out of reach for most in 2H25.

Exhibit 1 – Chart of the Day: Global spot PE shows the broadest strength since 30 days ago, but momentum is fading.

Source: Bloomberg, Company Reports, C-MACC Analysis, July 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!