Global Market Analysis

Compressed Gas, Compressed Margins: Why Integration, Not Relief, Defines 2026 Returns

Key Findings

- General Thoughts: Simultaneous natural gas and carbon price compression eases Europe’s cost burden, yet demand fragility, structural import dependence, and risk of renewed global tightening cap competitiveness.

- Supply Chain/Commodities: Inland ammonia allocation and logistics drive nitrogen margin durability, rewarding producers who actively flex product placement rather than relying on global benchmark strength.

- Energy/Upstream: US LNG affordability supports Asian demand growth, yet synchronized global feedstock convergence compresses chemical margins, elevating integration as the primary structural defense.

- Sustainability/Energy Transition: Continued European low-carbon project delays expose structurally impaired risk-adjusted returns, redirecting capital toward integrated, lower-cost industrial ecosystems.

- Downstream/Other Chemicals: Freight normalization in 2026 rewards disciplined carriers and integrated chemical exporters, as overcapacity caps rate upside while margin control determines structural advantage.

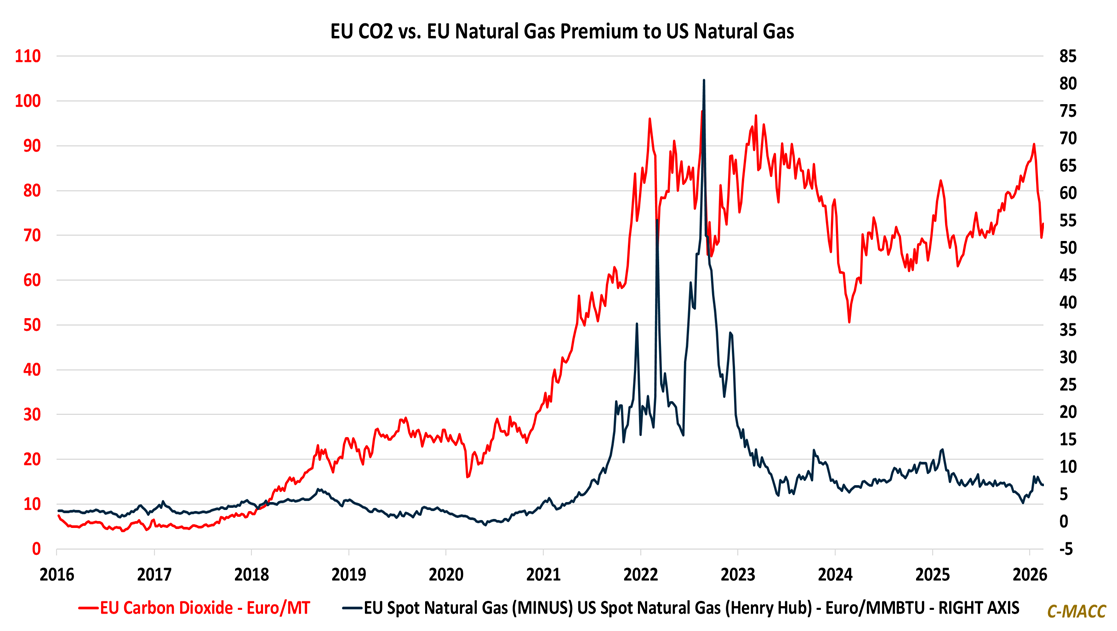

Exhibit 1: Europe’s natural gas and carbon price compression is far from restoring its industrial competitiveness.

Source: Bloomberg, C-MACC Analysis, February 2026

See the PDF below for all charts, tables, and diagrams

Client Login

Learn About Our Subscriptions and Request a Trial

Contact us at cmaccinsights@c-macc.com to gain full access and experience our services!