Global Market Analysis

After the Detour: Cost Curves Reassert Control, Further Exposing Europe’s High-Cost Chemical Base

Key Findings

- General Thoughts: Red Sea freight normalization could compress Western chemical market premiums, including for methanol, exposing cost curves, trade defenses, and discipline as differentiators in an Asian-led price setting.

- Supply Chain/Commodities: Petrochemical restructuring now hinges on who controls advantaged products and logistics, as Braskem, Lotte, and INEOS strive to redraw global value chains around gas-based economics.

- Energy/Upstream: Global chemical feedstock spreads remain the core driver of project economics, rewarding those who benefit from low-cost product flows from the US, including Chevron, Occidental, and Navigator.

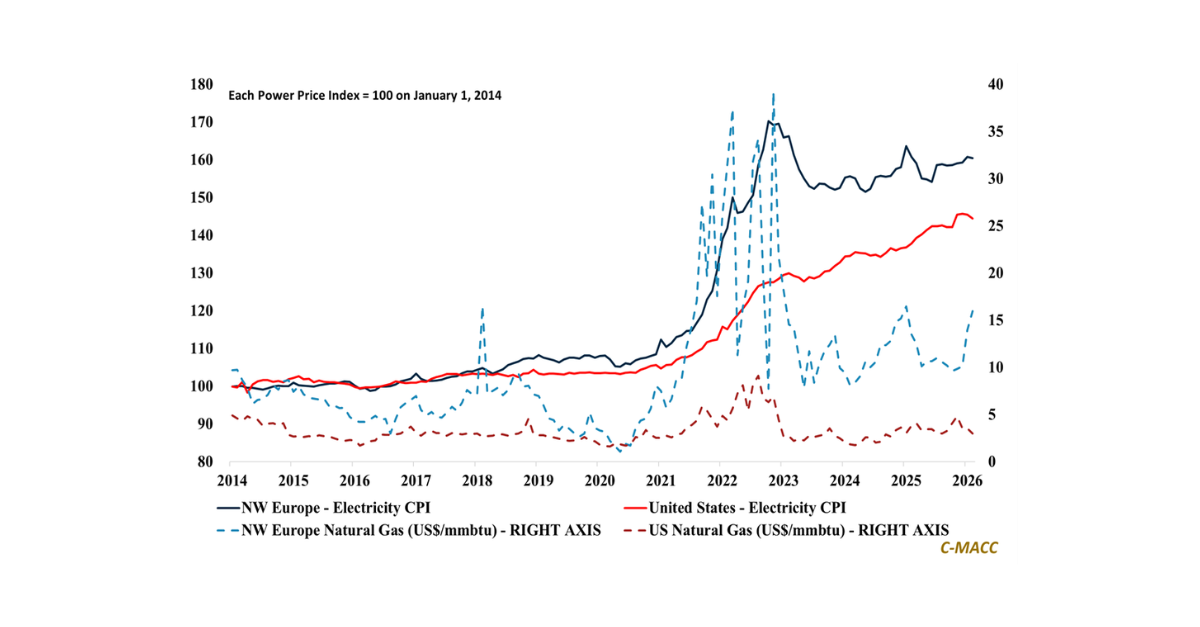

- Sustainability/Energy Transition: Europe’s tightening carbon regime and CBAM silently reprice trade flows, positioning low-carbon products and reliable low-cost power as the next legitimate global reserve currency.

- Downstream/Other Chemicals: Demand indicators decouple from macroeconomic easing, leaving OEMs, farmers, and chemical buyers constrained by liquidity, confidence, and still varied but disrupted trade policies.

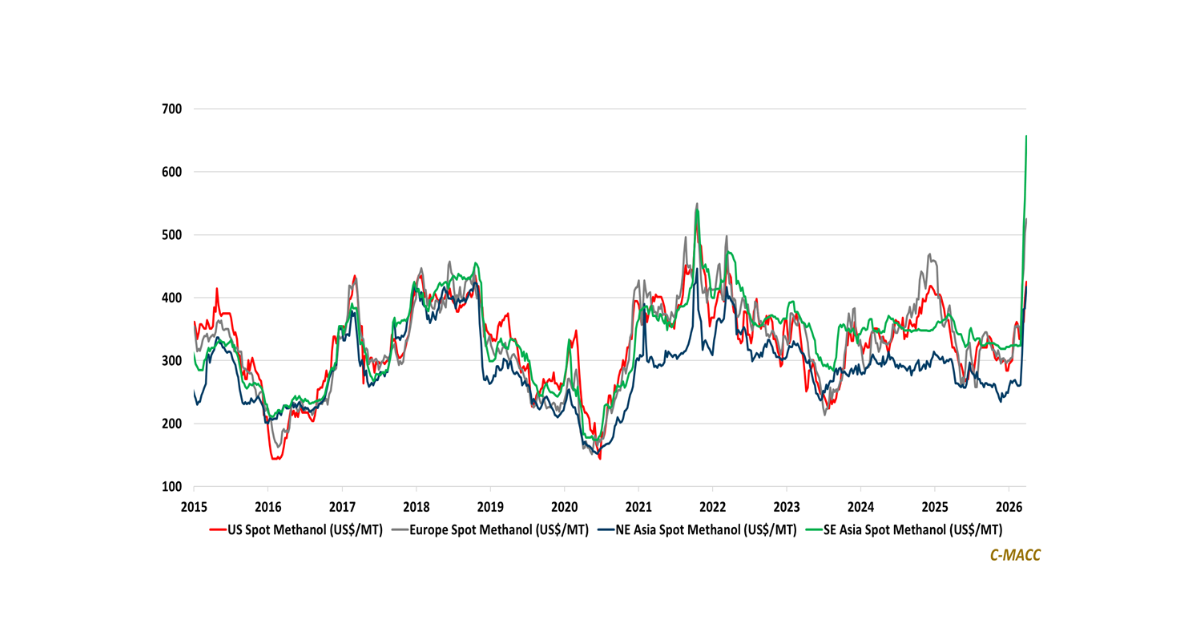

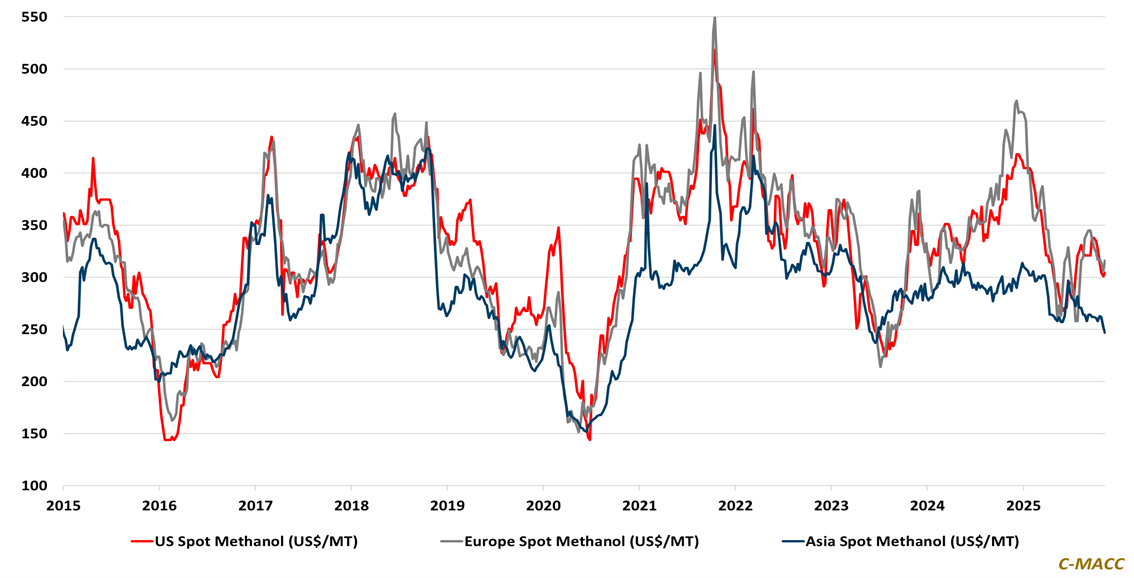

Exhibit 1: Western methanol spot prices to converge toward Asia if freight distortions begin to show structural cracks

Source: Bloomberg, C-MACC Analysis, November 2025

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!