C-MACC Sunday Executive Summary

Every Moat You Make: Structure Beats Scale, Returns Compound

- Structure, not scale, determines valuation, capital access, and resilience as oversupply, policy volatility, and higher rates punish complexity yet reward clarity, focus, optionality, disciplined execution, and transparency.

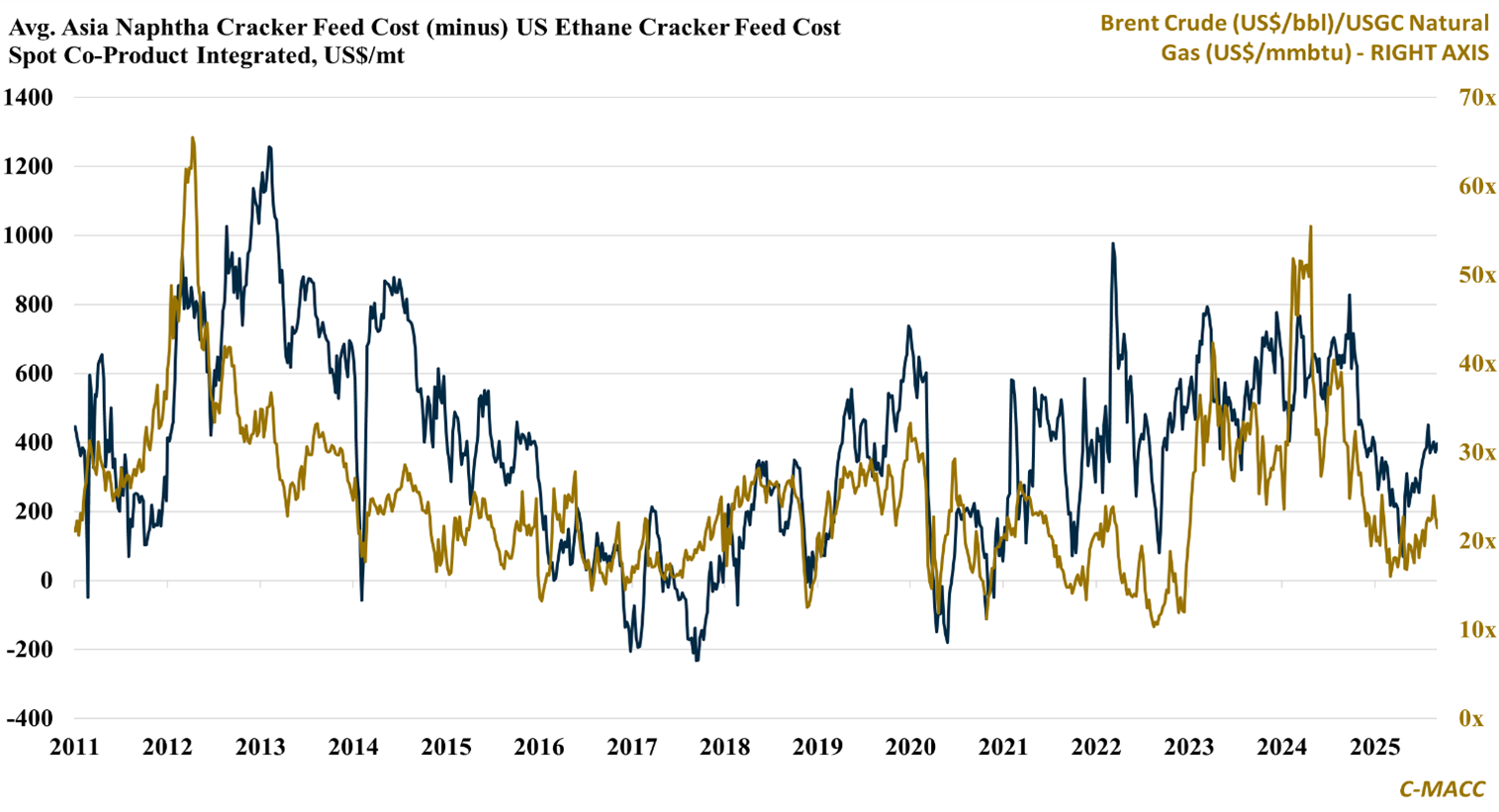

- Petrochemicals bifurcate: North America optimizes from low-cost ethane while Korea mandates petrochemical capacity cuts and Japan pushes consolidation; 2026 US/Qatar additions further entrench advantage.

- Agriscience restructures to isolate liability and unlock growth: Corteva considers separation; BASF Ag solutions continues to eye listing; Syngenta reorganizes to biologicals and IP, compressing costs and widening optionality.

- Mining consolidates around a long-term “scarcity” theme: Anglo Teck advances; Rio Tinto elevates lithium; BHP expands copper; Vale deepens nickel exposure; securing bottlenecks sets costs, certainty, and leverage.

- Otherwise, clarity premiums, policy friction, and input-cost bifurcation control playbooks: copper strengthens, lithium whipsaws, catalysts function as OpEx moats, China’s PP exports compress Western spreads.

- Companies Mentioned: Dow, CPChem, QatarEnergy, Lotte Chemical, Yeochun NCC, HD Hyundai, Mitsubishi Chemical, Mitsui Chemicals, Idemitsu Kosan, Corteva, BASF, Syngenta, Kraft Heinz, Anglo American, Teck, Rio Tinto, Arcadium Lithium, Vale, BHP, CATL, Albemarle, ExxonMobil, Superior Graphite, SQM, Prime Polymer, Westlake, Diamond, LyondellBasell, Ineos, Technip Energies, Ecovyst, Grace, UOP, Shell, Zeolyst, Aramco, Sinopec, Phillips 66, Cenovus, Marathon, Valero, ConocoPhillips, Microsoft, Google, Amazon (AWS), Meta, Xylem, Pentair, Veolia, TSMC, Intel, Samsung, ABB, Schneider Electric, Trane Technologies

- Products Mentioned: Oil, Natural Gas, Brent Crude, LNG, Naphtha, Ethane, Ethylene, Propylene, Polyethylene (PE), Polypropylene (PP), Polyvinyl Chloride (PVC), Polystyrene (PS), Diesel, Jet Fuel, Distillates, Copper, Coal, Lithium, Nickel, Graphite, Soybean, Corn, Cotton

Exhibit 1: Oil–gas parity drives naphtha–ethane spreads, forcing global restructuring and corporate strategic patience.

Source: C-MACC Estimates, September 2025

See PDF below for all charts, tables and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!