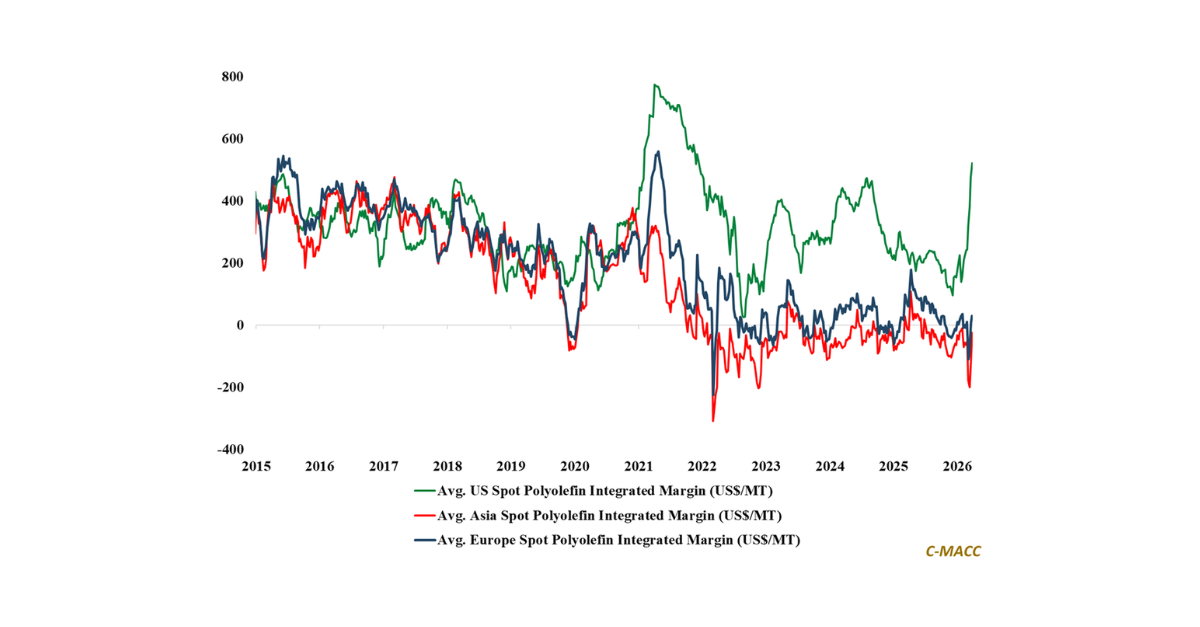

Polymer Global Analysis

Resin To Riches: Weekly Plastic Market Insights

- General Thoughts: Global polymer producers enter late-October’s 3Q25 reporting season defensive, not delusional, amid oversupply and flatter cost curves; we expect cash preservation and capex deferral focus over demand optimism.

- Polyethylene (PE): Global PE markets tread an uneasy floor, as Saudi cuts, Asian weakness, and modest US draws signal stability without strength, where sustained discipline and low integrated cost define near-term competitive advantage.

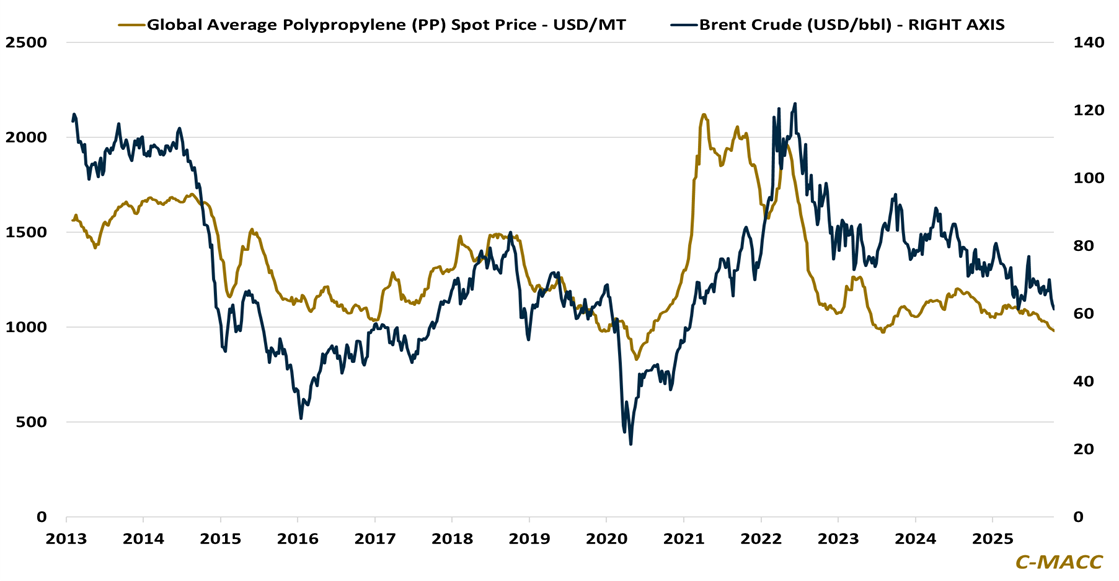

- Polypropylene (PP): Global PP faces synchronized oversupply and feedstock deflation; Chinese production expansion and low PGP prices pull prices lower, rewarding integrated PP producers relative to most non-integrated operators.

- Polyvinyl Chloride (PVC): Global PVC price steady unevenly as housing signals tentative thaw; trade barriers, EDC demand, and selective rationalization cushion downside while sustained oversupply caps meaningful recovery potential.

- Other Sector Developments: Tight feedstock spreads persist as naphtha and propane weaken; USGC propane’s slide versus ethane deepens the “cheap-C3” narrative, though it hasn’t yielded durable downstream derivative pricing power.

Exhibit 1 – Chart of the Day: Falling crude-oil-linked feedstocks add downward pressure to global PP markets.

Source: Bloomberg, C-MACC Estimates, October 2025

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!