Global Market Analysis

Integrated or Irritated: Who’s Stocked the Return Lotion for 2026?

Key Findings

- General Thoughts: The late 2025 commodity landscape rewards integrated, low-cost, logistics-agile producers, while 2026 will test who can sustain profits as new capacity, cost volatility, and oversupply pressures collide.

- Supply Chain/Commodities: Ammonia and aluminum prices sit near 2025 highs as energy, policy, and logistics constraints benefit cost-advantaged, integrated producers while hurting carbon-heavy, power-intensive players.

- Energy/Upstream: As global refinery capacity shifts steadily toward Asia, market balance will stay in flux, with long-term competitiveness increasingly anchored in feedstock-aligned, policy-driven, chemically integrated hubs.

- Sustainability/Energy Transition: Capital is rotating to power-first platforms, rewarding secured generation offtake and contracted uptime, as utility growth lags and time-to-power eclipses cost as the decisive advantage.

- Downstream/Other Chemicals: As global supply chains rewire under trade and cost pressure, US agriculture and industrial procurement are shifting from price optimization to resilience-led, capability-driven competitiveness.

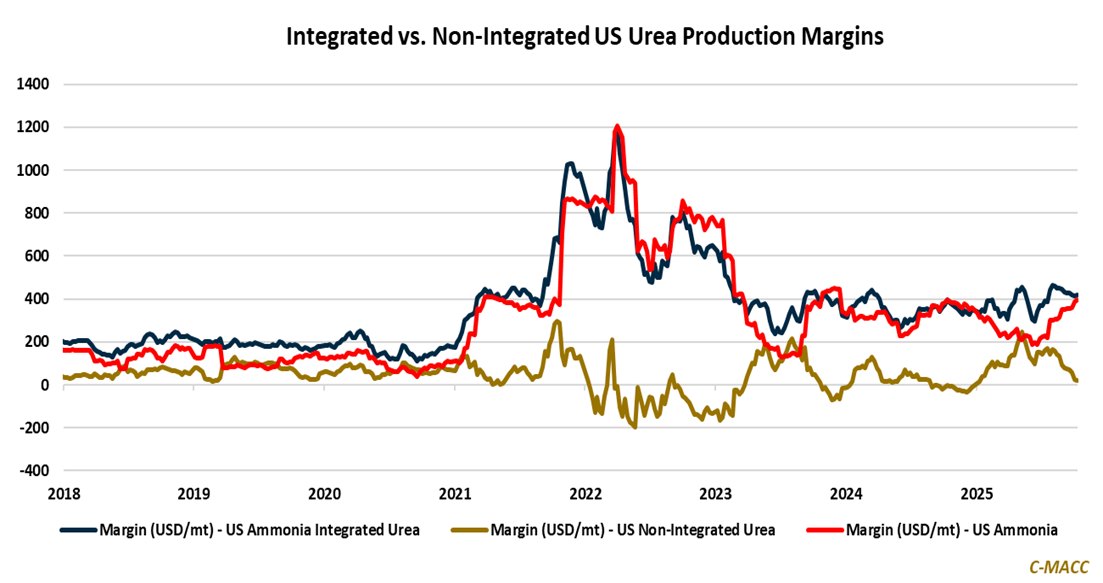

Exhibit 1: Integrated chains outperform non-integrated urea producers as gas volatility reshapes margins structurally.

Source: Bloomberg, C-MACC Analysis, October 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!