Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

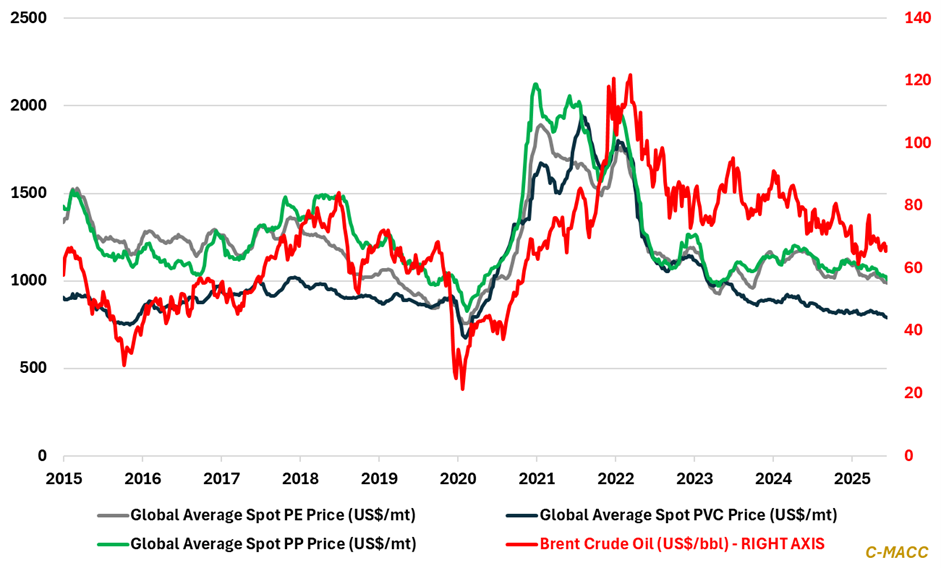

- General Thoughts: Global polymer markets confront structural repricing as oversupply, weak demand, and shifting trade flows anchor benchmarks near pandemic-era lows in mid-September, despite selective regional divergence.

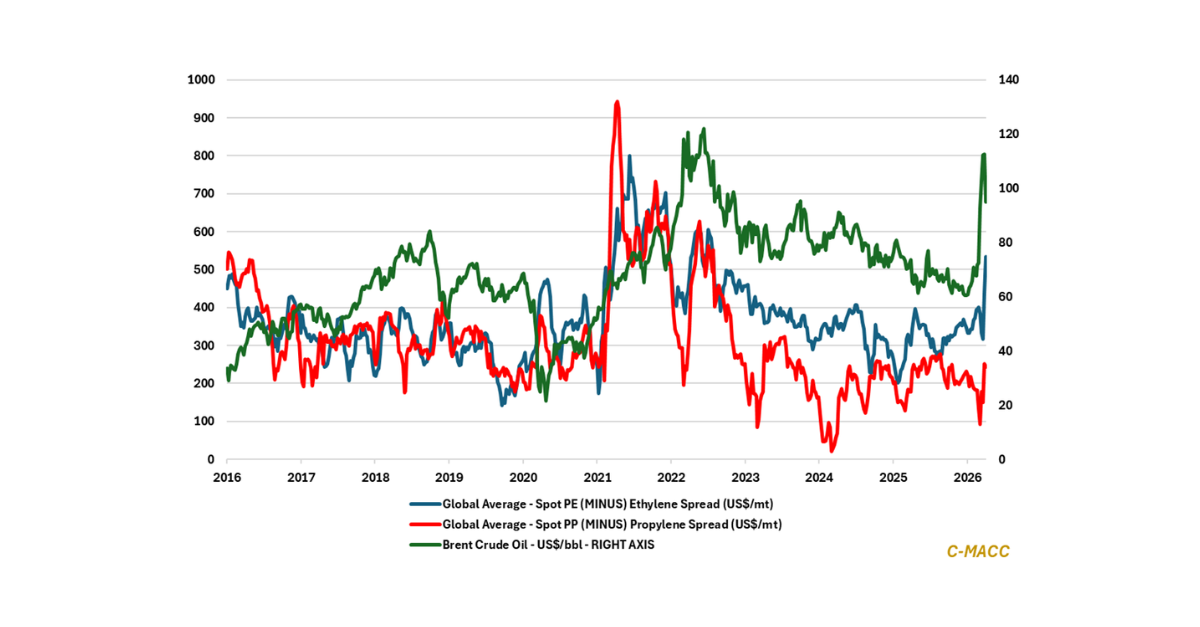

- Polyethylene (PE): Global spot PE markets were mainly steady last week as US exports pressured Southeast Asia, Europe fell to new lows, China’s restocking disappointed, and Middle Eastern producers conceded to October cuts.

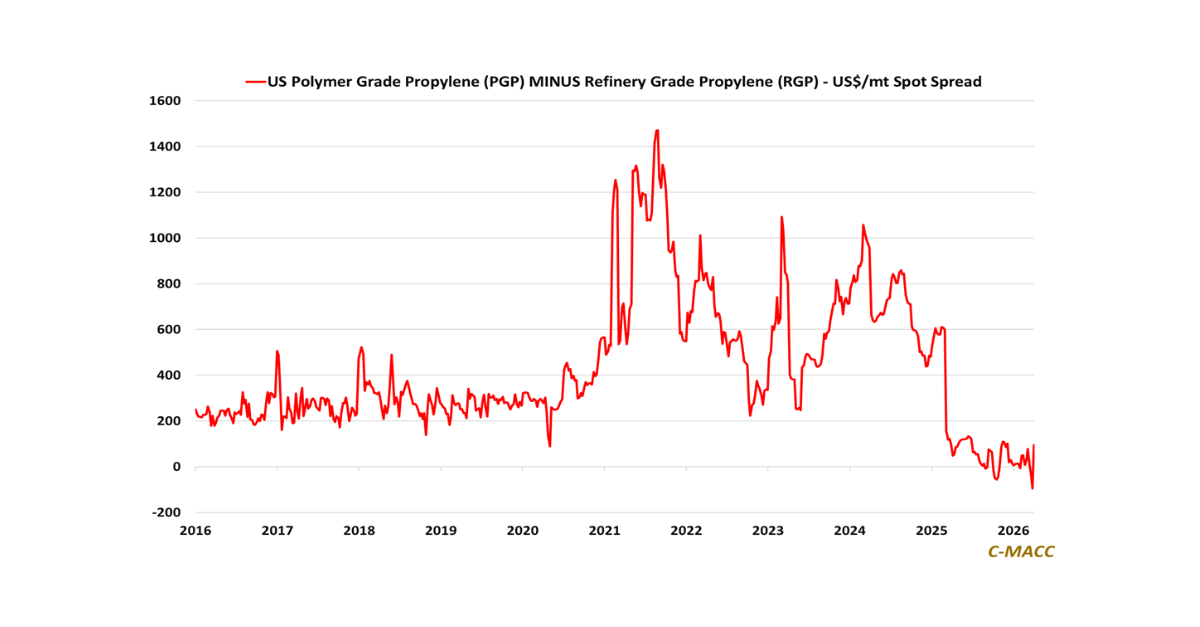

- Polypropylene (PP): Global spot PP markets slipped further last week as the US, Europe, and Asia saw price drops, PGP costs firmed, inventories swelled, Vietnam hit five-year lows, and China’s structural overcapacity deepened.

- Polyvinyl Chloride (PVC): Global average spot PVC prices hit fresh lows last week, as US spot prices slid, China held near its 2025 lows, and Europe faced surging Asian inflows. India reflected one of the only pockets of global strength.

- Other Sector Developments: Global integrated polymer production costs climbed last week, with naphtha, ethane, and propane edging higher, while polymer prices slid lower, compressing margins across most global producers.

Exhibit 1 – Chart of the Day: Resin and regression oversupply drags global polymer prices back toward pandemic lows.

Source: Bloomberg, Company Reports, C-MACC Analysis, September 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!