Base Chemical Global Analysis

Global Weekly Catalyst No. 301

- General Thoughts: Global chemical markets entered 4Q25 in synchronized deflation, where feedstock softness, rationalization, and integration depth, not demand recovery, will likely define competitiveness into early 2026.

- Feedstocks & Energy: Global chemical feedstock deflation in 4Q25 signals tightening margins and a volatile 1H26 defined by LNG-driven gas dynamics, naphtha oversupply, and structural margin compression relative to 1H25.

- Olefins: Global olefin markets fracture in 4Q25 as outages, weak demand, and feedstock divergence compress margins, rewarding integrated, flexible operators and likely exposing structural inefficiencies well into 2026.

- Other Base Chemicals: Global benzene weakens on soft demand, methanol steadies amid regional gas volatility, and chlor-alkali remains soft, framing weak 4Q conditions and integration-driven regional margin divergences.

- Agriculture: Fertilizer markets in 4Q25 reflect tightening ammonia supply, muted crop exports, and cautious restocking, setting the global stage for a volatile, gas-driven recalibration of nitrogen economics through 1H26.

- Refining & Biofuels: Ethanol margins softened while refining spreads held firm WoW, signaling a late-2025 plateau that transitions into 1H266, defined by policy-driven ethanol support and refining margin normalization.

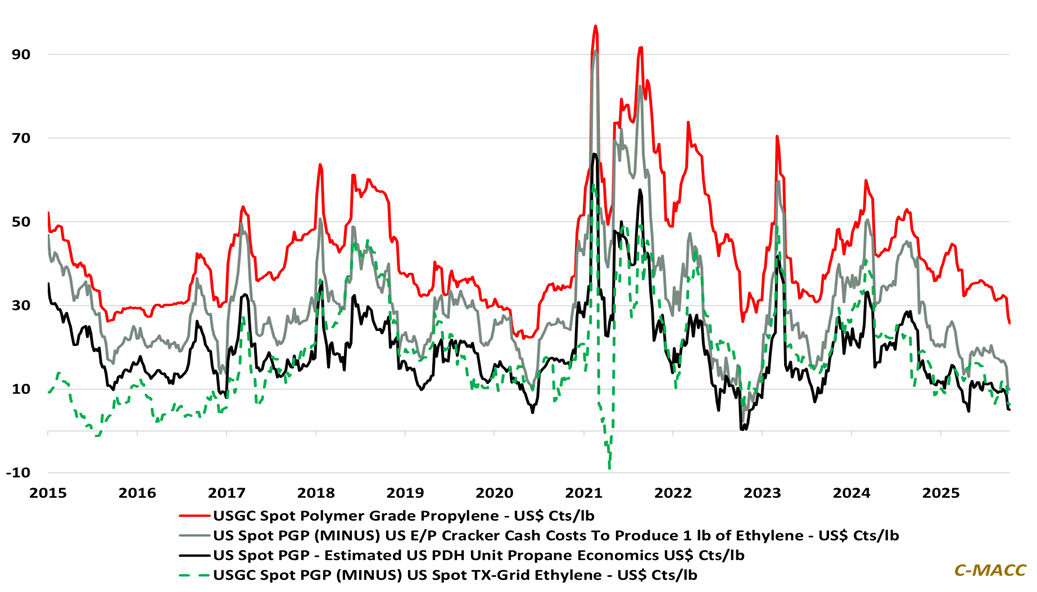

Exhibit 1 – Chart of the Day: USGC PGP spot prices fall to a multi-year low amid oversupplied derivative markets.

Source: Bloomberg, C-MACC Estimates, October 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!