Global Market Analysis

Crop It Like It’s Hot: Yield Ain’t Enough Anymore, On-Farm Margins Matter

Key Findings

- General Thoughts: With 2H25 crop prices pressured and 2026 farmer affordability strained, fertilizer and input sentiment may weaken, despite resilient long-term fundamentals that still favor strategic, integrated positioning.

- Supply Chain/Commodities: As farmers defend yield amid falling prices, demand for crop protection and nutrients remains resilient, but 2026 acreage shifts threaten to reveal economics eclipsing agronomy in input strategy.

- Energy/Upstream: Energy Transfer exemplifies midstream’s evolution, linking US infrastructure to global markets, expanding export optionality, and steadily eroding the low-cost gas and NGL edge many domestic buyers rely on.

- Sustainability/Energy Transition: Blue ammonia is positioning to become critical infrastructure by 2026, as CBAM, carbon prices, and growing locked-in offtake increasingly elevate it from ambition to strategic geopolitical lever.

- Downstream/Other Chemicals: Strong crop input demand in 2025 masks a 2026 reset, where supply outpaces sentiment, margins tighten, and disciplined, service-driven input players outperform volume-dependent peers.

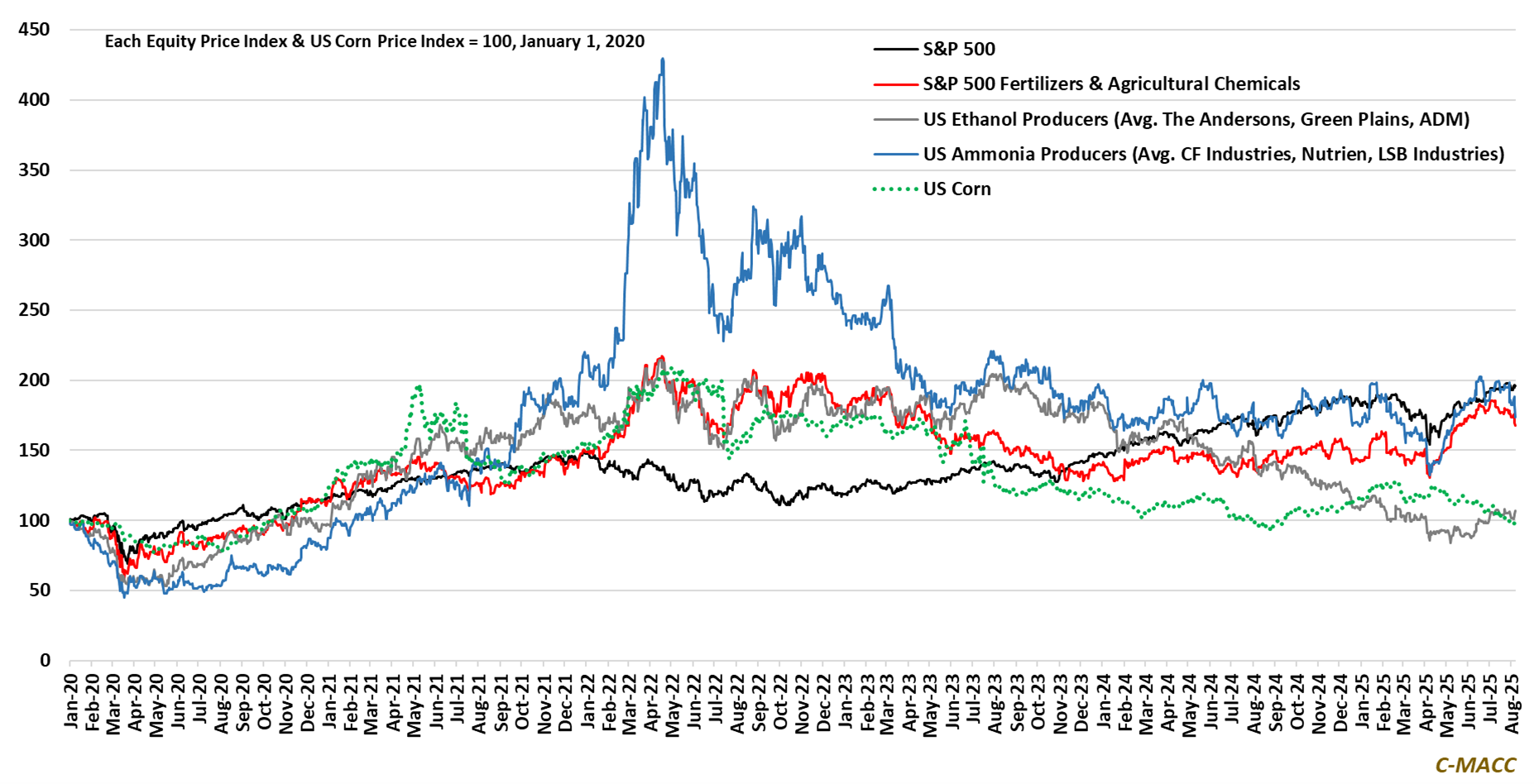

Exhibit 1: S&P Fertilizers & agricultural chemical equities fall from 2025 YTD highs amid concerns with low crop prices.

Source: Bloomberg, C-MACC Analysis, August 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!